Euro Holds Gains After ECB Cut, Yen Rallies On Higher JGB Yields

Euro remained firm following ECB’s decision to cut interest rates, a widely anticipated move. During the subsequent press conference, President Christine Lagarde emphasized a shift to “more evolutionary approach” to policy, now that monetary conditions have become “meaningfully less restrictive.” She also acknowledged the high levels of uncertainty, noting that “risks are all over.”

Lagarde welcomed Germany and the EU’s proposed defense and infrastructure investments, highlighting that they could offer broad support for European growth. However, she also cautioned that increased government spending might push inflation higher via rising aggregate demand. At the same time, ECB recognizes downside risks to the economy, particularly if trade tensions escalate, thereby dampening exports and threatening global growth.

Meanwhile, Yen resumed its recent rally against Dollar and recovered against European majors. Support for Yen came from an upswing in Japan’s 10-year JGB yield, which briefly touched 1.515%, its highest level since June 2009. Expectations of another BoJ rate hike this year have fueled speculation, while Germany’s surging benchmark yield also exerts upward pressure on Japan’s yield.

In contrast, U.S. yields are struggling under the weight of growing worries about a “Trumpcession.” Investors fear that the administration’s trade policies could tip the economy toward recession, softening expectations for robust growth and keeping Treasury yields in check. This dynamic contrasts sharply with Europe and Japan, where yields jumped notably this week.

Against this backdrop, Yen stands as the strongest performer for the day so far, followed by Swiss franc and then Euro. Canadian Dollar has taken the opposite position, emerging as the worst performer, trailed by Sterling and Dollar. Australian and New Zealand Dollars are in the middle of the pack.

In Europe, at the time of writing, FTSE is down 01.05%. DAX is up 0.63%. CAC is down -0.30%. UK 10-year yield is up 0.008 at 4.656. Germany 10-year yield up 0.101 at 2.892. Earlier in Asia, Nikkei rose 0.82%. Hong Kong HSI rise 2.47%. China Shanghai SSE rose 0.78%. Singapore Strait Times rose 0.66%. Japan 10-year JGB yield rose 0.053 to 1.499.

US initial jobless claims fall to 221k, vs exp 236k

US initial jobless claims fell -21k to 221k in the week ending March 1, below expectation of 236k. Four-week moving average of initial claims rose 250 to 224k.

Continuing claims rose 42k to 1897k in the week ending February 22. Four-week moving average of continuing claims rose 3k to 1866k.

ECB cuts 25bps as expected, not pre-committing to rate path

ECB cut its deposit rate by 25bps to 2.50% as expected. It maintains a data-dependent stance and stressing it is “not pre-committing to a particular rate path” amid rising uncertainty.

ECB noted that disinflation process remains on track, with inflation upgrade reflects stronger energy prices. Growth forecasts for 2025 and 2026 were downgraded due to weaker exports and investment, driven partly by trade and broader policy uncertainty.

In the new economic projections:

- Headline inflation to average 2.3% in 2025, 1.9% in 2026, and 2.0% in 2027.

- Core inflation to average 2.2% in 2025, 2.0% in 2026, and 1.9% in 2027.

- GDP to grow 0.9% in 2025, 1.2% In 2026, and 1.3% in 2027.

Eurozone retail sales fall -0.3% mom in Jan, EU down -0.2% mom

Eurozone retail sales volume dropped by -0.3% mom in January, missing expectations of a modest 0.1% mom increase. The decline was driven by weaker demand for non-food products, which fell -0.7% mom, while sales of automotive fuel also slipped by -0.3% mom. In contrast, spending on food, drinks, and tobacco rose by 0.6% mom, offering a slight offset to the overall decline.

Meanwhile, retail sales across the broader EU fell -0.2% mom on the month. Among individual EU, Slovakia saw the sharpest contraction, with retail trade volume plunging -9.0%, followed by Lithuania (-4.8%) and Cyprus (-2.2%). On the other hand, Slovenia (+2.3%), Hungary (+2.2%), and the Netherlands (+1.6%) recorded the strongest increases.

