Markets Treading Cautiously, As PMIs And Jackson Hole Awaited

As a fresh week unfolds, global markets seem to tread cautiously, keeping a close watch on the recent undertakings in Asian economies. PBoC’s modest rate cut decision has catalyzed a minor pullback in stocks across China and Hong Kong. In contrast, Japan’s Nikkei shows modest gains, reflecting a divergence in Asian market sentiment. The offshore Chinese Yuan wavers but stays above last week’s low against Dollar.

In the currency sphere, Australian and New Zealand dollars are registering mild declines alongside the greenback. On the flip side, Canadian dollar, Euro, and Swiss Franc exhibit a modest uptick. However, any drastic movement in major currency pairs are yet to be seen, with almost all major pairs and crosses stuck inside Friday’s range.

Investors should gear up for a potentially subdued trading ambiance in the next couple of days, given the sparse economic calendar. Nevertheless, Wednesday promises some action with release of PMIs from pivotal economies and Canadian retail sales data. Undoubtedly, the week’s crescendo will be the eagerly awaited annual Jackson Hole symposium, culminating in Fed Chair Jerome Powell’s address.

Technically, WTI crude oil recovers notably today and appears to have defended 78.72 near term support well on first attempt. The development keeps near term outlook neutral at worst, with prospect of resuming the larger rise from 63.67 through 84.91 resistance towards 90 handle at a later stage. However, firm break of 78.72 support, will argue that this rebound has completed, and bring deeper fall back to 74.74 resistance turned support, probably together with deterioration in risk sentiment elsewhere.

In Asia, at the time o writing, Nikkei is up 0.61%. Hong Kong HSI is down -1.38%. China Shanghai SSE is down -0.38%. Singapore Strait Times is down -0.45%. Japan 10-year JGB yield is up 0.012 at 0.643.

NZ exports down -14% yoy in Jul, imports down -16% yoy, China leads the falls

July 2023 has been a challenging month for New Zealand’s trade scenario, as the island nation witnessed a steep fall in both goods exports and imports. Data released depicted a substantial decline, with exports plunging by NZD -890m or -14% yoy, concluding at NZD 5.5B. Concurrently, imports saw a -16% yoy decline, falling NZD -1.2B to settle at NZD 6.6B for the month. This decrease in trade volumes culminated in a monthly trade deficit of NZD -1.1B. This significantly overshadows market expectations of NZD -0.05B.

Zooming in on the country-by-country trade details, China conspicuously led the downturn in both exports and imports. New Zealand’s exports to the Asian giant dipped by -24% yoy, translating to a decline of NZD -407m while imports reduced by a staggering NZD -427m, down -25% yoy.

However, not all trade relations showed a contraction. Australia the US emerged as silver linings, with their exports experiencing an upward trajectory. Exports to Australia saw an 8.9% yoy growth, adding NZD 59m to the tally, and US followed suit with a 16% yoy rise, upping the figure by NZD 105m.

Yet, as New Zealand engaged with its other major trade partners, the news wasn’t all positive. European Union and Japan both registered a decrease in exports, declining by -16% yoy (NZD -73m) and -21% yoy (NZD -84m) respectively. On the import front, while USA and South Korea posted a rise of 24% (NZD 166m) and 18% (NZD 71m), both European Union (up 1.9% yoy) and Australia (down -2.7% yoy) experienced mixed results.

China cuts 1-yr LPR moderately, keeps 5-yr LPR unchanged

In a somewhat anticipated move, China’s PBoC made a cut to its one-year loan prime rate by 10bps, settling it at 3.45%. This is a slight deviation from the 15bps reduction that the majority of economists had forecasted. What stands out is that this marks the second reduction in this rate in just a span of three months.

However, eyebrows were raised when PBOC decided to keep its five-year LPR — the benchmark for most mortgages in the country — steady at 4.2%. This move defied expectations of a 15 bps cut by many market watchers. The unaltered five-year LPR is being read by many as a signal of Chinese banks’ hesitancy to compromise their rate differential margin. Such reluctance throws into sharp relief potential concerns about the effective transmission of PBOC’s policy decisions into the broader market landscape.

