Tariff Shock Hits US Markets Hard, But Global Reactions Split

Reactions in the US markets to the long-anticipated reciprocal tariff announcement were decisively negative. NASDAQ futures tumbled more than -3%, while DOW futures shed as much as -2% at one point. US 10-year yields plunged below the 4.1% mark, highlighting a strong wave of safe haven flows. The reactions confirm what traders feared most—not just new tariffs, but the sheer complexity and breadth of the measures rolled out by the White House.

However, the global market reaction was more uneven. Japan’s Nikkei plummeted by over -1,000 points, nearly -3%, reflecting its vulnerability given the 24% tariff rate applied to its goods. Meanwhile, Hong Kong’s HSI fared relatively better, falling by just -1.5%, while Singapore’s Straits Times Index even managed to claw back most of its early mild losses.

In currency markets, Aussie and Kiwi led the declines, driven by broad risk aversion and China’s exposure to some of the harshest tariff levels. Dollar also came under pressure, as investors pulled out of US assets. Yen emerged as the day’s biggest gainer on classic safe-haven flows, followed by Swiss Franc. Euro, Pound, and Canadian Dollar showed some resilience, as the EU, UK, and Canada either received relatively milder rates or were temporarily spared.

The White House confirmed a baseline 10% tariff on all countries starting April 5, with “reciprocal” rates up to 50% going into effect on April 9. Contrary to earlier hopes that the 10–20% range would serve as a maximum cap, these figures now appear to be just the starting point.

The US claims the new tariffs reflect roughly half of the effective trade barriers faced by American exports, accounting for both monetary and non-monetary impediments. But in practice, this means a steep increase in trade costs.

Many allies, including the EU (20%) and Japan (24%), were not spared, although Canada and Mexico were temporarily exempt. What’s more concerning is that these new tariffs are being layered on top of existing duties. The effective rate for China has ballooned to a staggering 54%, factoring in both new and existing duties.

The list of exemptions is narrow, covering only certain critical imports such as copper, pharmaceuticals, energy products, semiconductors, and minerals not available domestically.

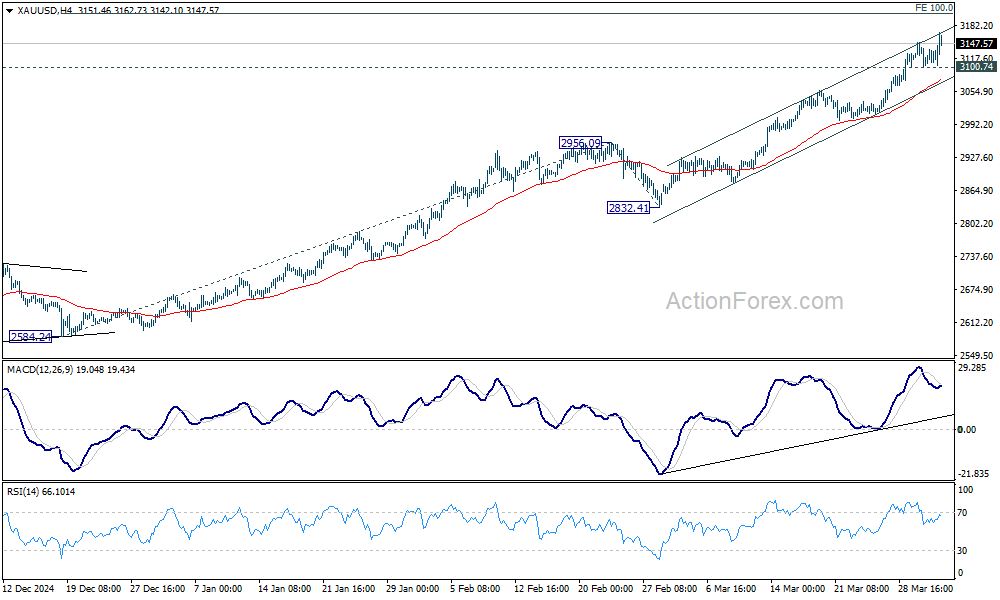

Gold, as expected, surged to a fresh record amid the turmoil, but signs of momentum exhaustion are emerging. While further rally is expected, Gold might find strong resistance at 100% projection of 2584.24 to 2956.09 from 2832.41 at 3204.26 to limit upside, at least on first attempt. Break of 3100.74 support will indicate short term topping and bring consolidations.

In Asia, at the time of writing, Nikkei is down -2.95%. Hong Kong HSI is down -1.77%. China Shanghai SSE is down -0.52%. Singapore Strait Times is down -0.17%. Japan 10-year JGB yield is down -0.099 at 1.38. Overnight, DOW rose 0.56%. S&P 500 rose 0.67%. NASDAQ rose 0.87%. 10-year yield rose 0.040 to 4.196.

Japan’s PMI composite finalized at 48.9, back in contraction

Japan’s services sector lost momentum in March, with the final PMI Services reading falling to the neutral mark of 50.0, down sharply from 53.7 in February. Composite PMI dropped to 48.9—its lowest since November 2022—signaling contraction in overall private sector activity.

