Investors Await Clarity As Trumps Trade Plan Nears Unveiling

Risk-off sentiment has returned to European markets and US futures as traders await the long-anticipated announcement of the United States’ reciprocal tariffs, scheduled for 2000 GMT. After months of speculation and political posturing, today is expected to bring the concrete details of US President Donald Trump’s sweeping reciprocal tariffs plan. Markets are hoping for clarity on which countries and sectors will be affected, the magnitude of the levies, when they will take effect, and whether any exemptions will be granted.

While the announcement itself may provide clarity to a certain extent, hopefully, it’s far from the end of the story. A big unknown remains how major trading partners, especially the European Union, will respond. Retaliatory measures are expected, but the scale, scope, and timing remain uncertain. And beyond that, markets are already looking to Washington’s next move—will the US escalate further if other nations push back?

On the more hopeful side, many still believe that this will eventually culminate at the negotiating table, where barriers are eased rather than raised. Historically, tariff wars have led to tough talks and eventual compromises. However, any such diplomatic resolution would likely be a long process and do little to ease near-term volatility or economic strain.

Pessimists, on the other hand, are concerned that the true aim of the US isn’t merely reciprocity, but reshoring manufacturing and breaking long-standing trade norms. These goals require very different approaches and outcomes. The former could lead to quick concessions, the latter a prolonged and potentially damaging realignment of global supply chains.

There is a chance of a short-term relief rally in stocks if today’s announcement is less severe than feared. However, any bounce could be short-lived. For S&P 500, downside risks remain dominant as long as 5786.95 resistance holds. The larger corrective fall from 6147.47 would still be in play. Next target would be 38.2% retracement of 3491.58 to 6147.47 at 5132.89 after the recovery, if any, completes.

In currency markets, Kiwi and Aussie are leading today followed by Sterling. while Loonie lags behind at the bottomed, followed by Dollar, and Swiss Franc. Euro and Yen are positioning in the middle.

In Europe, at the time of writing, FTSE is down -0.87%. DAX is down -1.63%. CAC is down -0.91%. UK 10-year yield is down -0.043 at 4.609. Germany 10-year yield is down -0.036 at 2.661. Earlier in Asia, Nikkei rose 0.28%. Hong Kong HSI fell -0.02%. China Shanghai SSE rose 0.05%. Singapore Strait Times fell -0.37%. Japan 10-year JGB yield fell -0.025 to 1.479.

US ADP jobs grow 155k, pay growth cools further

US ADP private sector employment rose by 155k in March, exceeding expectations of 120k. There were 24k positions added in goods-producing sectors and 132k in services.

Employers of all sizes contributed to the growth, with small firms leading the way, adding 52k jobs, followed by large and medium-sized businesses with 59k and 43k respectively.

Despite the strong employment numbers, wage growth continued to decelerate. Year-over-year pay gains slowed to 4.6% for job-stayers and 6.5% for job-changers. The premium for switching jobs fell to 1.9 percentage points—the lowest in the series since September.

ADP Chief Economist Nela Richardson commented that despite “policy uncertainty and downbeat consumers,” the headline job number was a positive indicator for the economy and businesses of all sizes.

ECB’s Lagarde: Tariffs harmful globally, often lead back to negotiation table

ECB President Christine Lagarde warned that the global effects of US-led tariffs will be “negative,” though the extent of the damage depends heavily on the scope, duration, and targeted products.

In an interview with Ireland’s Newstalk radio, she emphasized that the broader implications for global trade and growth would vary, but the potential for lasting disruption is real.

Lagarde also noted that history shows such trade escalations often end in talks rather than prolonged battles.

“Quite often those escalation of tariffs, because they prove harmful, even for those who inflict it, lead to negotiation tables,” she said, suggesting that any initial damage might eventually give way to diplomatic resolutions and the removal of trade barriers.

ECB’s Schnabel: Trade fragmentation risks rekindling inflation, hitting growth

ECB Executive Board member Isabel Schnabel warned today that a global trade war could cause a sharp resurgence in inflation and weigh heavily on growth.

In a speech, she highlighted that a severe disruption in global trade flows could lift inflation by several percentage points in the early years.

She added that even a “mild decoupling” scenario would still have a meaningful impact—adding up to 1% to inflation and taking years to unwind.

