Dollar Stays Soft With Falling Yields And Stocks Rally

Dollar remains under pressure as the market heads into the US session, with selling momentum picks up slightly alongside a continued decline in Treasury yields. US stock futures are staging a robust rally, reflecting optimism over President-elect Donald Trump’s selection of Scott Bessent as Treasury Secretary. Bessent is viewed as a safe choice for implementing key policies, including tariffs, with a measured approach.

On the other hand, Euro stands out as the strongest performer so far, shrugging off disappointing German Ifo Business Climate data. Swiss Franc follows as the second strongest, while Yen rounds out the top three. In contrast, Canadian Dollar is among the weakest, followed by Australian Dollar, with Kiwi and Sterling occupying middle-ground positions.

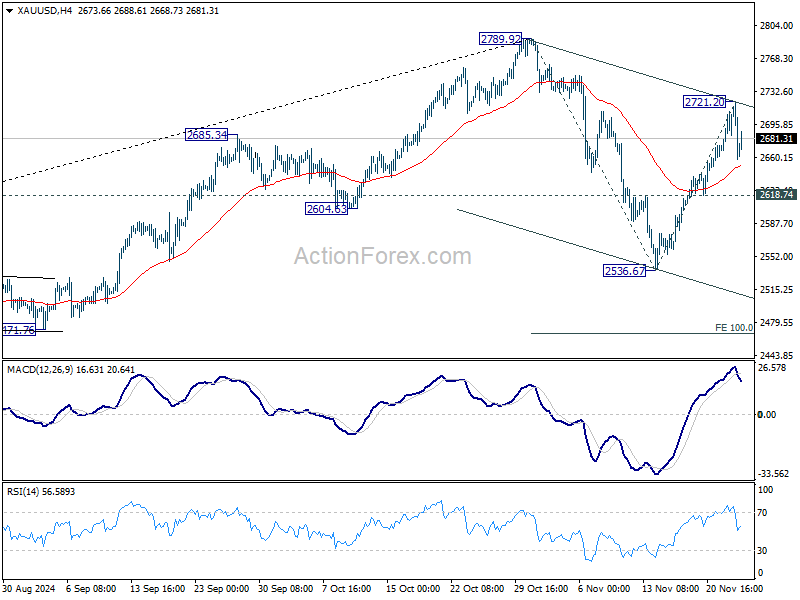

Technically, Gold is also weakening slightly in spite of the pullback in Dollar. Rebound from 2536.67 stalled after reaching 2721.20. While another rise cannot be ruled out, upside should be limited by 2789.92 resistance. Break of 2618.74 support would argue that the corrective pattern from 2789.92 has started the third leg for 2536.67 again, and possibly below.

In Europe, at the time of FTSE is up 0.33%. DAX is up 0.43%. CAC is up 0.14%. UK 10-year yield is down -0.048 at 4.344. Germany 10-year yield is down -0.0203 at 2.227. Earlier in Asia,Nikkei rose 1.30%. Hong Kong HSI fell -0.41%. China Shanghai SSE fell -0.11%. Singapore Strait Times fell -0.39%. Japan 10-year JGB yield fell -0.0057 to 1.074.

BoE’s Lombardelli warns of costly risks if inflation upside materializes

I view the probabilities of downside and upside risks to inflation as broadly balanced. But at this point I am more worried about the possible consequences if the upside materialised, as this could require a more costly monetary policy response.

Lombardelli said the level of interest rates was “comfortably in restrictive territory at the moment” and supported “a gradual removal of monetary policy restriction” but the data over the coming months will be critical and need “careful observation.”

“There are some signs that the process of wage disinflation may be slowing, so it’s too early to declare victory on inflation. It’s often been said that the last mile may be the hardest, and that’s where we are now.”

ECB’s Lane warns against prolonged restrictive policy

In an interview with Les Echos, ECB Chief Economist Philip Lane highlighted that “monetary policy should not remain restrictive for too long”.

He explained the challenges of maintaining restrictive monetary policy stance for an extended period, cautioning that it could stifle economic growth and lead to inflation falling below ECB’s 2% target.

However, while markets currently assign a 50% probability to a 50bps rate cut in December, Lane appeared to moderate these expectations by emphasizing that inflation remains above target in key areas, particularly services, and that much of the recent decline stems from easing energy costs rather than broad-based price adjustments.

“There is still some distance to go in terms of adjustment for inflation to return to the desired level in a more sustainable way,” Lane noted.

German Ifo falls to 85.7, further deteriorations

Germany’s Ifo Business Climate Index declined to 85.7 in November, down from 86.5 in October, reflecting growing pessimism across key sectors of Europe’s largest economy. Current Assessment Index dropped from 85.7 to 84.3, indicating weaker confidence in present conditions. Expectations Index edged slightly lower from 87.3 to 87.2, suggesting limited optimism for the months ahead.

