Dollar Struggling To Gain Momentum Despite Global Market Shakeup

In the face of mounting tumult across stocks, bonds, and the crypto realm, the currency market projects an island of relative calm. Despite the extended rout in equities and treasuries and the dramatic tumble in Bitcoin, the forex market has responded with comparative restraint. A discernible dip in commodity currencies is on display, with Australian Dollar leading the downturn as the worst performer of the week, trailed closely by its New Zealand and Canadian counterparts. However, a rapid downward spiral hasn’t taken hold as of yet.

On the flip side, while Dollar and Swiss Franc chart among the top performers, British Pound (Sterling) continues its reign, retaining its premier top position. In the mix, both the Euro and Yen tread a middle ground, neither significantly surging nor plummeting. But there is prospect of a stronger rise in Yen ahead.

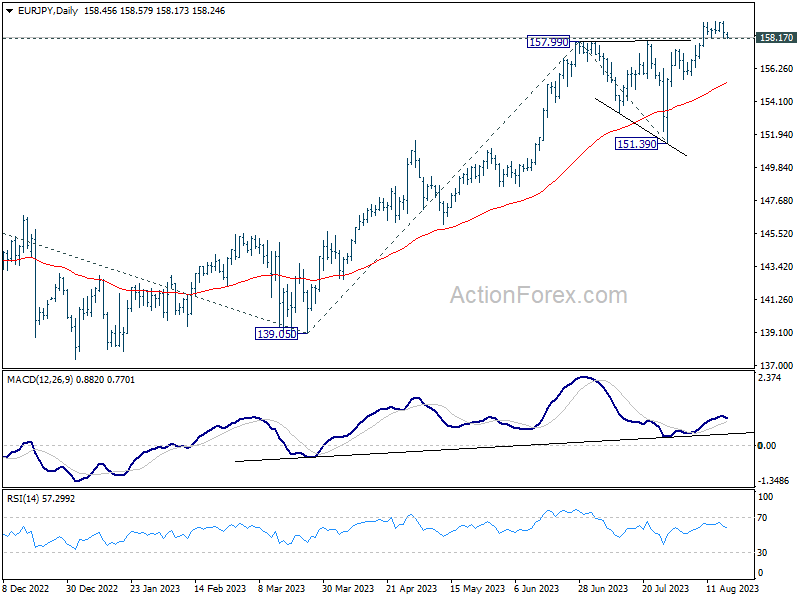

From a technical perspective, as the week draws to a close, the spotlight could shift to potential movements in Yen pairs. Should EUR/JPY breaks 158.17 support, it would likely signal a short-term peak, ushering in a more pronounced dip towards the 55 D EMA (now at 155.32). Such a move could correspondingly pull USD/JPY downwards, and possibly, a parallel dip in EUR/USD.

In Asia, at the time of writing, Nikkei is down -0.41%. Hong Kong HSI is down -1.12%. China Shanghai SSE is down -0.06%. Singapore Strait Times is down -0.69%. Overnight, DOW dropped -0.84%. S&P 500 dropped -0.77%. NASDAQ dropped -1.17%. 10-year yield rose 0.050 to 4.308.

Japan CPI core eased to 3.1% in Jul, but core-core back at four decade high

Japan’s core CPI, which excludes fresh food, eased slightly from 3.3% yoy in June to 3.1% yoy in July, aligning with market expectations. Notably, this metric continued its streak above BoJ’s 2% inflation target for a commendable 16 consecutive months.

Diving deeper, core-core CPI, which subtracts both fresh food and energy, inched higher to 4.3% yoy, equalling the peak seen in May. This current rate hasn’t been witnessed since 1981, underscoring the latent inflationary pressures within the Japanese economy.

Processed food costs are a particular hotspot, skyrocketing by 9.2% yoy – a surge not seen in nearly half a century. Adding to this, durable goods saw a robust rise of 6.0% yoy. Furthermore, possibly driven by travel and vacationing demand, accommodation fees witnessed a significant 15.1% yoy hike during the prime summer holiday period.

Conversely, energy prices painted a contrasting picture, plummeting by -8.7% yoy. This decline can largely be attributed to government interventions, with subsidies introduced to mitigate household utility expenses. These subsidies, in turn, have played a pivotal role, dragging the core CPI lower by approximately one percentage point.

Service prices also shifted gears, moving up to 2% yoy from 1.6% yoy – the most substantial leap since 1993 if we set aside the aftermath of the 1997 sales tax hike.

Despite these intricate dynamics, headline CPI remained steadfast at 3.3% yoy.

Market turbulence: Bitcoin crash and NASDAQ selloff

Markets witnessed Bitcoin’s dramatic plunge over the last 12 hours, fueled by a succession of negative headlines: the escalating Ripple-SEC legal drama, reports of SpaceX’s substantial Bitcoin write-down, and the bankruptcy filing of China’s Evergrande. But a more important question is whether the cryptocurrency’s slide mirrors is part of a larger shift in risk sentiment, underscored by this week’s drop in US stocks.

The tremors in the crypto market seemed to intensify post US Federal Judge Analisa Torres’ nod to the SEC’s interlocutory appeal, which came shortly after a preliminary ruling favoring Ripple. The narrative was further dented the Wall Street Journal’s disclosure about SpaceX’s USD 373m Bitcoin value markdown in recent years, combined with the “unexpected” news of Evergrande’s Chapter 15 bankruptcy protection in New York.

