Yen Finds Some Relief From Inflation Data, But Struggles To Rebound

The overall mood in the forex markets remains one of indecision, with major currencies largely range-bound. Yen is attempting a mild rebound after Tokyo’s CPI figures came in stronger than expected, with core-core inflation rising to 2.2% yoy. However, the Japanese currency is still the worst performer of the week, reflecting the broader uncertainty over BoJ’s next move.

Domestically, the sharp surge in rice prices—up 92.4% yoy—will likely be dismissed by BoJ as a temporary shock stemming from supply issues. What will matter more for policy direction is whether the uptick in rents and service-sector inflation, driven by rising wages, proves to be more persistent.

At the same time, BoJ Summary of Opinions revealed a clear concern among board members over downside risks from US tariffs and global economic instability. Even though BoJ remains on a path toward further rate hikes, the timing of the next move is now more uncertain. The central bank may opt to delay any action to better assess the economic fallout from global trade policies.

This cautious stance is mirrored in Fed’s approach as well, with US policymakers signaling patience amid what they describe as a “dense fog” of uncertainty. Tariffs, inflation expectations, and murky consumer sentiment are all contributing to a wait-and-see. While markets still lean toward a June rate cut, the messaging from the Fed increasingly suggests a higher bar for near-term easing.

Paradoxically, should Fed proceed with a rate cut in June, it could spook markets rather than calm them. A cut might be interpreted not as proactive easing, but as a reaction to more serious underlying weakness in the economy.

For the week, Canadian Dollar has outperformed. Australian Dollar follows, lifted by strong commodity performance, while Sterling finds support despite softer UK CPI. Meanwhile, Yen remains the weakest, followed by Kiwi and Euro. Dollar and Swiss Franc treading water in the middle of the pack.

Technically, Gold continues to command attention as its record-breaking rally persists. The precious metal seems to be ignoring what should be formidable resistance at its medium-term rising channel.

On the downside, break below 3012.37 should indicate a near-term rejection and signal the start of a corrective pullback toward the 2832.31/2956.09 support zone.

However, sustained trading above the channel could prompt upside acceleration for the medium term. Next target will be 100% projection of 2584.24 to 2956.09 from 2832.41 at 3204.26

In Asia, at the time of writing, Nikkei is down -2.09%. Hong Kong HSI is down -0.87%. China Shanghai SSE is down -0.54%. Singapore Strait Times is down -0.087%. Japan 10-year JGB yield is down -0.044 at 1.547. Overnight, DOW fell -0.37%. S&P 500 fell -0.33%. NASDAQ fell -0.53%. 10-year yield rose 0.031 to 4.369.

Tokyo CPI core rises to 2.4%, driven by soaring food and rent prices

In Japan, Tokyo’s CPI core, which excludes fresh food, rose from 2.2% yoy to 2.4% yoy in March, surpassing expectations of 2.2% yoy. Even more notable was the rise in the core, core measure, which strips out both food and energy—climbing from 1.9% yoy to 2.2% yoy, signaling broader-based inflation. Headline inflation also ticked higher to 2.9% yoy from 2.8% yoy.

The key driver behind the spike was food prices, which surged 5.6% yoy, the fastest pace since January 2024. A standout was the massive 92.4% yoy jump in rice prices, the steepest rise since 1976.

Adding to the inflationary pressure was the services sector, where prices rose 0.8% yoy, up from 0.6% yoy in February. Rent prices, a key component, increased by 1.1% yoy, the sharpest rise since 1994.

BoJ opinions highlight tariff risks, but path to further hikes still intact

The Summary of Opinions from BoJ’s March monetary policy meeting revealed growing concerns over the fallout from US trade policy, particularly the risk that new tariffs could negatively impact Japan’s real economy.

One board member warned that downside risks from the US have “rapidly heightened”. I f tariff issues worsen, it could have a “negative impact” on Japan’s real economy. BoJ should be “particularly cautious” when considering further interest rate hikes if trade tensions escalate.

Other members echoed similar concerns, citing elevated uncertainty from tariff threats, global supply chain disruptions, and stiff competition from low-priced Chinese products.

The tone suggests policymakers are carefully monitoring how these factors affect inflation expectations, wage growth, and investment—particularly among SMEs.

A separate opinion suggested that as underlying CPI inflation edges closer to the 2% target, BoJ should prepare to shift from accommodative to “neutral” policy.

Overall, BoJ still sees a path toward rate normalization—contingent on its inflation outlook materializing—but recent developments in global trade and domestic firm performance will dictate the pace and timing of the next move.

Fed’s Barkin: It’s “zero visibility” fog, pull over and turn on your hazards

Richmond Fed President Tom Barkin noted that the fast-moving policies of the new administration, particularly around tariffs, have created a “dense fog” of uncertainty. While acknowledging that recent high inflation could amplify the impact of new tariffs, he noted that the ultimate effect remains unknowable given the lack of clarity on final tariff rates and the responses of global actors.

Barkin warned that this heightened uncertainty is already weighing on sentiment. He explained that for consumers and businesses to spend and invest, “they need to have a certain level of confidence”. Without that, demand may quiet, particularly as markets navigate the unknowns tied to policy shifts and geopolitical developments.

