Global Market Rout Deepens Ahead Of US Jobs Data

There’s no relief in sight for the markets as risk aversion extends into Friday’s Asian session. Japan’s Nikkei is leading the losses once again, falling over -3% and cementing a near 10% weekly drop — the worst performance since early 2020. Singapore’s Strait Times Index has finally caught up with the global rout, slumping nearly -3% as traders there digest the full extent of the tariff-driven global selloff. Meanwhile, Hong Kong and China markets are taking a breather, closed for the Ching Ming Festival holiday. But the pause might only delay—not prevent—the contagion, as sentiment across asset continues to sour.

US futures point to more pain ahead, with DOW at risk of closing below the psychological 40k psychological level this week. Markets appear unconvinced that a bottom is in sight, especially with geopolitical uncertainty and trade war escalation clouding the outlook. One of the clearest signs of deepening concern is the move in US Treasury yields. 10-year yield has broken below the critical 4% psychological support during Asian session, for the first time in six months. A weekly close below 4% could mark a seismic shift in sentiment, likely reinforcing safe-haven flows and risk aversion even further.

Today’s U.S. non-farm payrolls report is the marquee event, but its interpretation is unlikely to offer a clear rescue narrative. A strong report won’t necessarily be bullish, as markets are more focused on looming global trade frictions than short-term economic strength. Conversely, a weak NFP print might push Fed rate cut expectations higher, but would also reinforce fears that the economy is already sliding into a downturn. In short, there’s little in this data that could provide comfort in the current climate.

In currencies, despite the steep selloff, Dollar is not the weakest performer this week. That spot goes to the Aussie, followed by the greenback and Kiwi. At the other end, the new safe-haven trio of Swiss Franc, Japanese Yen, and Euro are leading the pack. Sterling and Loonie sit in the middle of the spectrum.

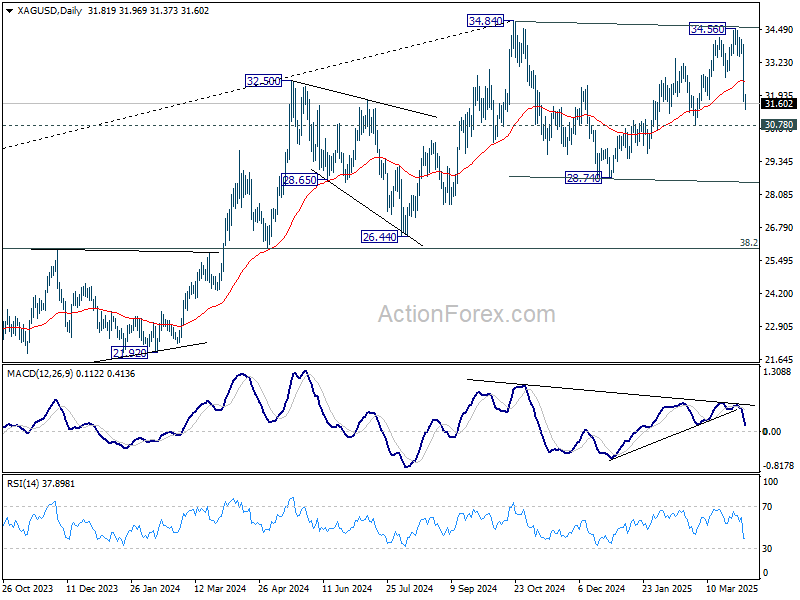

Technically, Silver’s steep decline yesterday indicates that rise from 28.74 has already completed at 34.56, after rejection by 34.84 key resistance. Fall from 34.56 is now seen as the third leg of the corrective pattern from 34.84. Deeper fall should be seen to 30.78 support first. Firm break there will target 28.74 support, and possibly below.

In Asia, at the time of writing, Nikkei is down -3.07%. Japan 10-year JGB yield is down -0.147 at 1.204. Singapore Strait Times is down -2.69%. Hong Kong and China are on holiday. Overnight, DOW fell -3.98%. S&P 500 fell -4.84%. NASDAQ fell -5.97%. 10-year yield fell -0.141 to 4.055.

NFP unlikely to offer relief, miss could cement Q2 fed cut

Today’s US non-farm payrolls report comes as the markets are already reeling from this week’s tariff shock. With consensus expecting a 128k rise in jobs for March and the unemployment rate holding steady at 4.1%, the print itself may not do much to lift sentiment or Dollar, even if it exceeds expectations.