Furthermore, it stirs up conversations about the central bank’s capability to invigorate the property sector and the broader economy through monetary easing strategies. This narrative is all the more potent given that this decision on the one-year LPR came on the heels of an unexpected reduction in PBOC’s medium-term policy rate just a week earlier. To give specifics, PBOC had reduced the one-year medium-term lending facility rate by 15 basis points, bringing it down to 2.50% from its previous 2.65%.

Considering these rate adjustments, many financial experts are now projecting more proactive measures from the PBOC in the forthcoming months. This may encompass further rate trims as well as potential reductions in the reserve requirement ratio for banks.

Fed Powell’s balancing act at Jackson Hole in focus

As the financial world turns its gaze towards the Annual Jackson Hole Symposium from August 24-26, expectations are mounting on the discussions surrounding “Structural Shifts in the Global Economy.” This renowned gathering, drawing in elite central bankers from across the globe, stands as a barometer for gauging the future trajectory of monetary policies.

The spotlight is set to shine brightest on Fed Chair Jerome Powell’s speech this Friday. The backdrop is intriguing. On one hand, post-July FOMC meeting data reveals easing pressures on prices and wages in the US, tilting the scales towards concluding the ongoing tightening phase. On the other, the undeniable vitality in labor markets coupled with robust consumer spending suggests that price pressure isn’t backing down anytime soon. Market stakeholders will be keen to dissect how Powell balances these contrasting narratives in his address.

Yet, for those expecting a seismic shift in Fed’s stance, disappointment might be on the horizon. The overarching narrative is likely to remain consistent – a commitment to combating inflation, while leaving the door ajar for a potential September rate hike. It’s also prudent to remember that decision-makers at Fed will have another round of CPI and non-farm payroll data at their disposal before the crucial FOMC verdict on September 20. As for hints on the timing of inaugural rate cut, Powell is anticipated to toe the line, emphasizing the need for interest rates to remain restrictive for as long as the situation demands.

While Powell’s speech will be the main event, it’s the off-stage whispers that could provide invaluable insights. Observers should attune their ears to the informal comments from other Fed officials. Their words might just offer a glimpse into the hawkish vs. dovish balance within the committee.

Amidst the Jackson Hole fervor, the broader economic calendar for the week seems relatively subdued, characteristic of the last full week of August. Yet, there are some metrics worth the watch. PMI figures from the heavyweights – Australia, Japan, Eurozone, UK, and US – are poised to dominate headlines. With the services sector being the bulwark of major economies, even as manufacturing grapples with recessionary winds, any signs of fading momentum here could spark concerns. The looming question: How soon before the manufacturing downturn spills over to services?

Beyond PMIs, analysts will also be tracking US durable goods orders, Germany’s Ifo business climate index, Canada’s retail sales, and New Zealand’s trade balance and retail metrics. All in all, an eventful week beckons for financial market aficionados.

Here are some highlights for the week:

- Monday: New Zealand trade balance; Germany PPI; Canada new housing price index.

- Tuesday: Swiss trade balance; UK public sector net borrowing; Eurozone current account; US existing home sales.

- Wednesday: New Zealand retail sales; Australia PMIs; Japan PMIs; Eurozone PMIs; UK PMIs; Canada retail sales; US PMIs, news home sales.

- Thursday: US jobless claims, durable goods orders.

- Friday: Japan Tokyo CPI, corporate services prices; Germany GDP final, Ifo business climate; US U of Michigan consumer sentiment final.