S&P Global’s Annabel Fiddes noted that while new orders and export business in services remained in growth territory, market conditions had clearly softened.

Additionally, input costs across the private sector rose at the fastest pace in seven months, and output price inflation remained historically elevated.

Business sentiment also deteriorated, with overall optimism about the year-ahead outlook for output falling to its lowest since January 2021.

China’s Caixin PMI services rises to 51.9, but deflation and jobs remain concerns

China’s Caixin Services PMI ticked up to 51.9 in March from 51.4, while Composite PMI rose to 51.8 from 51.5, marking the 17th consecutive month of expansion.

According to Caixin Insight Group’s Wang Zhe, both supply and demand showed improvement, particularly in manufacturing. However, service sector employment dragged overall job growth, and price pressures remained weak.

Despite signs of recovery and a stable start to the year, persistent deflationary pressures and a sluggish job market continue to weigh on sentiment. Wang noted that weak domestic demand and cautious market expectations were limiting momentum.

Looking ahead

ECB meeting accounts is a main feature in European session. Eurozone will release PPI and PMI services final. UK will also release PMI services final while Switzerland will publish CPI.

Later in the day, US ISM services will be the focus, as trade balance and jobless claims will be released. Canada trade balance will also be featured.

USD/JPY Daily Outlook

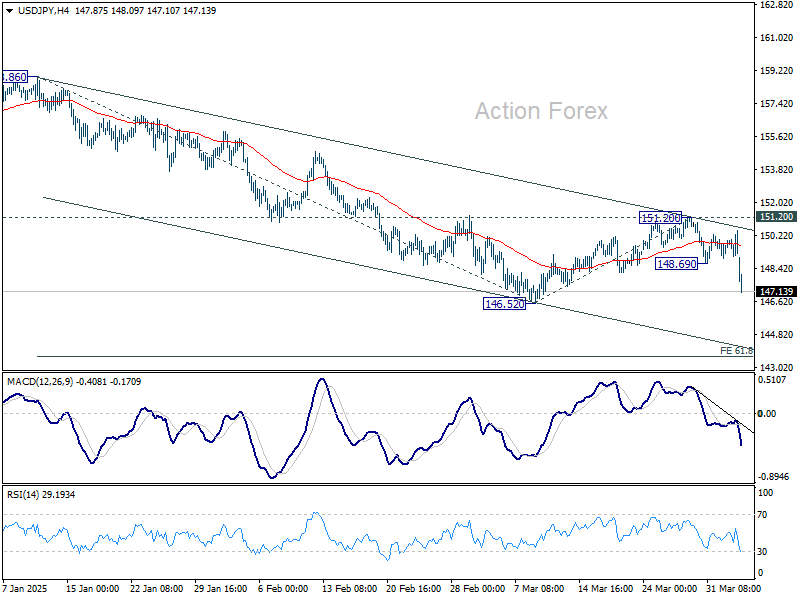

Daily Pivots: (S1) 148.80; (P) 149.64; (R1) 150.19; More…

Intraday bias in USD/JPY is back on the downside with break of 148.69 and retest of 146.52 low should be seen next. Firm break there will resume whole fall from 158.86. Next target is 61.8% projection of 158.86 to 146.52 from 151.20 at 143.57. On the upside, above 148.69 support turned resistance will turn intraday bias neutral first. But recovery should be limited below 151.20 resistance to bring another fall.

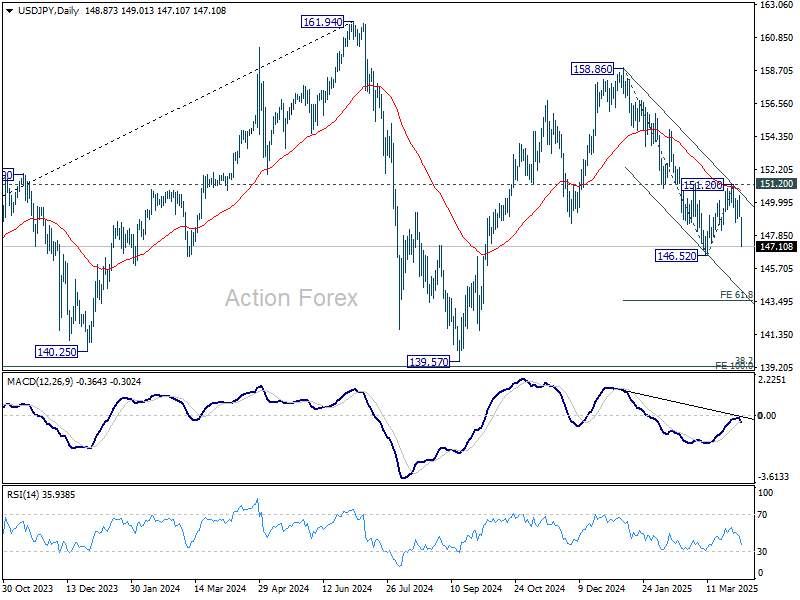

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more