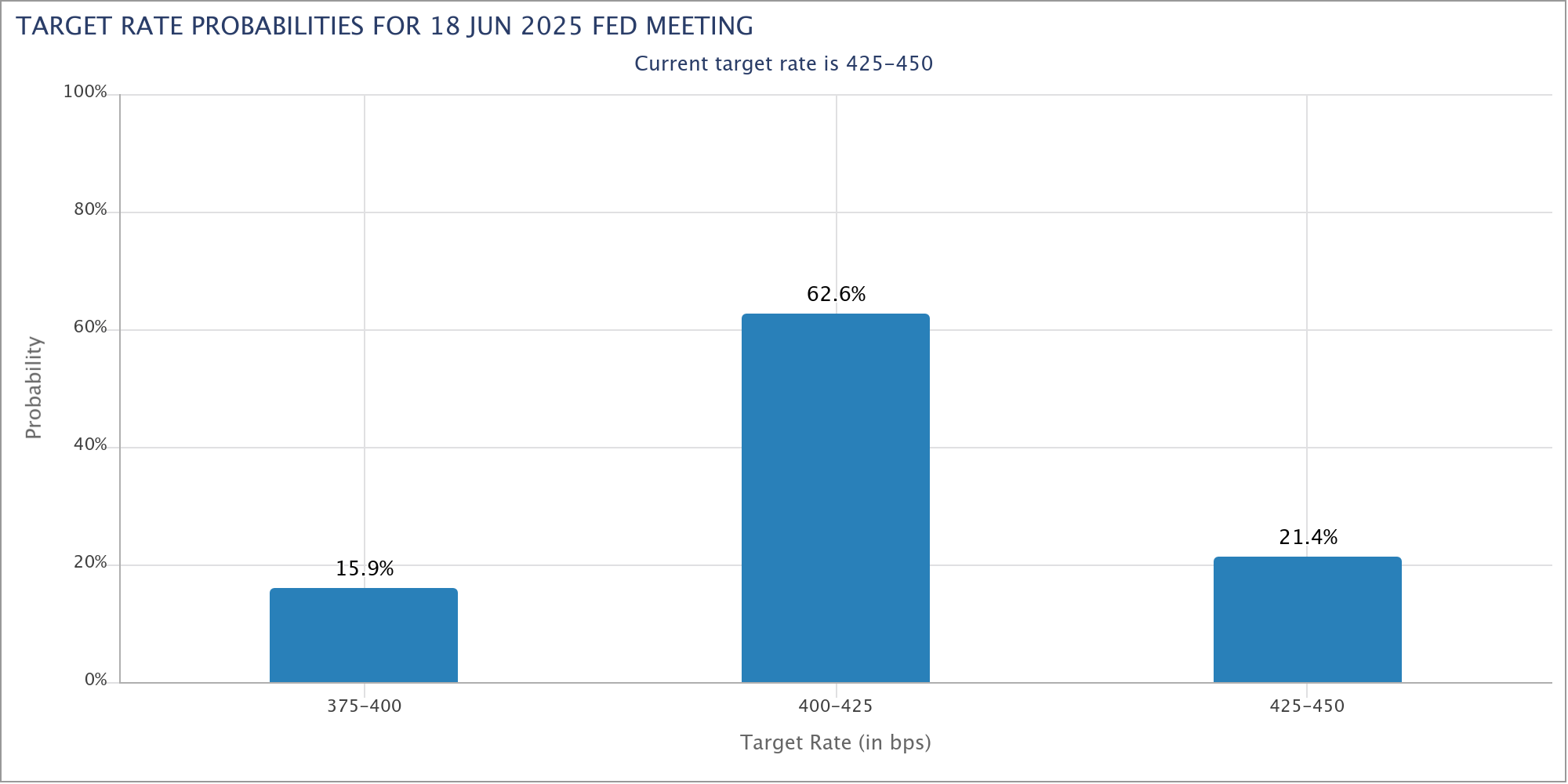

On the other hand, a downside surprise could further shift the odds in favor of a Fed rate cut in Q2. Currently, fed funds futures suggest nearly an 80% probability of a 25bps reduction in June.

While Fed has signaled patience, deteriorating jobs data may leave policymakers with little choice but to move sooner rather than later. Such development would in turn apply further pressure on Dollar.

Recent data paints a murky picture: the employment components in both ISM manufacturing (44.7) and services (46.2) surveys fell deep into contraction in March. ADP report came in at a modest 155k growth.

Whether today’s NFP captures the full extent of that weakness as indicated by ISM data remains to be seen, but the underlying trend is clearly deteriorating.

Fed’s Jefferson: Important to take time and think carefully amid sweeping policy shifts

Fed Vice Chair Philip Jefferson reiterated in a speech overnight that there is “no need to be in a hurry” to adjust policy further. Current policy settings are appropriately positioned amid a period of sweeping changes in trade, immigration, fiscal, and regulatory policies.