Bitcoin fell to as low as 25588 in Asian session, and recovered just ahead of 38.2% retracement of 15452 to 31815 at 25564. Risk will stay heavily on the downside as long as 28555 support turned resistance holds. Attention will be on the reaction to support zone between 24739 and 25564.

Strong rebound from this level will keep price actions from 31815 as a medium term correction only, i.e. the up trend from 15452 is not over yet. However, decisive break of this support zone will significantly raise the chance of trend reversal, and could trigger deeper acceleration to 61.8% retracement at 21702 at least.

At the same time, NASDAQ also closed sharply lower by -1.17%. Deeper fall is expected as long as 13789.15 resistance holds, to 38.2% retracement of 10088.82 to 14446.55 at 12781.89. Reaction from there will unveil whether the decline is just a correction to the rise from 10088.82, or reversing the whole trend.

Looking ahead

UK retails sales and Eurozone CPI final are the main features in European session. later in the day, Canada will release IPPI and RMPI.

EUR/USD Daily Outlook

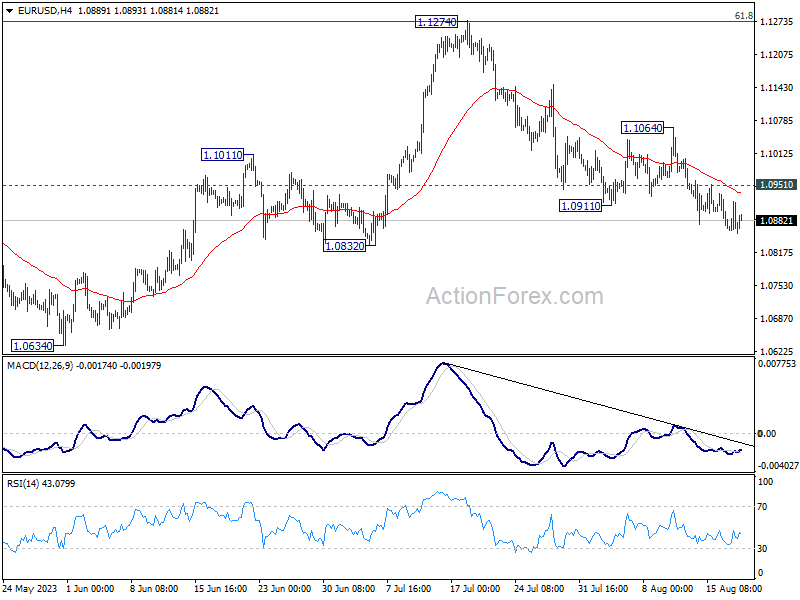

Daily Pivots: (S1) 1.0847; (P) 1.0883; (R1) 1.0908; More…

Intraday bias in EUR/USD stays on the downside at this point, even though downside momentum is relatively unconvincing. Break of 1.0832 will extend the fall from 1.1274 to 1.0609/34 cluster support. On the upside, above 1.0951 minor resistance will turn intraday bias neutral first. But risk will stay on the downside as long as 1.1064 resistance holds, in case of rebound.

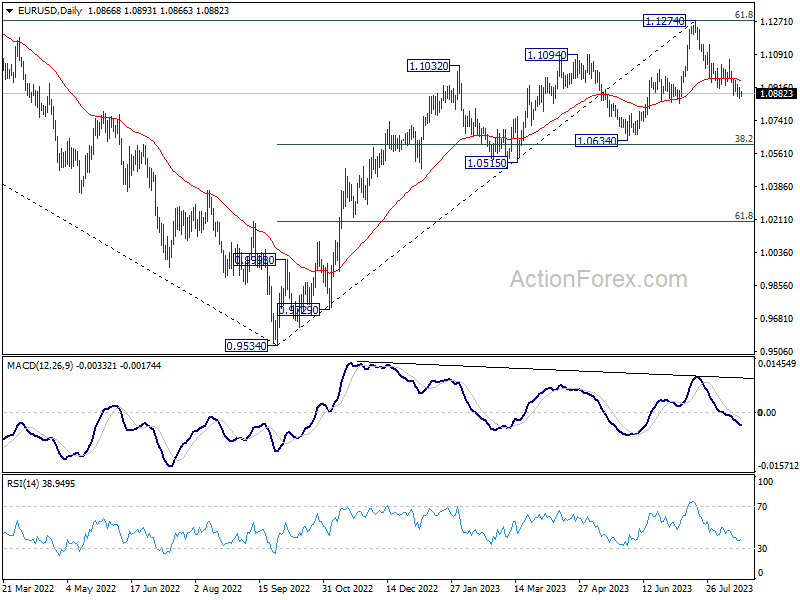

In the bigger picture, a medium term top should be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Fall from there is seen as a correction to the uptrend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Y/Y Jul | 3.30% | 3.30% | ||

| 23:30 | JPY | National CPI ex-Fresh Food Y/Y Jul | 3.10% | 3.10% | 3.30% | |

| 23:30 | JPY | National CPI ex Food Energy Y/Y Jul | 4.30% | 4.20% | ||

| 06:00 | GBP | Retail Sales M/M Jul | -0.40% | 0.70% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jul F | 5.30% | 5.30% | ||

| 09:00 | EUR | Eurozone Core CPI Y/Y Jul F | 5.50% | 5.50% | ||

| 12:30 | CAD | Industrial Product Price M/M Jul | 0.20% | -0.60% | ||

| 12:30 | CAD | Raw Material Price Index Jul | 2.10% | -1.50% |

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more