Yen Rebounds On Risk-Off Mood In Asia, Focus Shifts To SNB And BoE

Asian markets are showing signs of mild risk-off sentiment today, with Hong Kong and China stocks retreating from recent gains. The weaker regional tone contributed to a stronger Yen. Additionally, Yen’s rebound is also fueled by post-FOMC Dollar softness. The technical picture suggests that the recent pullback in Yen against Dollar has likely run its course, allowing the currency to regain some ground.

Meanwhile, the weaker regional sentiment has put pressure on New Zealand Dollar, despite the strong GDP data that showed the country exiting recession. Aussie is also under pressure, not just due to the broader market risk aversion but also because of softer-than-expected employment data, which saw a surprise contraction in jobs. While both the Kiwi and Aussie have had some resilience earlier this week, today’s price action suggests that traders are probably turning more cautious.

SNB rate decision will be the first major focus in the European session, with the central bank widely expected to deliver another 25bps rate cut. A key question is whether SNB signals that the current easing cycle is nearing its end. Attention will then shift to BoE, which is widely expected to keep its benchmark interest rate steady. The focus will be on the voting composition within the MPC.

For the week so far, Dollar is currently the worst performer, followed by Euro and Aussie. On the other hand, Swiss Franc is the strongest, followed by Kiwi and Sterling. Loonie and Yen are positioning in the middle, with Yen’s outlook improving due to today’s risk-off flows.

In Asia, Japan is on holiday. Hong Kong HSI is down -1.51%. China Shanghai SSE is down -0.25%. Singapore Strait Times is up 0.67%. Overnight, DOW rose 0.92%. S&P 500 rose 1.08%. NASDAQ rose 1.41%. 10-year yield fell -0.025 to 4.256.

US stocks recovered as Fed sticks to two rate cut outlook for 2025

US stocks closed higher overnight, and extended their near-term consolidations. Investors were somewhat relieved that Fed maintained its outlook for two rate cuts this year. However, the central bank also introduced a note of caution, warning in its statement that “uncertainty around the economic outlook has increased” and that it remains “attentive to the risks to both sides of its dual mandate.”

In the post-meeting press conference, Chair Jerome Powell explicitly addressed the impact of tariffs. He warned that “the arrival of tariff inflation may delay further progress” on disinflation. He also noted that Fed’s quarterly summary of economic projections does not show further downward progress on inflation this year, attributing this to new tariffs coming into effect.

This acknowledgment reinforces the stance that while rate cuts remain in the pipeline, the timing and extent of policy easing will depend on how inflation evolves in the face of trade disruptions and supply chain adjustments.

Fed left its benchmark interest rate unchanged at 4.25-4.50%, a widely expected move. Fed fund futures now assign roughly 70% probability that the next rate cut will come in June, compared to just 47% a month ago.

Technically, S&P 500 turned into consolidations after falling to 5504.65 last week. 55 W EMA (now at 5596.07) could offer some support for a near term recovery. But risk will stay on the downside as long as 55 D EMA (now at 5873.77) holds.

On resumption, fall from 6147.43, as a correction to the rise from 3491.58, should target 38.2% retracement at 5132.89.

New Zealand GDP exits recession with stronger-than-expected 0.7% qoq growth in Q4

New Zealand’s economy expanded by 0.7% qoq in Q4, surpassing expectations of 0.4% qoq and officially pulling the country out of recession. However, the broader picture remains mixed, as GDP still declined by -0.5% yoy, reflecting the lingering impact of previous contractions.

The positive quarterly growth was driven by expansions in 11 out of 16 industries, with the rental, hiring, and real estate sector, retail trade, and healthcare services leading the gains.

Despite the overall improvement, some key sectors struggled, with construction and information media & telecommunications posting declines.

Still, a major positive takeaway from the report is that GDP per capita rose by 0.4% in Q4, marking its first increase in two years.