BoJ’s Ueda: US tariffs pose short-term inflation risk, long-term growth uncertainty

BoJ Governor Kazuo Ueda said today that the ramifications of US tariff policy remain “highly uncertain” and could significantly affect global trade.

Speaking to Japan’s parliament, Ueda emphasized that the ultimate impact would depend on the “range and scale” of the tariffs being implemented. He also noted that beyond trade flows, a key concern lies in “how the tariffs could affect the sentiment and spending of households and companies.”

Ueda further highlighted that while US inflation may rise in the short term due to higher import costs, the longer-term effect is less predictable. He suggested that elevated tariffs could eventually weigh on US economic growth, which in turn might dampen inflationary pressures over time.

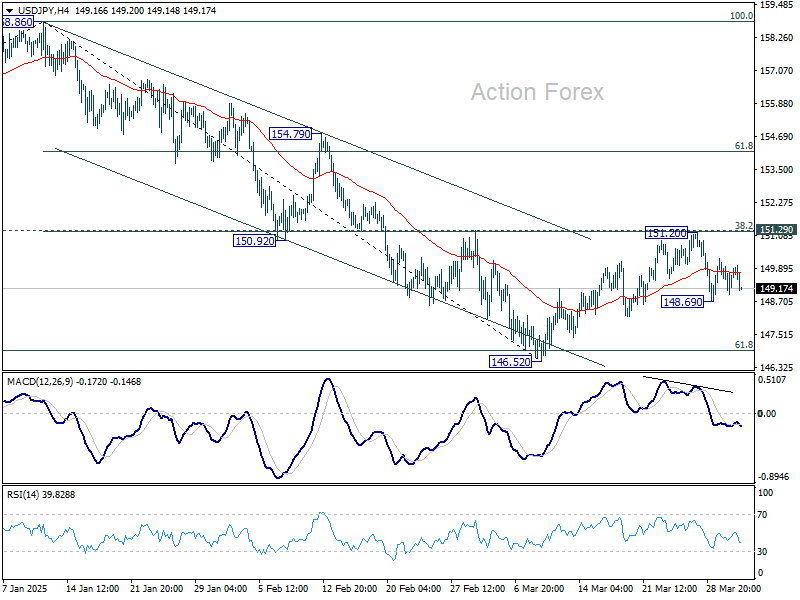

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 149.01; (P) 149.58; (R1) 150.19; More…

Range trading continues in USD/JPY and outlook is unchanged. Intraday bias remains neutral at this point. Corrective rise from 146.52 could have completed at 151.20 already. Risk will stay on the downside as long as 151.29 resistance holds. Below 148.69 will bring retest of 146.52 low first. Firm break there will resume whole decline from 158.86 towards 139.57 support next.

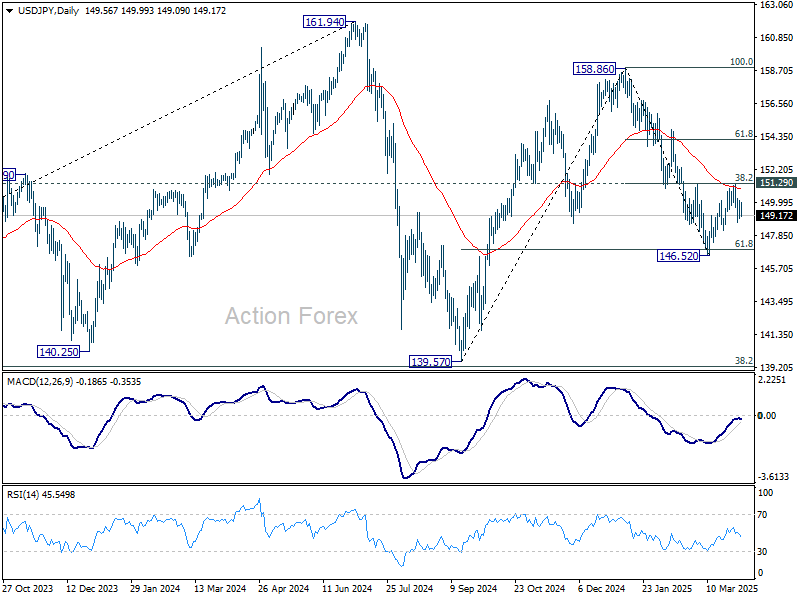

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more