Markets Driven By PMI Data And Tariff Speculations, Silver At Risk Of Reversal

Market sentiment today is largely influenced by a mix of global PMI releases and ongoing uncertainty around US tariff policy. There are reports suggesting the Trump administration may exclude a set of sector-specific tariffs from the sweeping reciprocal levies set to begin on April 2. US futures are pointing to a solid open, suggesting investors are hoping for a more surgical, less disruptive approach to trade action.

However, clarity is still lacking. It’s unclear whether excluded sectors will be spared entirely or if reciprocal tariffs will blanket all imports, with sectoral levies added on top later. Despite the ambiguity, sentiment has been lifted, with US futures pointing to a solid open.

European currencies are also finding some support alongside gains in regional equities. However, upside in both Euro and Sterling is capped by mixed PMI data. In the Eurozone, manufacturing showed a smaller contraction and even a bounce in output, signaling green shoots. Yet, service sector growth lost momentum, adding to the sense of an uneven recovery. In the UK, services surprised with strong growth, but manufacturing activity deteriorated sharply, dragging down the overall tone of the report.

Meanwhile, Australia outperformed, with both sectors registering improvements and supporting Aussie’s strength today. On the other hand, Yen is under pressure as Japan’s services PMI fell into contraction territory, raising concerns about domestic demand and the broader economic outlook.

Currency performance reflects this divergence. Aussie is currently the strongest performer for the day, followed by Sterling and Swiss Franc. At the bottom of the table, Yen leads losses, followed by Kiwi and Dollar. Loonie and Euro sit in the middle of the pack.

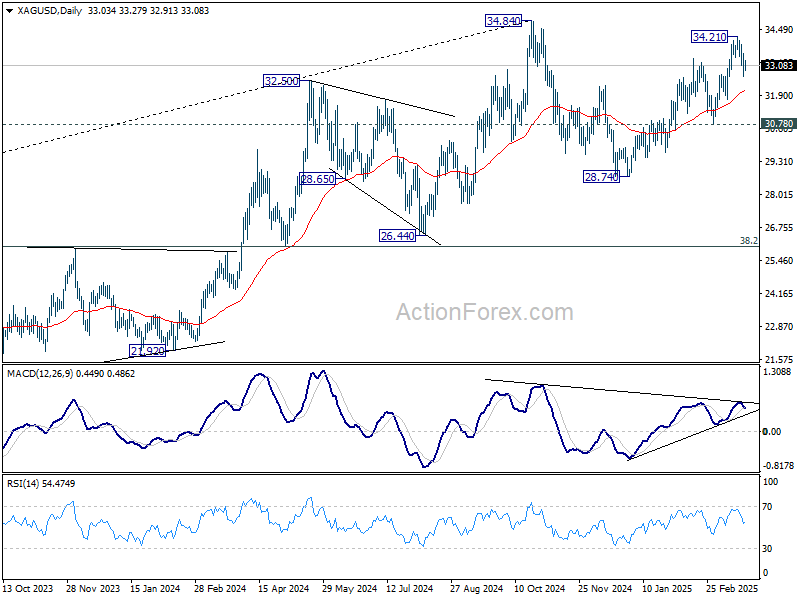

Technically, Silver could have formed a short term top at 34.21, ahead of 34.84 resistance. Break of 55 D EMA (now at 32.07) will suggest that rebound from 28.74 has already completed. Further break of 30.78 support will indicate that corrective pattern from 34.84 has already started the third leg back to 28.74 support and possibly below.

In Europe, at the time of writing, FTSE is down -0.22%. DAX is down -0.06%. CAC is down -0.12%. UK 10-year yield is up 0.001 at 4.723. Germany 10-year yield is up 0.028 at 2.797. Earlier in Asia, Nikkei fell -0.18%. Hong Kong HSI rose 0.91%. China Shanghai SSE rose 0.15%. Singapore Strait Times rose 0.25%. Japan 10-year JGB yield rose 0.028 to 1.545.

UK PMI manufacturing falls to 44.6, while services rises to 53.2

UK delivered a mixed set of PMI readings in March, with services providing a welcome surprise as the index rose from 51.0 to 53.2, a 7-month high. PMI Composite also improved from 50.5 to 52.0, suggesting modest expansion. However, the picture was clouded by a sharp deterioration in manufacturing, where the index slumped from 46.9 to 44.6 — its lowest level in 18 months.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, cautioned against over-optimism, noting that “one good PMI doesn’t signal a recovery.”