Sector-specific data painted a grim picture. Manufacturing sentiment worsened, dropping from -20.6 to -21.9, and the services sector also reversed, declining from 0.1 to -3.6. Construction sentiment weakened significantly, falling from -25.7 to -28.5. Trade was the only sector to show some improvement, rising from -29.4 to -26.6, though it remains firmly in negative territory.

Ifo President Clemens Fuest characterized the situation as increasingly bleak, remarking that sentiment among German companies has turned “gloomier” and that the economy is “floundering.”

New Zealand’s Q3 retail sales down -0.1% qoq, ex-auto sales slumps -0.8% qoq

New Zealand’s retail sales volume for Q3 showed a marginal decline of -0.1% qoq, a better outcome than the expected -0.5% qoq contraction. However, the data revealed underlying weakness, as retail sales excluding autos fell by a sharper-than-expected -0.8% qoq, missing the forecast of -0.3% qoq.

A breakdown of the data shows that 10 out of 15 retail industries experienced lower sales volumes during the quarter.

Meanwhile sales value dropped significantly by -0.7% qoq. Regionally, 15 of the 16 regions reported lower seasonally adjusted sales values, underscoring the broad-based nature of the decline.

As Michael Heslop, an economic indicators spokesperson, noted, “Retail activity was flat in the September 2024 quarter, with a decrease in spending in most retail industries being offset by an increase in motor vehicles and electrical and electronic goods.”

New Zealand’s goods exports rises 7.5% yoy in Oct, goods imports up 3.0% yoy

New Zealand’s goods exports increased by 7.5% yoy in October, reaching NZD 5.8B, while total goods imports rose by 3.0% yoy to NZD 7.3B. This resulted in a trade deficit of NZD -1.54B, which, although significant, was better than the expected deficit of NZD -1.76B.

Key export markets demonstrated robust growth, with exports to China rising by NZD 113m (8.4% yoy), Australia up by NZD 60m (8.3% yoy), the US surging NZD 90m (15% yoy), the EU increasing NZD 48m (18% yoy), and Japan gaining NZD 19m (6.7% yoy).

On the import side, trends were more mixed. Imports from China and the EU declined, falling NZD 42m (-2.7% yoy) and NZD 35m (-3.2% yoy) respectively. However, imports from the US surged by NZD 459m (79% yoy), while South Korea and Australia saw notable increases of NZD 148m (32% yoy) and NZD 58m (7.5% yoy) respectively.

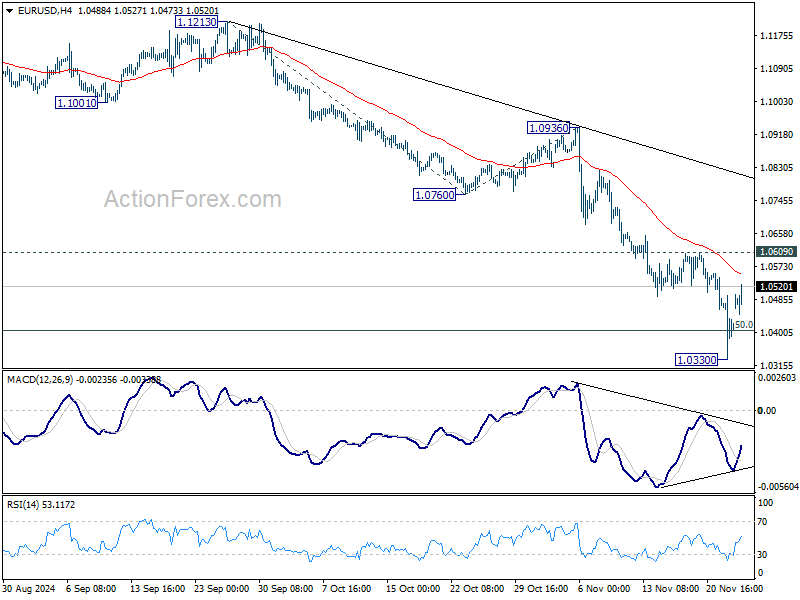

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0335; (P) 1.0416; (R1) 1.0500; More…

EUR/USD’s recovery from 1.0330 extends higher today but stays below 1.0609 resistance. Intraday bias remains neutral and further decline is still in favor. On the downside, sustained trading below 1.0404 key fibonacci level will carry larger bearish implication and target next level at 161.8% projection of 1.1213 to 1.0760 from 1.0936 at 1.0203. However, firm break of 1.0609 will confirm short term bottoming, and turn bias back to the upside for 1.0760 support turned resistance first.

In the bigger picture, immediate focus is now on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more