He stressed the importance of assessing the “cumulative effect” of these evolving policies before making any shifts in the monetary path.

Commenting on the new of import tariffs announced this week after the formal remarks, Jefferson acknowledged the heightened uncertainty such measures introduce, adding that they could weigh on household sentiment and business investment.

In this environment, Jefferson said it is important to “take our time and think carefully” as it evaluates the broader economic impact.

Fed’s Cook: Risks tilt toward high inflation and slower growth

Fed Governor Lisa Cook highlighted in a speech overnight that her baseline forecast sees the US economy will “slow moderately” this year, with a slight uptick in unemployment. Also, inflation progress will “stall in the near term”, because of tariffs and other policy changes.

Cook acknowledged the potential for a more optimistic scenario in which new policies prove minimally disruptive and consumer demand holds up, allowing for stronger-than-expected growth.

However, she placed “more weight on scenarios where risks are skewed to the upside for inflation and to the downside for growth”.

Given the elevated risks and uncertainty, Cook supports the case to keep interest rates unchanged for now. With both sides of the Fed’s dual mandate facing uncertainty and risks, she stressed that policymakers must remain “patient but attentive”.

BoJ’s Ueda: US tariffs likely to pressure Japan’s economy

BoJ Governor Kazuo Ueda warned that the 24% tariffs imposed by the US on Japanese goods could have broad implications. He emphasized that heightened uncertainty over the economic outlook may weigh on corporate sentiment and trigger volatile market behavior. This, in turn, could place “downward pressure on global and Japanese economies”.

Meanwhile, Ueda noted that the effect on inflation remains uncertain, as the tariffs could either suppress prices by weakening demand or push them higher through supply chain disruptions.

Despite these concerns, Ueda maintained a cautiously optimistic view on Japan’s economy. He pointed out that corporate sentiment remains positive, and capital expenditure plans are stronger than in the same period of prior years.

He referred to the latest Tankan survey as supportive of BoJ’s baseline view that Japan’s economy is “recovering moderately”. Still, Ueda noted that the survey, conducted from late February to March 31, may not have fully captured the impact of the US tariff announcements.

BoJ Deputy Governor Shinichi Uchida, also speaking at the session, reiterated that the central bank remains committed to adjusting rates if the likelihood of achieving its 2% inflation target increases.

Uchida emphasized that future policy decisions will be made on a meeting-by-meeting basis, based on updated forecasts, “without any preconception”.

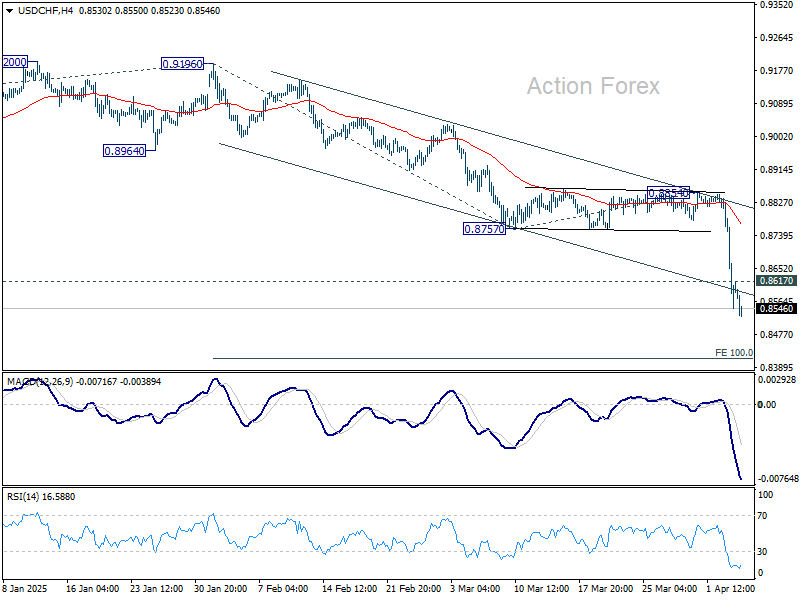

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8483; (P) 0.8658; (R1) 0.8769; More…

USD/CHF’s steep decline is still in progress and there is no sign of bottoming yet. Intraday bias stays on the downside for 100% projection of 0.9196 to 0.8757 from 0.8854 at 0.8415. On upside, above 0.8617 minor resistance will turn intraday bias neutral and bring consolidations. But recover should be limited below 0.8757 support turned resistance to bring another fall.

In the bigger picture, rejection by 0.9223 key resistance keep medium term outlook bearish. That is, larger fall from 1.0342 (2017 high) is not completed yet. Firm break of 0.8332 (2023 low) will confirm down trend resumption. Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more