Euro Rally Extends As German Greens Eye Defense Spending Deal This Week

Euro’s rally continues after a brief pause, boosted by signs of political breakthrough in Germany over major defense and infrastructure spending. Consensus appears to be emerging around the large-scale funding deal, a game-changer toward bolstering Europe’s economic and defense resilience, especially amid ongoing geopolitical conflicts in Ukraine.

Germany’s Green party is reportedly prepared to reach an agreement as early as this week with prospective Chancellor Friedrich Merz of CDU/CSU. Greens co-leader Franziska Brantner indicated in a Bloomberg TV interview that negotiations could move quickly, citing the urgent need for Europe to “speed up” its defense capabilities given the “dire” situation in Ukraine. An influx of hundreds of billions of Euros in spending could act as a significant stimulus for the German economy, thereby supporting the broader Eurozone.

On the other hand, Dollar is generally weaker against European majors, reflecting a cautious mood. US futures are also sluggish, reversing earlier recovery and struggling to find direction in a narrow trading range. Many investors appear to be sidelined, waiting for tomorrow’s CPI release to guide the next market move.

Expectations point to core CPI remaining sticky, albeit with a modest decrease from 3.3% to 3.2%. The pace of disinflation has clearly lost momentum in recent months, suggesting that inflationary pressures are far from fully contained. Should the data confirm a slow decline in inflation, it would solidify Fed’s case to hold rates steady at the upcoming March 19 meeting.

Even so, market participants are increasingly betting that Fed will need to ease policy in Q2, as the economic impact of tariffs and weaker sentiment gradually translate into weaker hard data. The uncertainty surrounding trade policy, coupled with signs of slowing economic momentum, has kept Dollar on the back foot.

Looking at weekly performance, Euro remains the strongest currency so far. British Pound and Yen are also holding up well. On the other end of the spectrum, Canadian Dollar is the worst performer this week, followed by Australian and New Zealand Dollars, as risk sentiment remains weak and commodity-linked currencies struggle. Dollar and Yen are currently positioned in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.09%. DAX is up 0.21%. CAC is up 0.03%. UK 10-year yield is up 0.024 at 4.626. Germany 10-year yield is up 0.046 at 2.883. Earlier in Asia, Nikkei fell -0.64%. Hong Kong HSI fell -0.01%. China Shanghai SSE rose 0.41%. Singapore Strait Times fell -1.88%. Japan 10-year JGB yield fell -0.065 to 1.506.

ECB’s Rehn warns US tariffs could cut global output by 0.5% in both 2025 and 2026

In a speech today, Finnish ECB Governing Council member Olli Rehn highlighted the potential damage that US tariffs could inflict on global economic activity.

According to Bank of Finland estimates, import tariffs of 25% on US imports from the Eurozone and 20% on imports from China, along with reciprocal measures by those regions, would shave more than 0.5% off global output this year and next

Rehn stressed that this looming trade conflict would carry both deflationary and inflationary implications for Europe. “It’s worth recalling that if growth were to slow down in the world economy and euro area economy compared to forecasts, that would weigh on inflation downwards,” Rehn said.

Given this uncertainty, he noted that ECB will assess fresh economic data ahead of its April meeting before committing to additional rate cuts or a pause.

Australia Westpac consumer sentiment jumps to 95.9, soft landing achieved

Australian consumer sentiment saw a strong rebound in March, with Westpac Consumer Sentiment Index jumping 4.0% mom to 95.9, the highest level in three years and not far from neutral 100 mark.

Westpac attributed the improvement to slowing inflation and February’s RBA interest rate cut which have lifted confidence across households. positive views on job security suggest that “soft landing has been achieved”. Nevertheless, “unsettling overseas news” continues to weigh on the broader economic outlook.

Looking ahead to RBA’s upcoming meeting on March 31-April 1, Westpac expects the central bank to keep the cash rate unchanged. RBA was clear that the 25bps cut in February “did not mean further reductions could be expected at subsequent meetings.”

Westpac added, “further slowing in inflation will give the RBA sufficient confidence to deliver more rate cuts this year with the next move coming at the May meeting”.

Australia’s NAB business confidence slips back into negative as cost pressures persist

Australia’s NAB Business Confidence fell from 5 to -1 in February, erasing last month’s gain and returning to below-average levels. While business conditions improved slightly from 3 to 4, the decline in confidence suggests that businesses remain cautious despite RBA’s recent rate cut and positive Q4 GDP data.

