Dollar Stays Weak As Markets Await Fed Guidance, Yen Softens After BoJ Hold

Dollar remains under pressure as markets await FOMC rate decision and, more crucially, the updated economic projections. While the central bank is widely expected to hold rates steady at 4.25-4.50%, traders are looking for any signs that Fed officials are adjusting their outlook in response to mounting trade tensions. Meanwhile, US stocks saw another selloff overnight, led by the tech sector, though major indexes have so far held above last week’s lows. Sentiment remains fragile, and any dovish elements in Fed’s projections could trigger another round of risk aversion and Dollar weakness. However, the biggest market move may be on hold until April 2, when the final decision on reciprocal tariffs is expected.

Japanese Yen is also soft in a tight range after BoJ left monetary policy unchanged earlier today. While this decision was widely anticipated, some market participants noted that the earlier-than-usual timing of the announcement suggested that the BoJ was not yet ready to accelerate rate hikes. Yen has also weakened this week on broader risk-on sentiment in Asia, despite the selloff in US equities.

On the other hand, Euro remains firm, though lacking decisive upside momentum. Germany’s parliament approved the massive fiscal expansion plan yesterday, marking a historic departure from the country’s long-standing fiscal conservatism. This move has given CDU/CSU leader Friedrich Merz a significant political boost as he continues talks with the Social Democrats to form a centrist coalition government. While some economists argue that Germany’s fiscal expansion is the most significant since reunification, they also warned that structural reforms will be necessary to turn this spending into sustainable growth.

Looking at currency performance this week, Kiwi is leading gains, followed by Swiss Franc and Aussie. In contrast, Yen remains the weakest performer, followed by Dollar and Sterling. Euro and Loonie are positioned in the middle of the pack.

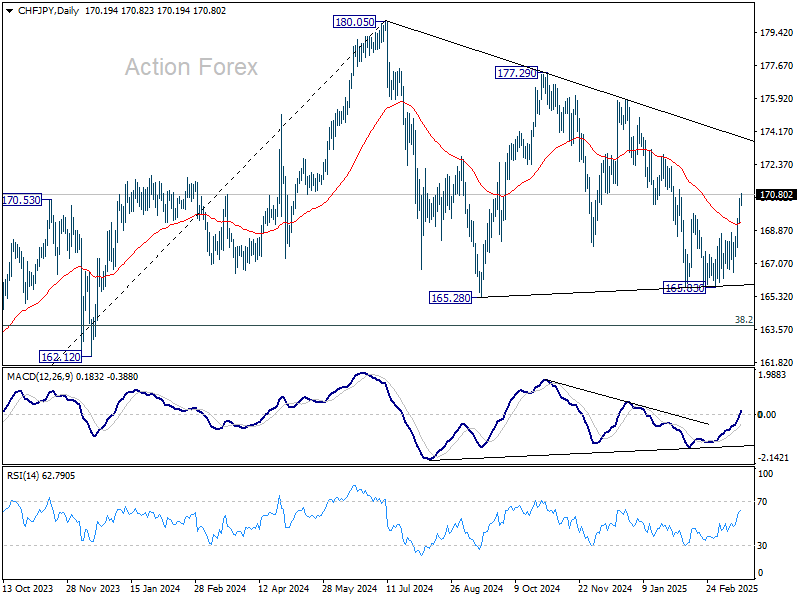

Technically, CHF/JPY is among the top movers this week so far. The extended rebound and firm break of 55 D EMA (now at 162.27) suggests that fall from 177.29 has completed at 165.83 already. The whole corrective pattern from 180.05 might have finished too. Further rise is now expected to trend line resistance at 173.95 first. Firm break there will solidify this bullish case and target 177.29/180.05 resistance zone next.

In Asia, at the time of writing, Nikkei is up 0.03%. Hong Kong HSI is down -0.09%. China Shanghai SSE is down -0.18%. Singapore Strait Times is up 0.34%. Japan 10-year JGB yield is up 0.011 at 1.517. Overnight, DOW fell -0.62%. S&P 500 fell -1.07%. NASDAQ fell -1.71%. 10-year yield fell -0.025 to 4.281.