“It’s not an everyday ‘forecasting is hard’ type of fog,” he said, but rather one that demands a cautious approach—“a ‘zero visibility, pull over and turn on your hazards’ type of fog.”

In this context, Barkin reiterated that the Fed’s current moderately restrictive stance remains appropriate. “We are waiting for the fog to clear,” he concluded.

Fed’s Collins Advocates “active patience” with interest rates

Boston Fed President Susan Collins expressed her full support for Fed to keep interest rates unchanged last week, noting that continued economic uncertainty and inflation risks warrant a cautious approach.

Collins said that with upside risks to inflation still present, it would likely be appropriate to maintain current policy settings “for a longer time”. She stressed the importance of “active patience” and flexibility as Fed monitors the evolving economy.

One of the key factors now clouding the outlook is tariffs. Collins acknowledged that new tariffs will almost certainly raise inflation in the near term. However, the longer-term implications depend heavily on how other countries react and whether businesses pass costs onto consumers. These elements could determine whether the inflationary shock is temporary or more persistent.

Looking ahead

Germany Gfk consumer sentiment and unemployment; UK retail sales, goods trade balance and Q4 GDP final; Swiss KOF will be released in European session. Later in the day, Canada will release monthly GDP. US will release personal income and spending, and PCE inflation.

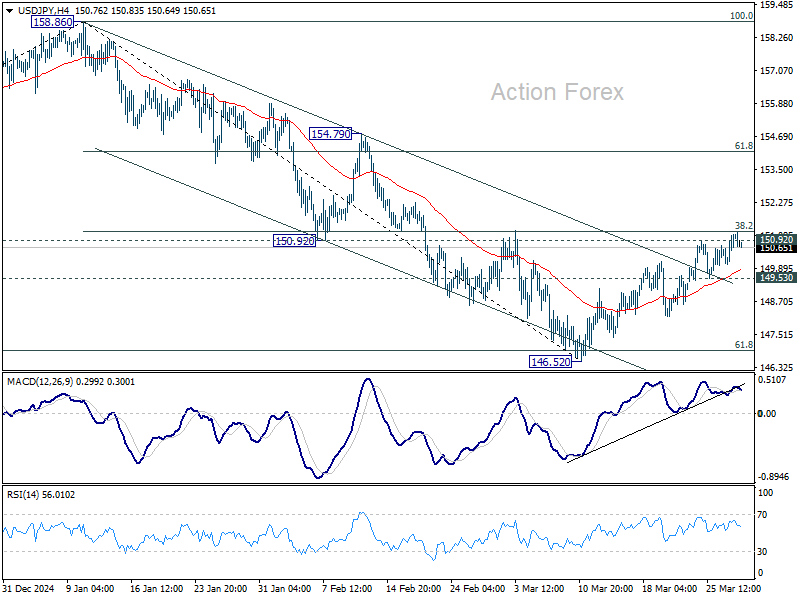

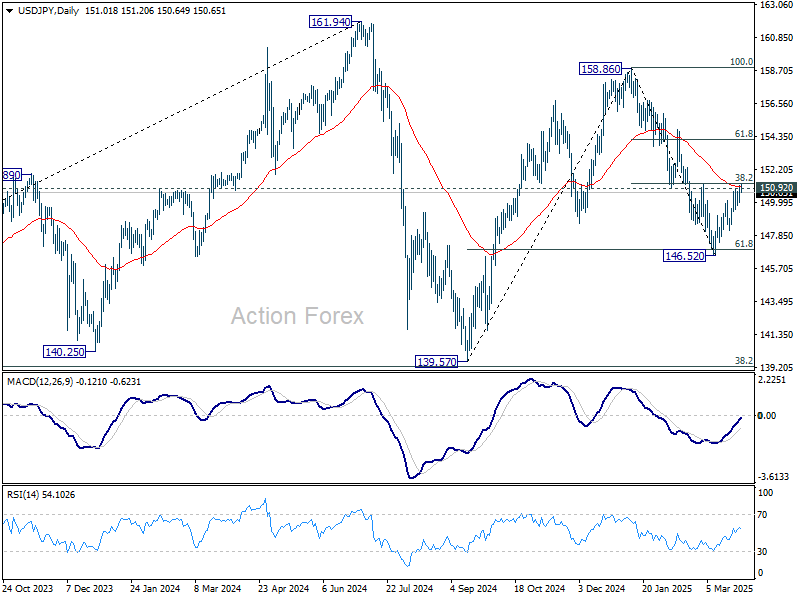

USD/JPY Daily Outlook

Daily Pivots: (S1) 150.35; (P) 150.75; (R1) 151.45; More…

No change in USD/JPY’s outlook and intraday bias remains neutral. Strong resistance is still expected from 150.92 to complete the corrective recovery from 146.52. On the downside break of 149.53 support will bring retest of 146.52 first. Sustained trading below 61.8% retracement of 139.57 to 158.86 at 146.32 will resume the fall from 158.86 to 139.57 support. However, firm break of 150.92 will argue that fall from 158.86 has completed and turn bias back to the upside for 154.79 resistance next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more