Markets Stabilize Ahead Of Tariff D-Day, Focus Turns To Eurozone CPI And ISM Manufacturing

The global equity selloff appears to have passed its peak—at least for now. After days of heavy risk-off moves driven by fears surrounding the upcoming US reciprocal tariffs announcement on Wednesday, traders have taken a cautious step back into a wait-and-see mode. US indexes clawed back most of their earlier losses overnight, closing mixed. Asian markets followed with mild gains in early Tuesday trading.

Currency markets, meanwhile, are staying largely range-bound in Asian session. Despite the calm surface, risk aversion remains evident in the performance breakdown. Kiwi, Aussie, and Loonie are still the worst performers for the week so far. On the flip side, Yen and Dollar are leading the pack, followed by Euro. Sterling and Swiss Franc are holding middle ground.

A major focus for today will be Eurozone’s flash CPI data. Recent media reports have revealed that some ECB officials are warming up to the idea of pausing rate cuts at the upcoming meeting on April 17. Odds now stand at around 65% for another 25bps reduction. While the doves remain committed to further easing, many appear willing to skip a meeting if hawks insist on more time to assess evolving risks. Any upside surprise in today’s inflation print would strengthen the hawkish camp and make a pause more likely.

US ISM Manufacturing Index will also draw much attention. After briefly returning to expansion territory for just two months, the index is expected to slip back into contraction. Beyond headline activity, the price component will be scrutinized, especially in light of the impending tariffs. Prices index has surged from around 50 to over 60 this year—further acceleration could signal inflationary pressures re-emerging on the supply side.

Technically, EUR/CHF is worth a watch today, considering the impact of Eurozone inflation data. Rebound from 0.9486 is gathering some upside momentum. Break of 0.9581 resistance will argue that correction from 0.9660 has already completed, after drawing support from 0.9489. Further rise should then bee seen through 0.9660 to resume the whole rally from 0.9204.

In Asia, at the time of writing, Nikkei is up 0.29%. Hong Kong HSI is up 0.53%. China Shanghai SSE is up 0.36%. Singapore Strait Times is down -0.07%. Japan 10-year JGB yield is up 0.015 at 1.503. Overnight, DOW rose 1.0%. S&P 500 rose 0.55%. NASDAQ fell -0.14%. 10-year yield fell -0.009 to 4.246.

RBA stands pat, inflation eases as expected, but outlook clouded

RBA kept the cash rate target unchanged at 4.10% today, in line with broad market expectations. While the central bank welcomed the continued decline in underlying inflation, it emphasized a “cautious” stance due “risks on both sides”.

Recent data suggests inflation is easing in line with forecasts, but RBA reiterated that it needs greater confidence that this trend will continue sustainably toward the midpoint of the 2–3% target band.

RBA highlighted “notable uncertainties” around domestic consumption and labor market dynamics. Internationally, there are concerns over the escalating US tariff policy, noting that such developments are already affecting global confidence.

The risk of further tariff expansion or retaliatory measures from other countries could amplify the drag on global activity. Inflation could move in “either direction” depending on how households and firms react to the shifting macroeconomic environment.

Japan’s Tankan survey flags manufacturing caution, services hit 33-year high

Japan’s Q1 Tankan survey revealed a mixed outlook for the economy, with sentiment among large manufacturers slipping for the first time in a year. The index fell from 14 to 12, in line with expectations, as steel and machinery producers grew more cautious amid weak global demand, rising input costs, and uncertainty surrounding US tariff policy.

However, manufacturing outlook ticked down just slightly to 12, beating expectations of a sharper decline to 9, indicating that businesses remain cautiously optimistic.

In contrast, Japan’s services sector showed remarkable resilience. The large non-manufacturing index rose from 33 to 35—marking the highest level since 1991. Still, the outlook component was flat at 28, slightly missing forecasts of 29.

Capital expenditure plans were also encouraging, with large firms expecting a 3.1% increase for fiscal 2025, ahead of consensus of 2.9%.

Japan PMI manufacturing finalized at 48.4, weaker domestic and international demand

Japan’s manufacturing sector contracted further in March, with final PMI reading falling to 48.4 from February’s 49.0, marking the lowest level in a year.

According to S&P Global, both output and new orders declined more sharply, reflecting “weaker demand from both domestic and international clients”. Employment offered a rare bright spot, as firms increased hiring at the fastest rate in three months.

However, confidence remained muted and below the long-run average. Cost pressures also persisted, with strong increases in both input costs and selling prices, suggesting that “inflationary pressure across the sector remains acute”.

China Caixin manufacturing rises to 51.2, jobs and prices Lag

China’s Caixin PMI Manufacturing rose to 51.2 in March, up from 50.8 and marking a four-month high.

According to Wang Zhe of Caixin Insight Group, the upbeat print points to a steady start to the year, suggesting broader signs of recovery in the industrial sector.

Still, challenges remain beneath the surface. The labor market “remained relatively sluggish”. In addition, “deflationary pressures persisted”, driven by weak domestic demand and cautious sentiment among market participants.