NAB Chief Economist Alan Oster noted that the lift in sentiment seen in January was not sustained, signaling ongoing uncertainty in the business environment. Persistent cost pressures and subdued profitability appear to be key factors weighing on sentiment, keeping confidence below long-term norms.

Within business conditions, trading conditions ticked up from 7 to 8, and profitability conditions rose slightly from -2 to -1, though still remaining in negative territory. Employment conditions, however, weakened from 5 to 4.

Cost pressures remain a concern, with purchase cost growth accelerating from 1.1% to 1.5% in quarterly equivalent terms. On the positive side, labor cost growth eased from 1.7% to 1.5%, indicating that wage price pressures are gradually cooling. Meanwhile, final product price growth slowed from 0.8% to 0.5%, though retail price inflation held steady at 1.0%.

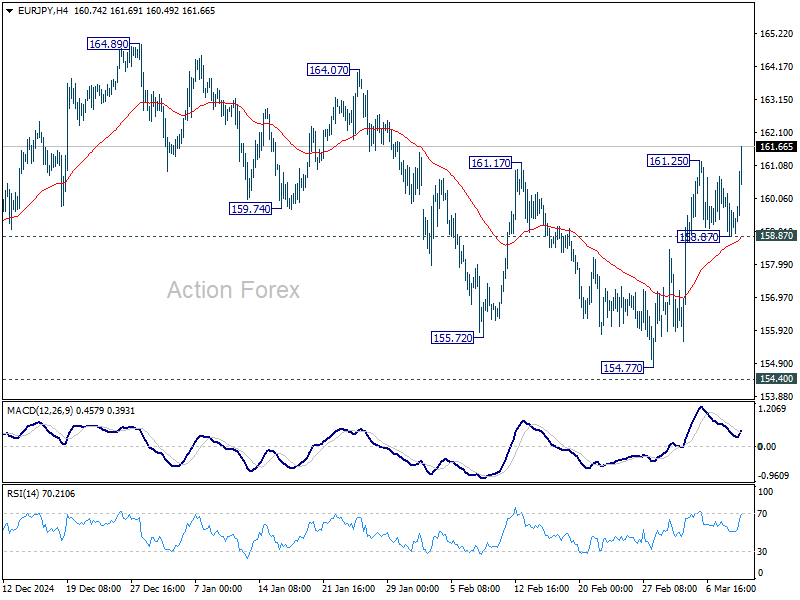

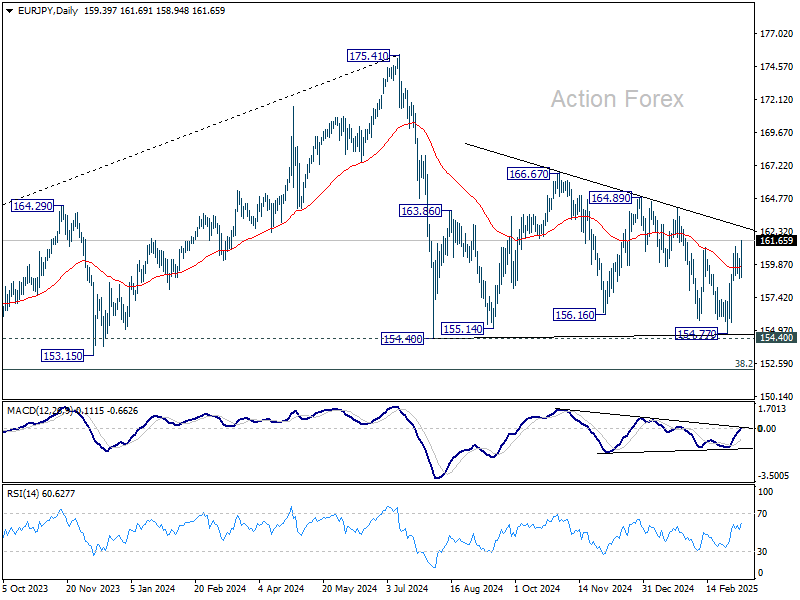

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.86; (P) 159.62; (R1) 160.35; More…

EUR/JPY’s rally resumed by breaking through 161.25 temporary top and intraday bias is back on the upside. Rise from 154.77 is seen as another rising leg in the consolidation pattern from 154.40. Next target is 164.89 resistance. For now, further rise is expected as long as 158.87 support holds, in case of retreat.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more