Tariff Sparks Risk Exodus; Euro Rises As Preferred Shelter

Risk-off sentiment swept across global financial markets today following the U.S. announcement of sweeping reciprocal tariffs. The sheer scale, complexity, and breadth of the trade measures surprised investors and rattled confidence. Equities in Europe and Japan suffered broad losses, but the brunt of the selloff appears to be landing squarely on US markets, where the mood has sharply deteriorated.

Now the spotlight turns to whether bargain hunters will step in to stabilize equity markets and provide some relief through the rest of the week. Without a decisive rebound, there is a real risk that the current slide could deepen into a prolonged selloff through the rest of April, especially if the anticipated retaliation from global trading partners begins to materialize in the coming days.

In currency markets, Dollar is being dumped across the board. Aussie is also among the weakest, likely suffering from its exposure to China. Surprisingly, Sterling joined the bottom three, mostly due to heavy selling against Euro and Swiss Franc.

The standout performers are clearly the traditional safe-havens: Yen, Swiss Franc. Notably, Euro is emerging as the key substitute for the greenback in terms of liquidity and market depth. Loonie and Kiwi are holding in the middle.

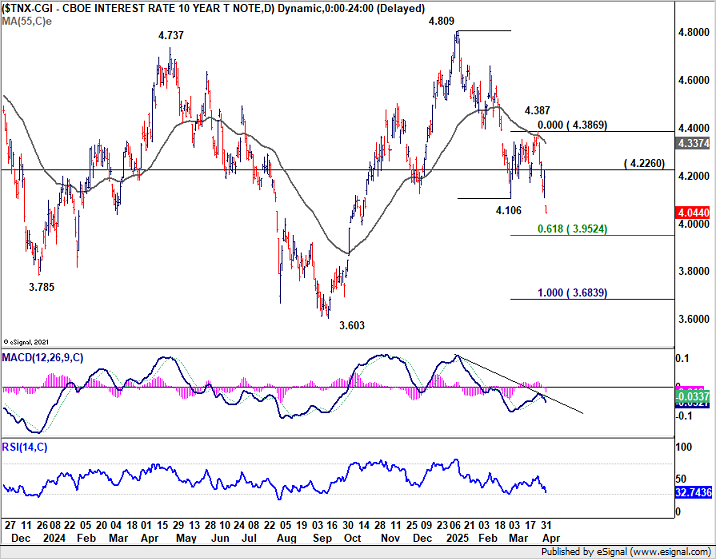

Technically, US 10-year yield’s strong break of 4.106 support confirms resumption of the whole decline from 4.809. Risk will now stay heavily on the downside as long as 4.226 resistance holds. Next target is 61.8% projection of 4.809 to 4.106 from 4.387 at 3.952.

Strong support is anticipated there as it’s close to 4% mark. However, firm break of 3.952, especially sustained trading below the critical 4% psychological threshold — would likely deal a heavy blow to sentiment and spark even deeper losses in risk assets.

In Europe, at the time of writing, FTSE is down -1.38%. DAX is down -2.13%. CAC is down -2.80%. UK 10-year yield is down -0.111 at 4.536. Germany 10-year yield is down -0.079 at 2.644. Earlier in Asia, Nikkei fell -2.77%. Hong Kong HSI fell -1.52%. China Shanghai SSE fell -0.24%. Singapore Strait Times fell -0.30%. Japan 10-year JGB yield fell -0.129 to 1.351.

US initial jobless claims fall to 219k vs exp 225k

US initial jobless claims fell -6k to 219k in the week ending March 29, below expectation of 224k. Four-week moving average of initial claims fell -1k to 223k.

Continuing claims rose 56k to 1903k in the week ending March 22, highest since November 13, 2021. Four-week moving average of continuing claims rose 3k to 1871k.

ECB Accounts: March debate leaves April meeting open to cut or hold

ECB’s March 5-6 meeting accounts revealed a heated debate among Governing Council members over both the 25bps rate cut decision and the tone of accompanying communications.