Australian employment plunges -52.8k in Feb, unemployment rate unchanged at 4.1%

Australia’s employment dropped sharply by -52.8k in February, significantly missing market expectations of 30k gain. The decline was broad-based, with full-time jobs falling by -35.7k and part-time employment down by -17k.

Unemployment rate remained steady at 4.1%, in line with forecasts. The participation rate declined by -0.4% to 66.8%, suggesting that fewer people were actively seeking work, which helped keep the jobless rate from rising. Additionally, monthly hours worked fell by -0.4% mom, reflecting softer labor market conditions.

The Australian Bureau of Statistics attributed part of the decline in employment to fewer older workers re-entering the labor force. However, the broader trend still points to resilience in the job market, with employment up by 266k people, or 1.9%, compared to last year. The annual employment growth rate remains close to the 20-year pre-pandemic average of 2.0%.

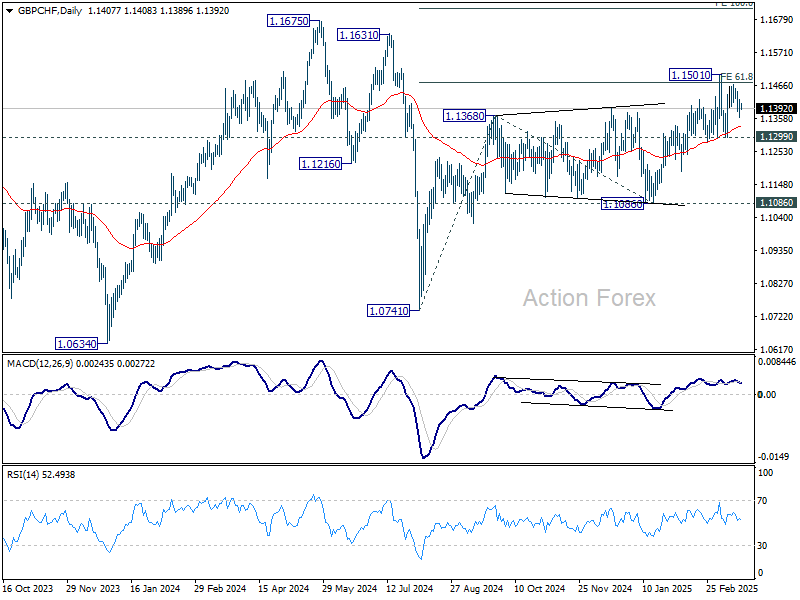

SNB to cut, BoE to hold, a look at GBP/CHF

Two major central banks will announce their monetary policy decisions today, with SNB leading, followed by BoE.

SNB is widely expected to lower its policy rate by 25bps to 0.25%. With inflation at just 0.3% in February, well below the mid-point of target range, there is both room and necessity for further easing to keep medium-term inflation expectations anchored closer to 1%.

However, the urgency for additional policy support appears to be diminishing, especially with growing optimism around Eurozone economy. Stronger Eurozone growth, driven by major fiscal expansion plans, is expected to lift Euro and boost demand for Swiss exports, which could help mitigate recession and deflation risks in Switzerland.

A Reuters poll of economists showed that most expect rates to remain at 0.25% by year-end, while 10 foresee a move to 0%, and only three expect SNB to maintain the current 0.50% level.

Meanwhile, BoE is widely expected to hold its Bank Rate steady at 4.5%, with little change to its cautious forward guidance. A Reuters poll of 61 economists showed unanimous expectations for a rate hold today, with the next cuts projected for May, August, and November.

The key focus for markets will be whether any additional Monetary Policy Committee members join Catherine Mann and Swati Dhingra in voting for an immediate rate cut, which could signal a shift toward a more dovish stance in the coming months.