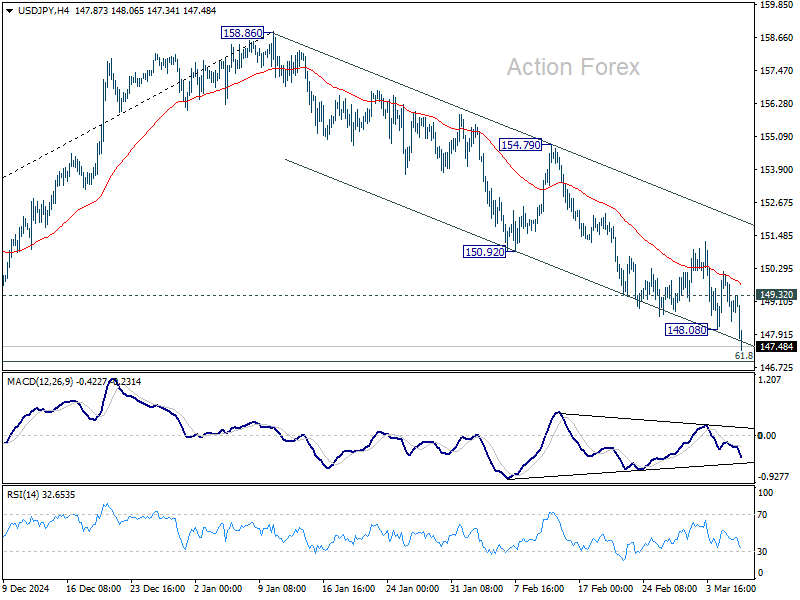

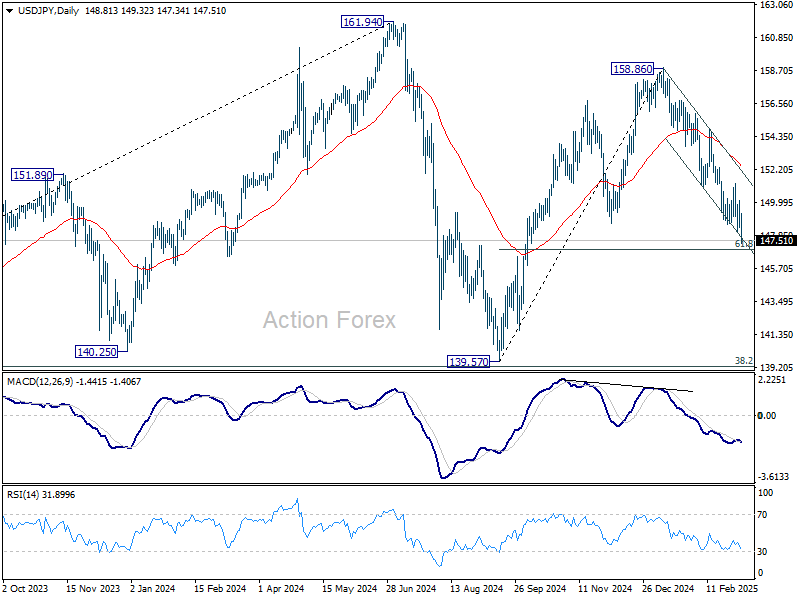

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.12; (P) 149.15; (R1) 149.91; More…

Intraday bias in USD/JPY is back on the downside with break of 148.08 temporary low. Fall from 158.86, as the third leg of the corrective pattern from 161.94 high, has resumed. Sustained break of 61.8% retracement of 139.57 to 158.86 at 146.32 will pave the way back to 139.57 low. On the upside, 149.32 minor resistance will turn intraday bias neutral and bring consolidations again, before staging another fall.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more