Sterling Holds Firm After BoE, But Dollar And Yen Outperform

Sterling is trading slightly firmer today, though it struggles against the rebounding Dollar and Yen. BoE’s rate decision leaned slightly more hawkish than expected, with only one member of the MPC, the known dove Swati Dhingra, voting for a rate cut. The rest supported keeping rates on hold. The overall tone of the statement remained unchanged, reinforcing a gradual and cautious approach to monetary easing. While BoE acknowledged downside risks to growth, it sounded alert on inflation persistence, signaling that the central bank is unlikely to rush into aggressive rate cuts.

Meanwhile, Swiss Franc weakened after the SNB cut rates by 25bps to 0.25%. The message wasn’t particularly dovish. The central bank still see inflation rising back to 0.8% in 2026. Given that interest rates are already at an ultra-low level, if incoming data aligns with this forecast, further rate cuts may not be necessary anytime soon. This outlook helped cushion Franc’s downside but was not enough to prevent weakness against stronger currencies like Yen and Dollar.

In the broader forex markets, Dollar and Yen are leading the charge today, though their rebounds remain relatively unconvincing. Both currencies have struggled to sustain momentum so far despite benefiting mildly from renewed risk aversion in global markets. Meanwhile, Kiwi and Aussie are under pressure, appearing to be weighed down by dampened sentiment. Loonie and European majors are stuck in the middle of the pack.

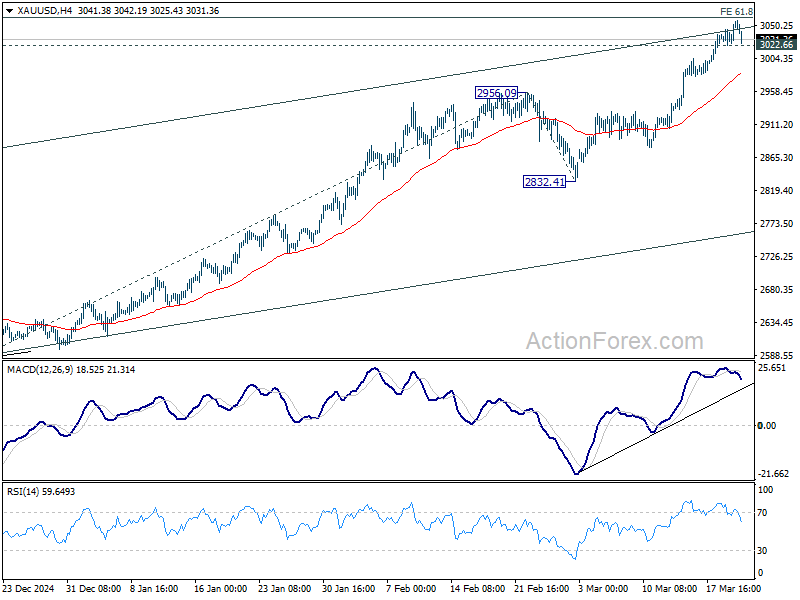

Technically, Gold is struggling to extend gains, as it loses momentum near key resistance levels. It has so far failed to decisively break above the 61.8% projection of 2584.24 to 2956.09 from 2832.41 at 3062.21, a level that coincides with a medium-term rising channel resistance. A break below 3022.66 support would indicate short-term topping, potentially leading to a deeper pullback toward the 55 4H EMA (now at 2983.99) or even further into the 2832.41/2956.09 support zone.

In Europe, at the time of writing, FTSE is down -0.07%. DAX is down -1.40%. CAC is down -0.96%. UK 10-year yield is down -0.045 at 4.597. Germany 10-year yield is down -0.043 at 2.764. Earlier in Asia, Japan was on holiday. Hong Kong HSI fell -2.23%. China Shanghai SSE fell -0.51%. Singapore Strait Times rose 0.57%.

US initial jobless claims rise to 223k vs exp 222k

US initial jobless claims rose 2k to 223k in the week ending March 15, slightly above expectation of 222k. Four-week moving average of initial claims rose 750 to 227k.

Continuing claims rose 33k to 1892k in the week ending March 18. Four-week moving average of continuing claims rose 6k to 1876k.