Technically, while GBP/CHF extended the rally from 1.1086, it has clearly struggled to find convincing momentum. It’s plausible that this rise is the third leg of the corrective rebound from 1.0741, which has already completed after meeting 61.8% projection of 1.0741 to 1.1368 from 1.1086 at 11437. Break of 1.1299 support will solidify this bearish case and bring deeper fall back to 1.1086 support. Nevertheless firm break of 1.1501 will pave the way to 1.1675 resistance next.

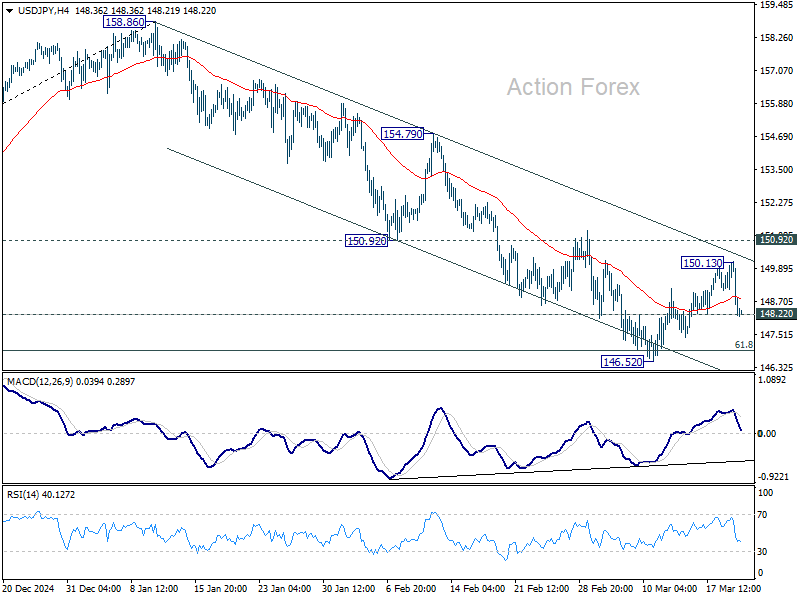

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.15; (P) 149.15; (R1) 149.69; More…

USD/JPY’s currently steep decline suggests rejection by near term falling channel resistance. Immediate focus is now on 148.22 minor support. Firm break there will indicate that corrective rebound from 146.52 has completed and bring retest of this low first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will resume the fall from 158.86 to 139.57 support. In case of another recovery, upside should be limited by 150.92 support turned resistance.

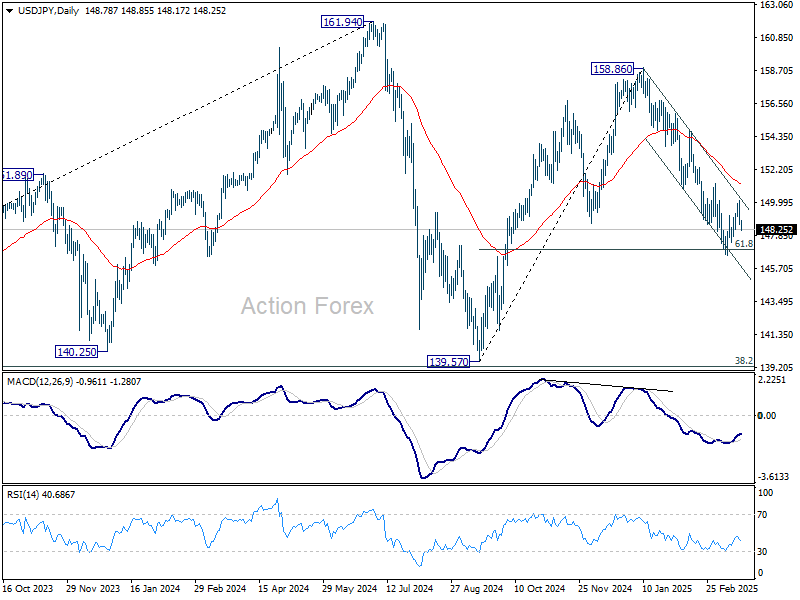

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more