Safe Havens Surge, Treasury Rout Deepens, US Assets Hit By Relentless Selloff

The brief moment of optimism following the US tariff truce has quickly faded, as financial markets buckle again under renewed pressure. US stocks closed sharply lower overnight, wiping out a large portion of Wednesday’s historic rebound. The risk-off tone spilled into Asia, though unevenly—Japan saw steep losses, Singapore posted moderate declines, while Hong Kong and China held relatively steady. Overall, the ongoing huge volatility suggests that global markets are far from stabilizing.

The trade war narrative has shifted into a far more dangerous phase. The US confirmed that tariffs on Chinese imports were immediately raised to 125% after China responded with an 84% rate of its own. That brings total US duties on Chinese goods to a staggering 145%. At these levels, the tariff figures themselves become much less relevant. The policy is signaling a structural decoupling of the world’s two largest economies.

Yet, the most alarming development is unfolding in the US Treasury market as 10-year yield surged past 4.45% mark again in Asian trading. This sharp reversal from the temporary calm after the US paused some reciprocal tariffs for 90 days is stoking fears of deeper structural issues in bond markets. This trouble in Treasuries has drawn comparisons to the 2020 “dash-for-cash” and the 2022 UK gilt crisis.

In the currency markets, the flight to safety is clear, just not into Dollar. Swiss Franc surged to its highest level against the greenback since 2015, while Euro and Yen also strengthened markedly. Altogether, markets appear to be undergoing a synchronized flush-out of US assets, with investors dumping stocks, Dollar, and even Treasuries.

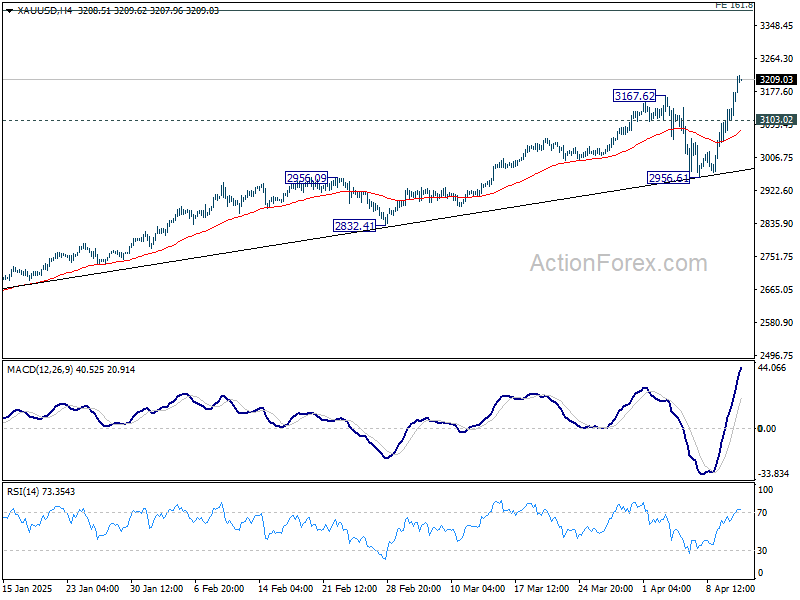

Technically, Gold defied gravity again and surged to new record high above 3200 market. For now, further rise is expected as long as 3103.02 support holds, or in short 3100 mark. Next target is 161.8% projection of 2293.45 to 2789.92 from 2584.24 at 3387.52.

In Asia, at the time of writing, Nikkei is down -4.36%. Hong Kong HSI is up 0.76%. China Shanghai SSE is up 0.32%. Singapore Strait Times is down 1.94%. Japan 10-year JGB yield is up 0.024 at 4.46. Overnight, DOW fell -2.50%. S&P 500 fell -3.46%. NASDAQ fell -4.31%. 10-year yield fell -0.006 to 4.394.

Fed’s Goolsbee: No playbook for tariff shock, rate path uncertain but likely lower

Speaking overnight, Chicago Fed President Austan Goolsbee said that nothing is “off the table”, including rate hikes, cuts, or holds. The sheer scale of recent trade developments creates a stagflationary shock, and there is “not a generic playbook” for how a central bank should respond to.