Fed’s Williams: Tariff impacts on inflation could linger for years

New York Fed President John Williams cautioned that the inflationary effects of new US tariffs could be “more prolonged” than initially anticipated.

In an interview with Yahoo Finance, Williams emphasized that while the immediate price increases are expected, the true impact of tariffs “might not be fully felt for a couple of years.”

He stressed the importance of monitoring not just the direct price changes, but also the “indirect effects” that ripple through the broader economy over time.

“It is still early days to be able to come to a concrete conclusion around this,” Williams said, noting that Fed will need to remain open-minded about “how long these last in terms of their effects on inflation and the economy.”

Fed’s Barkin: Tariffs create dual risks for inflation and jobs

Richmond Fed President Thomas Barkin highlighted growing concerns over the economic impact of the Trump administration’s upcoming tariffs. He told CNBC that the tariffs could both stoke inflation and weigh on the labor market.

“Call me nervous on both,” Barkin said, signaling that the path forward for monetary policy remains highly data-dependent.

Barkin emphasized “there’s a lot of uncertainty right now, and I think that makes the case for wait and see how this plays out.”

Looking ahead

Eurozone CPI flash is the main focus in European session. Eurozone will release unemployment rate and PMI manufacturing final. UK will release PMI manufacturing final. Swiss will release retail sales and PMI manufacturing. Later in the day, US ISM manufacturing is the main focus. Canada will also release PMI manufacturing.

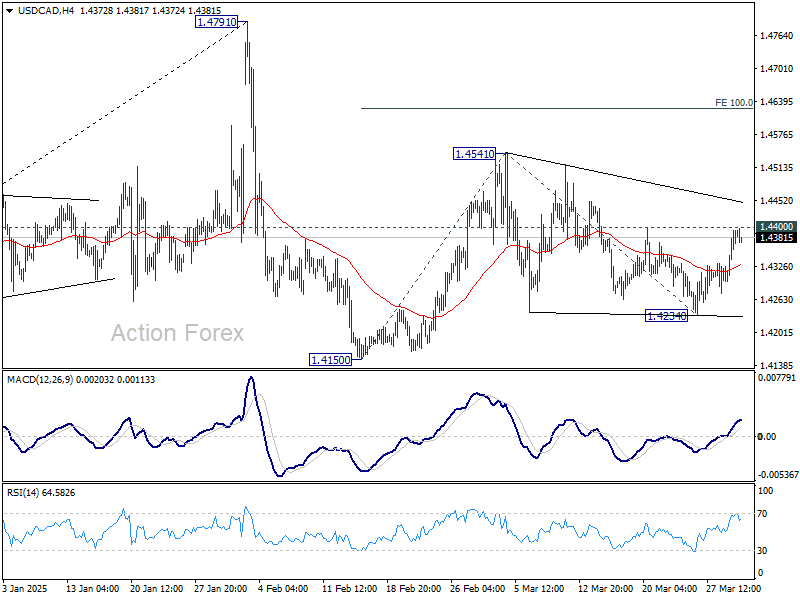

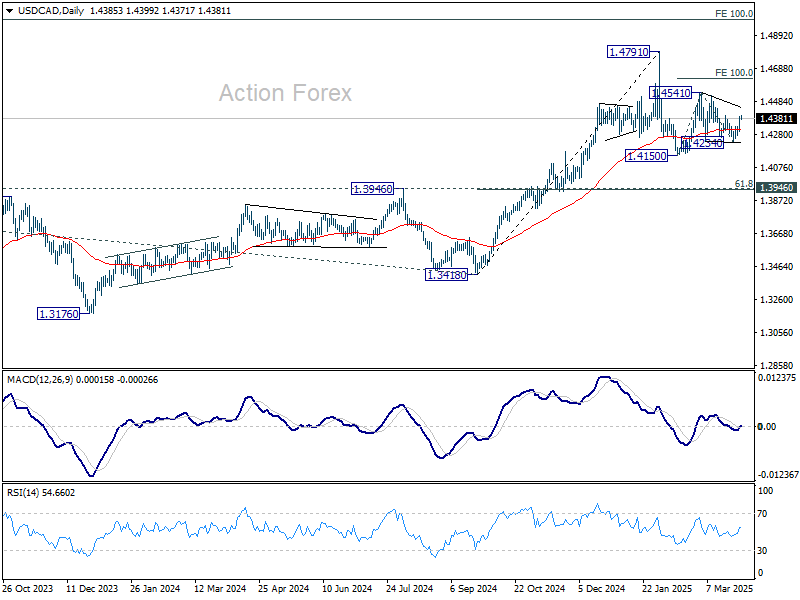

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4327; (P) 1.4361; (R1) 1.4424; More…

Intraday bias in in USD/CAD remains neutral at this point. Overall, corrective pattern from 1.4791 is still extending. On the upside, break of 1.4400 will argue that it’s still in the second leg. Intraday bias will be turned back to the upside fro 1.4541 resistance first, and then 100% projection of 1.4150 to 1.4541 from 1.4234 at 1.4625. On the downside, though, break of 1.42324 support will suggest that the third leg has already started for 1.4150 and below.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned support holds (2022 high), even in case of deep pullback.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more