BoJ holds rates, flags exchange rate as key inflation factor

BoJ kept its uncollateralized overnight call rate unchanged at around 0.50%, as widely expected.

In its statement, BoJ noted that growth is expected to remain above potential, while inflation progress remains on track toward its 2% target. However, policymakers flagged high levels of uncertainty, particularly citing global trade tensions and policy shifts in major economies as key risks.

A notable shift in BoJ’s tone was its heightened focus on exchange rate movements as a key factor influencing inflation. The central bank acknowledged that with firms increasingly raising wages and prices, exchange rate developments are, compared to the past, “more likely to affect prices”.

This suggests that further depreciation in Yen could accelerate price increases, and influence future monetary policy decisions.

Japan’s export rises 11.4% yoy in Feb, up for fifth straight month

Japan’s exports surged 11.4% yoy to JPY 9,191B in February, marking the fifth consecutive month of growth, driven by strong demand from both the US and China. Exports to the US rose 10.5% yoy, while shipments to China saw an even stronger 14.1% yoy increase.

Meanwhile, imports declined by -0.7% yoy, marking their first drop in three months, as demand for crude oil and coal weakened. This shift in trade dynamics helped Japan return to a trade surplus of JPY 584.5B, the first positive balance in two months.

On a seasonally adjusted basis, exports rose 4.0% mom to JPY 9,688B, while imports fell -4.1% mom to JPY 9,505B, leading to a JPY 182B surplus.

Fed to stand pat, watch for signs of trade war fallout in new projections

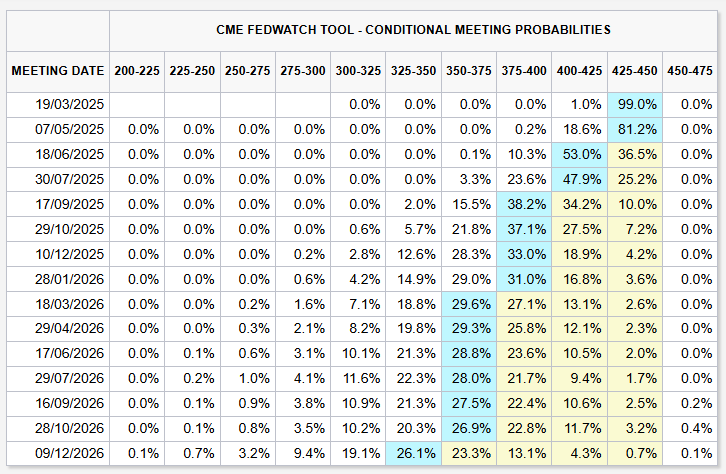

Fed is set to keep interest rates unchanged at 4.25-4.50% today. The focus will be on the updated economic projections, which may drop hints that Fed is beginning to pre-empt a full-blown trade war into its outlook. Additionally, another key element to watch will be the closely followed “dot plot”, which will reveal whether Fed still expects two rate cuts this year.

Chair Jerome Powell’s press conference is important as usual, as he will need to balance Fed’s current economic assessment with the risks posed by US President Donald Trump’s trade policy. However, with no details on the big event of reciprocal tariffs on April 2, Powell is unlikely to offer any concrete guidance. Instead, he may just reiterate the central bank’s stance that it is “in no hurry” to cut rates and emphasize a data-dependent approach.

Currently, Fed fund futures indicate that June and September are the most likely timing for policy easing.

One key market reaction to watch will be 10-year Treasury yield, which recovery has clearly lost momentum well ahead of 55 D EMA (now at 4.389). Any dovish tilt from Fed today could push yields back toward 4.106 support. That would in turn keep Dollar under pressure.