Also, Goolsbee noted a key challenge: the data being released now may not yet fully reflect the evolving reality on the ground. That’s why he believes Fed must closely monitor both hard data and soft indicators, especially as lag effects complicate interpretation.

Despite the tariff-related uncertainty, Goolsbee still sees rates trending lower over the next one to two years. Nevertheless, he stressed that should long-run inflation expectations begin to drift, “any central bank almost has to address that… regardless of what the other conditions are.”

Fed’s Collins: Tariff-driven price pressures may delay further policy normalization

Boston Fed President Susan Collins said in a speech overnight that keep interest rate at current level is “appropriate for the time being” due to the “highly uncertain environment.”

Collins acknowledged that “renewed price pressures” from tariffs could “delay further normalization of policy”.

“Confidence is needed that the tariffs are not destabilizing inflation expectations,” she emphasized.

She added that any “preemptive action” to support growth would require a “compelling” signal that economic activity is deteriorating more than expected.

Although she expects inflation to gradually return to the 2% target, she acknowledged that core inflation may rise “well above” 3% in the near term due to higher import costs. In her view, the Fed must remain vigilant to ensure these pressures do not become entrenched.

NZ BNZ manufacturing falls to 53.2, new orders signal trouble ahead

New Zealand’s BusinessNZ Performance of Manufacturing Index slipped slightly from 54.1 to 53.2 in March, but remained firmly in expansion territory. Production climbed to 54.2, the highest level since December 2021. Employment also posted a robust 54.7, marking its strongest result since mid-2021. However, a decline in new orders, which dipped below the 50-neutral mark to 49.6, raises concerns about the durability of this rebound.

BusinessNZ’s Catherine Beard acknowledged the resilience in activity and employment, but highlighted persistent challenges. Despite improving sentiment, nearly 58% of surveyed manufacturers cited negative conditions, pointing to weak demand, fewer new orders, and uncertainty across both domestic and export channels.

BNZ Senior Economist Doug Steel noted that the PMI data supports the case for manufacturing GDP growth in early 2025. Still, he cautioned that risks to the outlook are clearly tilted to the downside, “given recent extreme volatility on global markets following rapidly evolving US-driven trade policy changes.”

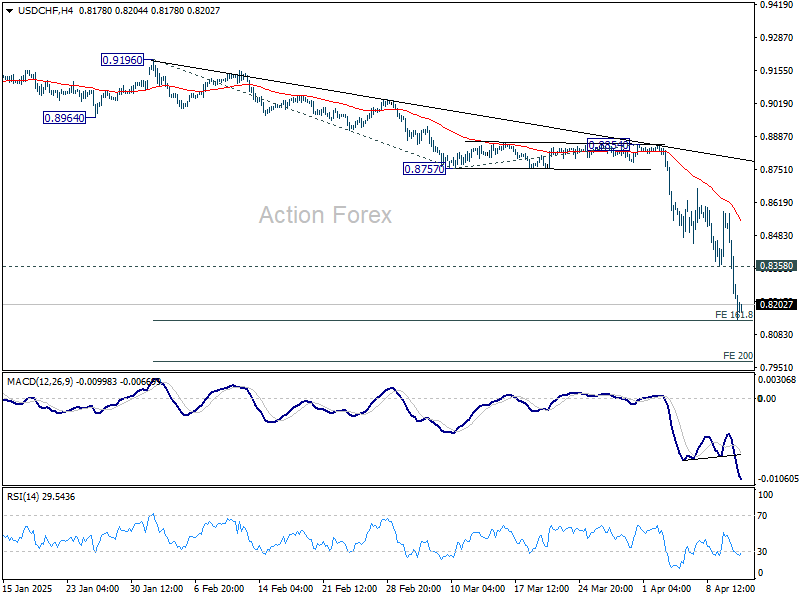

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8120; (P) 0.8350; (R1) 0.8467; More…

Intraday bias in USD/CHF remains on the downside as current selloff accelerates again. Break of 161.8% projection of 0.9196 to 0.8757 from 0.8854 at 0.8144 will target 200% projection at 0.7976 next. On the upside, above 0.8358 support turned resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, the break of 0.8332 (2023 low) confirms resumption of long term down trend from 1.0342 (2017 high). Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075. Firm break there will target 100% projection at 0.7382.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more