With considerable uncertainty clouding the outlook—ranging from global trade policy to persistent services inflation—many policymakers urged caution, particularly in avoiding language that could be construed as forward guidance. The balance of risks, especially from tariff escalations and uneven disinflation, made it clear that any commitment to further cuts would be premature.

A few members were only willing to support the March rate cut on the condition that the policy statement “avoided any indication of future cuts or of the future direction of trave”.

This led to a debate on whether to remove the phrase “monetary policy remains restrictive”. In the end, Chief Economist Philip Lane’s proposed compromise—“monetary policy is becoming meaningfully less restrictive”—was broadly accepted.

This phrasing was viewed as neutral enough to reflect the evolving inflation outlook without implying a preset path.

Crucially, the ECB emphasized that the revised language should not signal the outcome of April’s meeting. “Both a cut and a pause” are “on the table, depending on the incoming data.

ECB’s Nagel and Stournaras warn of economic fallout from US tariffs

Bundesbank President Joachim Nagel issued a strong warning today, saying the US administration’s new tariff measures “endanger global economic stability.”

Nagel emphasized the need for strong alliances and fewer trade barriers to tackle today’s global challenges, adding that the US is pursuing a “completely different direction” with economic policies that could leave many losers—especially within its own borders.

Echoing these concerns, Greek ECB Governing Council member Yannis Stournaras said the US tariffs are expected to weigh on Eurozone GDP growth rate by 0.3% to 0.4% in the first year, though he noted that the broader inflation outlook remains unaffected.

Stournaras added that the US tariffs were “not an obstacle” to an ECB rate cut in April.

Eurozone PPI rises 0.2% mom, 3.0% yoy in Feb

Eurozone PPI rose 0.2% mom and 3.0% yoy in February. The monthly gain was primarily driven by a 0.4% mom increase in prices for intermediate goods, alongside smaller rises in energy (0.2% mom) and capital goods (0.2% mom) prices. Prices for durable consumer goods slipped slightly, down -0.1% mom, while non-durable consumer goods posted a mild 0.1% mom uptick. Excluding energy, total industrial prices increased by 0.2% mom.

Across the broader EU, PPI rose 0.3% mom on the month and 3.1% yoy. The strongest monthly gains were recorded in Estonia (+9.5%), Romania (+4.8%), and Bulgaria (+2.5%), while declines were seen in Ireland (-4.9%), France, and Slovakia (both -0.8%).

Eurozone PMI composite finalized at 50.9, steady but shaky

Eurozone’s private sector continued to show signs of stabilization in March, with PMI Composite finalized at 50.9 — the highest in seven months — up from February’s 50.2. PMI Services was finalized at 51.0, up from prior month’s 50.6.

Among the major economies, Germany stood out with a 10-month high at 51.3, while France remained in contraction despite improving to a five-month high at 48.0.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, acknowledged that recession fears that loomed late last year are now giving way to cautious optimism. The Eurozone has managed to stay in growth territory for three straight months.

Still, he warned that this fragile recovery could be easily thrown “off course again” by external shocks — namely, the newly announced US reciprocal tariffs.

UK PMI services finalized at 52.5, outlook and employment subdued

UK PMI Services was finalized at 52.5 in March, up from 51.0 in February, marking the highest level since August 2024. PMI Composite also improved to 51.5, a five-month high.

The modest recovery in overall business activity was driven primarily by strength in the technology and financial services sectors, according to Tim Moore at S&P Global. However, this was offset by notable weakness in manufacturing, which experienced its steepest decline in output since October 2023.

However, service providers expressed limited optimism about the near-term outlook, with confidence levels hovering near two-year lows. The labor market also continued to show signs of strain, with March marking the sixth consecutive month of job losses due to hiring freezes and redundancies.

Price pressures remain a concern. The inflation indicators within the survey suggest that cost and pricing pressures in the services sector are still running significantly hotter than the pre-pandemic decade.