The data points to the economy barely expanding, with GDP growth tracking around 0.1% for the quarter. Employment continues to be trimmed as firms remain wary of rising costs and an uncertain economic outlook, with business confidence still hovering near January’s two-year low.

Looking ahead, challenges appear to be mounting. Businesses are bracing for higher National Insurance contributions starting in April,. Additionally, the anticipated unveiling of US tariff policy on April 2 adds another uncertainty.

ECB’s Cipollone: Case for rate cuts strengthens amid falling energy, rising Euro and trade risks

ECB Executive Board member Piero Cipollone struck a dovish tone in an interview with Expansión, signaling that recent developments have reinforced the case for further interest rate cuts.

Cipollone noted that at the time of the March meeting, ECB projections already showed inflation converging to the 2% target by early 2026—even under a rate path that included market expectations of cuts below 2%.

Since then, “not only has this narrative been confirmed, but key issues have arisen that have strengthened the arguments in favour of continuing to lower rates”, he added.

Cipollone noted that energy price pressures have already begun to reverse. Meanwhile, Euro appreciation and higher real interest rates are working in tandem to cool price growth.

If US tariffs on European goods materialize, that would have a “negative impact on demand”, which would “further strengthen the downward trend in inflation”. Similarly, escalating U.S.-China trade conflict may push Chinese goods into Europe, adding to price suppression across the bloc.

Notably, Cipollone suggested that inflation could reach target even sooner than the ECB’s latest projections anticipate.

Eurozone PMI hints at green shoots, manufacturing leads the way

Eurozone PMI data for March offered fresh signs of economic stabilization, with Composite index rising to a 7-month high of 50.4, supported by a notable rebound in manufacturing. The PMI Manufacturing rose from 47.6 to 48.7, its highest level in 26 months. Manufacturing output crossed into expansion territory at 50.7, a 34-month high. Services PMI slipped slightly from 50.6 to 50.4, but remained in growth territory.

Cyrus de la Rubia of Hamburg Commercial Bank noted the possibility that “temporary tariff-related import boom” could be inflating manufacturing figures. But he also expressed optimism that with, Europe’s investment drive in defense and infrastructure, “hope for a more sustained recovery seems well founded”.

Encouragingly for ECB, pricing pressures in the services sector are easing, with both input costs and output prices decelerating. In manufacturing, price pressures remain moderate as well, helped by falling energy costs.

However, risks remain. Potential retaliation tariffs from the US, trade tensions with China, and higher food prices caused by extreme weather events are all sources of uncertainty that could cloud the outlook and “make some ECB members hesitant to cut rates too aggressively.”

BoJ’s Ueda reaffirms commitment to rate hikes despite market and financial pressures

BoJ Governor Kazuo Ueda told parliament today that the central bank remains committed to raise interest rate if underlying inflation is deemed to be approaching its 2% target.

He emphasized that BoJ’s objectives remain squarely focused on price stability, and that its approach to policy “would not be disturbed by considerations for the BoJ’s finances.”

Ueda’s remarks come as concerns mount over the BoJ’s balance sheet in light of interest rate hikes and volatility in equity markets.

BoJ estimated in December that if short-term borrowing costs were to rise to 2%, it could incur losses of up to JPY 2 trillion.

Additionally, Ueda noted that a 1000-point drop in the Nikkei 225 index would translate into a valuation loss of about JPY 1.8 trillion in its ETF holding.

While these figures highlight the scale of financial risks, Ueda’s insistence on prioritizing price stability signals that BoJ is prepared to weather market volatility in pursuit of its monetary policy mandate.

Japan PMI composite falls to 48.5, business confidence sinks to lowest since 2020

Japan’s private sector saw a sharp loss in momentum at the end of Q1, with PMI Composite falling from 52.0 to 48.5, marking the first contraction in five months. PMI Manufacturing dropped from 49.0 to 48.3, its lowest in a year and ninth consecutive month in contraction. More concerning was the steep decline in PMI services, which fell from 53.7 to 49.5 — the weakest reading since mid-2024.

According to Annabel Fiddes of S&P Global, the downturn was driven by a “fresh fall in service sector activity” and an accelerated decline in manufacturing. Firms pointed to “strong inflationary pressure had dampened sales”, with clients showing increasing hesitation to place orders.

The broader picture is one of growing pessimism. Japanese firms cited a host of structural and cyclical challenges — from persistent inflation and labor shortages to an aging population and deepening global trade uncertainty. As a result, business confidence for future activity fell to its lowest level since August 2020.