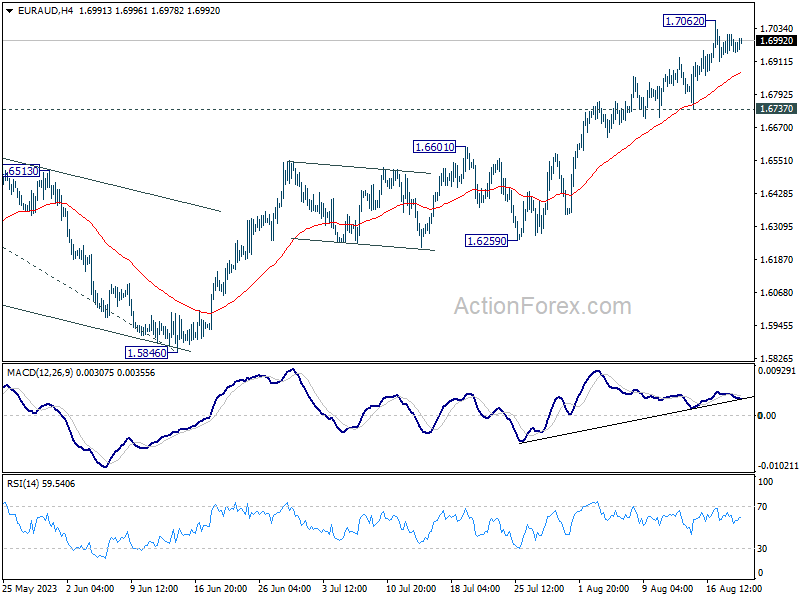

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6944; (P) 1.6980; (R1) 1.7015; More…

Intraday bias in EUR/AUD is turned neutral first as consolidation from 1.7062 temporary top is extending. Further rally is expected as long as 1.6737 support holds. Break of 1.7062 will resume larger up trend from 1.4281 to 1.7377 projection level.

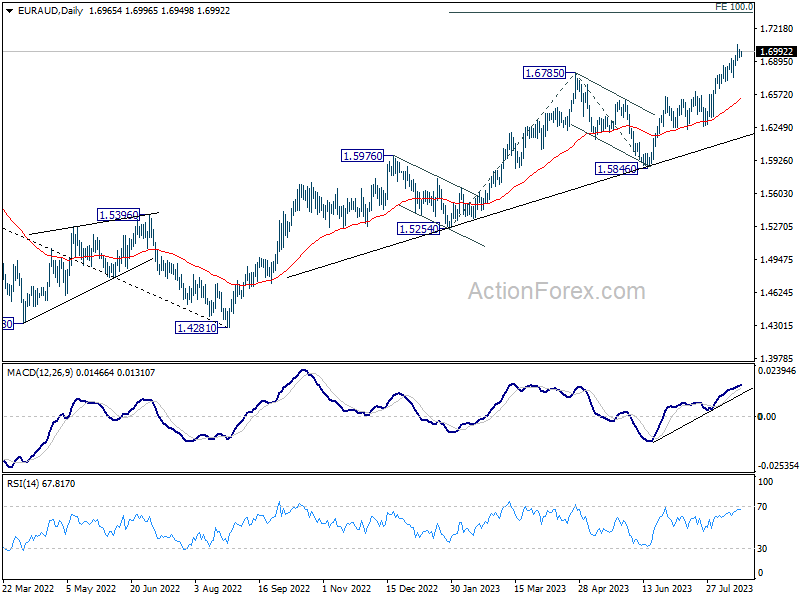

In the bigger picture, the rise from 1.4281 (2022 low) is in progress. Next target is 100% projection of 1.5254 to 1.6785 from 1.5846 at 1.7377. For now, outlook will stay bullish as long as 1.5846 support holds, even in case of another pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Jul | -1107M | -50M | 9M | -111M |

| 23:01 | GBP | Rightmove House Price Index M/M Aug | -1.90% | -0.20% | ||

| 06:00 | EUR | Germany PPI M/M Jul | -0.20% | -0.30% | ||

| 06:00 | EUR | Germany PPI Y/Y Jul | -5.10% | 0.10% | ||

| 12:30 | CAD | New Housing Price Index M/M Jul | 0.00% | 0.10% |

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more