BoE holds rates at 4.50%, Dhingra lone dissenter for a cut

BoE left the benchmark Bank Rate unchanged at 4.50%, in line with market expectations. Known dove Swati Dhingra once again dissenting, and voted in favor of a 25bps rate cut. However, Catherine Mann, who had previously voted for a 50bps cut, switched her stance and supported keeping rates on hold.

The accompanying statement emphasized a “gradual and careful approach” to rate cuts, reinforcing that BoE is not in a rush to ease policy despite some signs of economic softness.

BoE also highlighted growing global uncertainties, particularly surrounding intensified trade policy risks and geopolitical tensions. The committee acknowledged the impact of new US tariffs and retaliatory measures from some governments. Additionally, recent German fiscal reforms were noted.

While UK GDP growth has been “slightly stronger than expected”, business surveys continue to point to underlying weakness in employment intentions and broader economic activity. BoE expects CPI to rise to around 3.75% in Q3 2025, and to “fall back thereafter”. But policymakers remain cautious about potential persistent inflationary pressures.

UK payrolled employment rises 21k in Feb, unemployment rate unchanged at 4.4% in Jan

In February, UK payrolled employment rose by 21k (0.1% mom). However, median monthly pay growth slowed to 5.0% yoy from 6.0%, reinforcing signs that wage pressures are gradually easing. However claimant count, surged 44.2k, far exceeding expectations of 7.9k.

In the three months to January, unemployment rate remained unchanged at 4.4%, slightly better than the expected 4.5%. Average earnings including bonuses rose by 5.8% yoy, just below expectations of 5.9%. Excluding bonuses, wages rose 5.9% yoy, in line with forecasts.

SNB cuts 25bps, flags downside inflation risks and uncertain growth outlook

SNB delivered a widely expected 25bps rate cut, bringing the policy rate down to 0.25%. In its statement, SNB justified the decision by pointing to low inflationary pressures and “heightened downside risks to inflation”.

The central bank acknowledged that Switzerland’s economic outlook has become “considerably more uncertain”, particularly due to rising global trade tensions and geopolitical risks. The external environment remains a key threat to growth.

The new conditional inflation forecast suggests that inflation will remain well within its price stability range, averaging 0.4% in 2025, and 0.8% in both 2026 and 2027. These projections assume that the policy rate stays at 0.25% throughout the forecast horizon.

On the growth front, SNB expects GDP to expand between 1% and 1.5% in 2025, with domestic demand benefiting from rising real wages and easier monetary conditions. However, weak external demand is expected to act as a drag on growth. For 2026, SNB anticipates GDP growth of around 1.5%.

ECB’s Lagarde warns US-EU tariff war could slash eurozone growth by 0.5%

Speaking to a European Parliament committe, ECB President Christine Lagarde warned that US tariffs of 25% on European imports could have a significant negative impact on the Eurozone economy, cutting growth by around 0.3% in the first year.

If the EU responds with retaliatory tariffs, the impact could deepen, reducing Eurozone GDP growth by as much as 0.5%.

While the sharpest impact would be felt in the first year, Lagarde emphasized that the effects would be long-lasting, leaving a “persistent negative effect on the level of output”.

Beyond growth concerns, inflation outlook would also become highly uncertain in such a scenario.

In the short term, EU retaliatory measures and a weaker Euro—stemming from lower US demand for European products—could push inflation higher by around 0.5%.

In the medium term, weaker economic activity would dampen price pressures, ultimately counteracting the initial inflationary impact.

New Zealand GDP exits recession with stronger-than-expected 0.7% qoq growth in Q4

New Zealand’s economy expanded by 0.7% qoq in Q4, surpassing expectations of 0.4% qoq and officially pulling the country out of recession. However, the broader picture remains mixed, as GDP still declined by -0.5% yoy, reflecting the lingering impact of previous contractions.

The positive quarterly growth was driven by expansions in 11 out of 16 industries, with the rental, hiring, and real estate sector, retail trade, and healthcare services leading the gains.

Despite the overall improvement, some key sectors struggled, with construction and information media & telecommunications posting declines.

Still, a major positive takeaway from the report is that GDP per capita rose by 0.4% in Q4, marking its first increase in two years.

Australian employment plunges -52.8k in Feb, unemployment rate unchanged at 4.1%

Australia’s employment dropped sharply by -52.8k in February, significantly missing market expectations of 30k gain. The decline was broad-based, with full-time jobs falling by -35.7k and part-time employment down by -17k.