Australia’s PMI manufacturing jumps to 52.6, services rises to 51.2

Australia’s PMI Manufacturing surged to 52.6 from 50.4—marking a 29-month high—while PMI Services ticked up to 51.2 from 50.8. PMI Composite , which combines both sectors, rose to a 7-month high at 51.3.

Jingyi Pan of S&P Global Market Intelligence highlighted that the output growth was not only the strongest in seven months but also “broad-based” across both manufacturing and services. Despite a decline in export orders due to weather disruptions and weak global conditions, domestic demand rebounded impressively, pushing new orders to their highest growth rate in nearly three years.

However, the report also highlighted a notable dip in business confidence. Suppressed price increases may have helped support near-term demand. But “tariff uncertainty may continue to cast a shadow on output growth in the year ahead”.

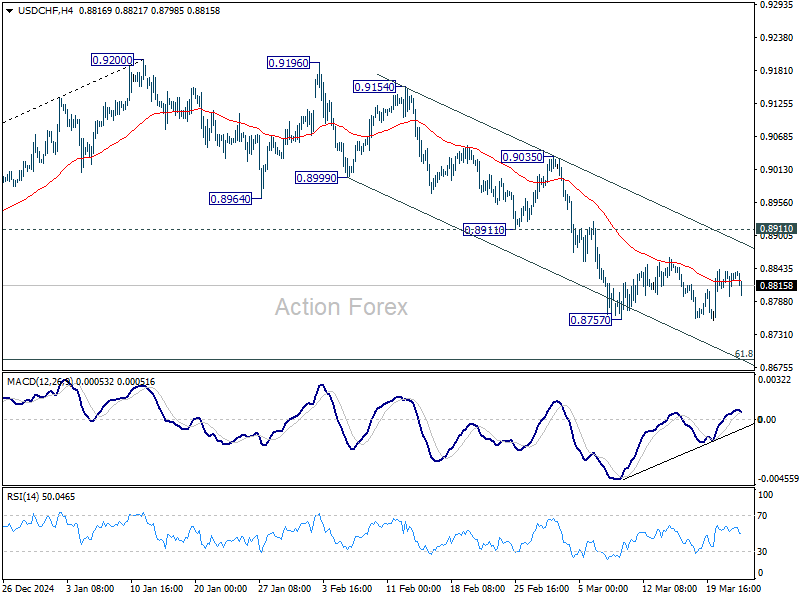

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8805; (P) 0.8823; (R1) 0.8849; More…

No change in USD/CHF’s outlook as consolidations continue in established range above 0.8757. In case of stronger recovery, upside should be limited by 0.8911 support turned resistance. On the downside, break of 0.8757 will resume the fall from 0.9200 to 61.8% retracement of 0.8374 to 0.9200 at 0.8690. Sustained break there will pave the way back to 0.8374 support.

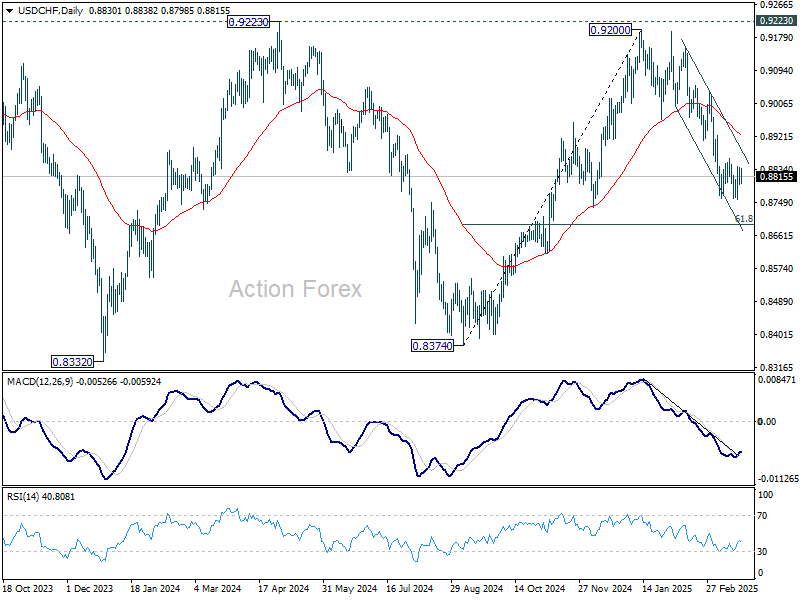

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more