Though, firm break of 61.8% retracement of 3.603 to 4.809 at 4.063 is not anticipated for now, at least until the tariff picture is cleared or there are more signs of recession in the US. On the upside, any rebound should be limited by 55 D EMA.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0907; (P) 1.0931; (R1) 1.0969; More…

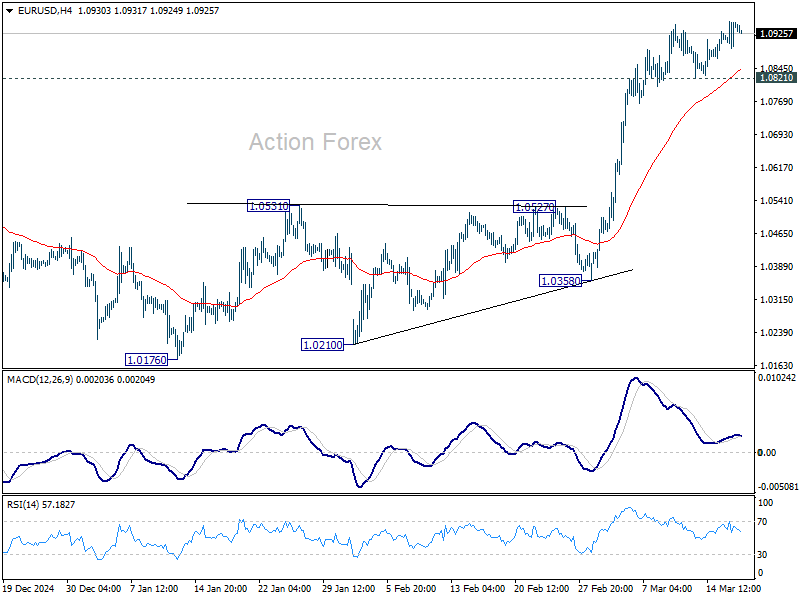

Intraday bias in EUR/USD remains on the upside for the moment. Current rally from 1.0176 should target 1.1274 key resistance. On the downside, though, break of 1.0821 support will indicate short term topping, likely with bearish divergence condition in 4H MACD. That will turn bias back to the downside for deeper pullback.

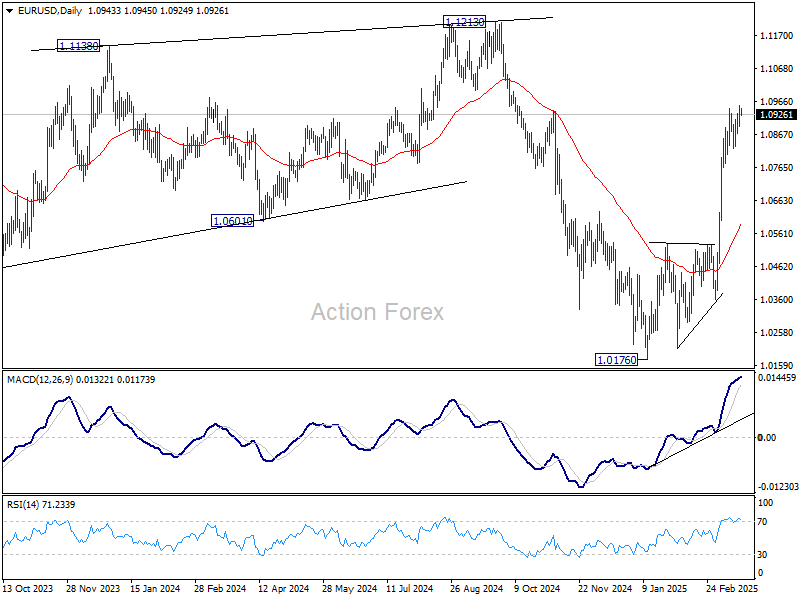

In the bigger picture, prior strong break of 55 W EMA (now at 1.0675) suggests that fall from 1.1274 (2024 high) has completed as a three wave correction to 1.0176. Rise from 0.9534 is still intact, and might be ready to resume. Decisive break of 1.1274 will target 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Also, that will send EUR/USD through a multi-decade channel resistance will carries larger bullish implication. This will now be the favored case as long as 1.0531 resistance turned support holds.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more