Unemployment rate remained steady at 4.1%, in line with forecasts. The participation rate declined by -0.4% to 66.8%, suggesting that fewer people were actively seeking work, which helped keep the jobless rate from rising. Additionally, monthly hours worked fell by -0.4% mom, reflecting softer labor market conditions.

The Australian Bureau of Statistics attributed part of the decline in employment to fewer older workers re-entering the labor force. However, the broader trend still points to resilience in the job market, with employment up by 266k people, or 1.9%, compared to last year. The annual employment growth rate remains close to the 20-year pre-pandemic average of 2.0%.

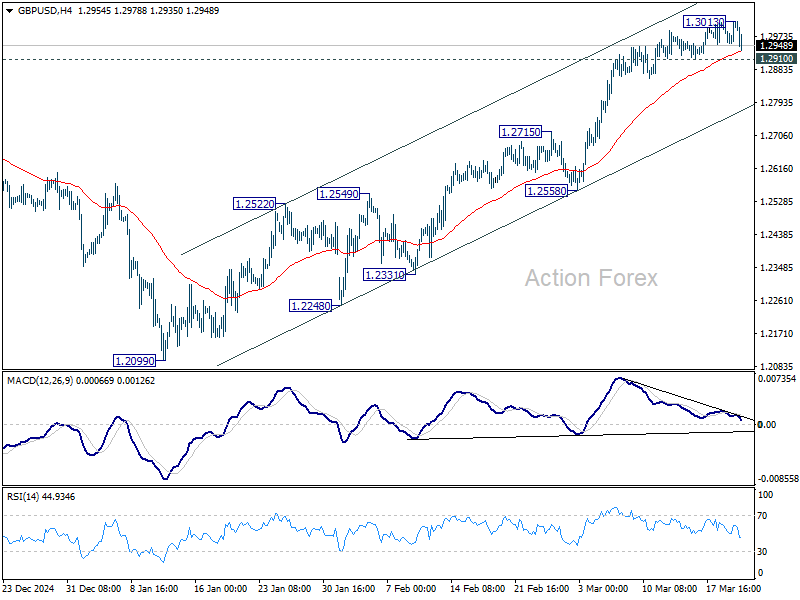

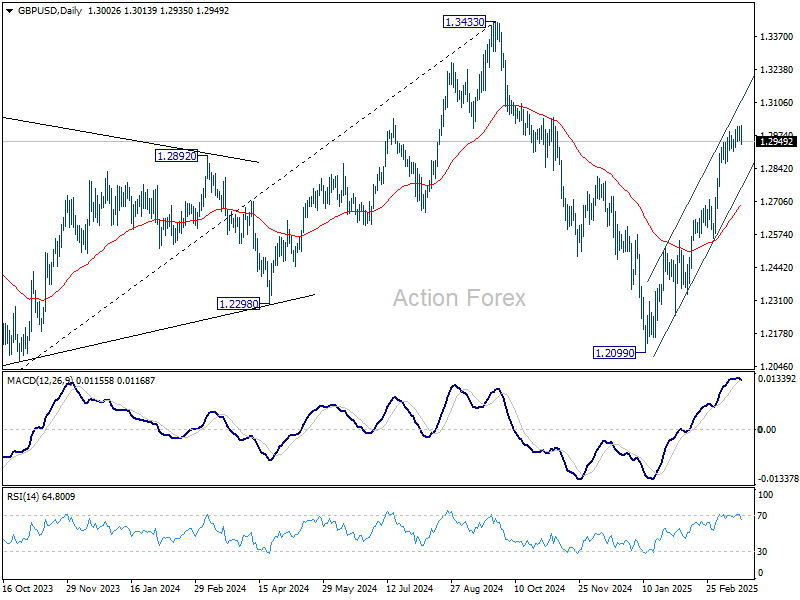

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2969; (P) 1.2990; (R1) 1.3025; More…

Intraday bias in GBP/USD is turned neutral again with current retreat. On the downside, firm break of 1.2910 support should confirm short term topping, on bearish divergence condition in 4H MACD. In this case, intraday bias will be back on the downside for near term channel support (now at 1.2770). On the upside, though, above 1.3013 will resume the rally from 1.2099 towards 1.3433 high.

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more