Swiss CPI unchanged at 0.3% yoy in Mar, misses expectations

Swiss consumer inflation remained subdued in March, with headline CPI unchanged on the month, below the expected 0.1% mom rise. Core CPI (excluding fresh and seasonal products, energy and fuel) rose just 0.1% mom. The breakdown showed a -0.1% mom decline in domestic product prices, offset somewhat by a 0.5% mom rise in prices of imported products.

On an annual basis, headline CPI held steady at just 0.3% yoy, missing expectations for an uptick to 0.5% yoy. Core inflation also remained unchanged at 0.9% yoy. The slight increase in domestic product inflation from 0.9% yoy to 1.0% yoy suggests some persistence in local cost pressures. But overall imported inflation remains deeply negative at -1.7% yoy, down from -1.5% yoy.

Japan’s PMI composite finalized at 48.9, back in contraction

Japan’s services sector lost momentum in March, with the final PMI Services reading falling to the neutral mark of 50.0, down sharply from 53.7 in February. Composite PMI dropped to 48.9—its lowest since November 2022—signaling contraction in overall private sector activity.

S&P Global’s Annabel Fiddes noted that while new orders and export business in services remained in growth territory, market conditions had clearly softened.

Additionally, input costs across the private sector rose at the fastest pace in seven months, and output price inflation remained historically elevated.

Business sentiment also deteriorated, with overall optimism about the year-ahead outlook for output falling to its lowest since January 2021.

China’s Caixin PMI services rises to 51.9, but deflation and jobs remain concerns

China’s Caixin Services PMI ticked up to 51.9 in March from 51.4, while Composite PMI rose to 51.8 from 51.5, marking the 17th consecutive month of expansion.

According to Caixin Insight Group’s Wang Zhe, both supply and demand showed improvement, particularly in manufacturing. However, service sector employment dragged overall job growth, and price pressures remained weak.

Despite signs of recovery and a stable start to the year, persistent deflationary pressures and a sluggish job market continue to weigh on sentiment. Wang noted that weak domestic demand and cautious market expectations were limiting momentum.

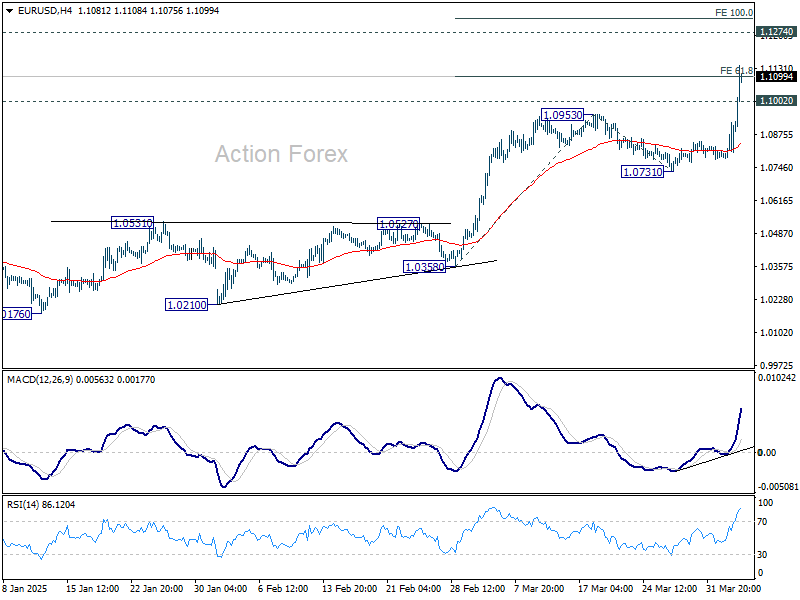

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0785; (P) 1.0855; (R1) 1.0929; More…

EUR/USD’s rally accelerates to as high as 1.1145 so far, and met 61.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1099 already. Intraday bias stays on the upside. Sustained trading above 1.1099 will pave the way 1.1274 key resistance, and probably further to o 100% projection at 1.1326. On the downside, below 1.1002 minor support will turn intraday bias neutral and bring consolidations, before staging another rise.

In the bigger picture, prior strong break of 55 W EMA (now at 1.0692) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0731 support holds.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more