Dollar Softens Post-PPI Release, Yet Selling Momentum Remains Limited

Dollar is under some selling pressure in early US session despite stronger-than-expected PPI readings. However, downside momentum of the greenback is relatively limited. The post-CPI selloff yesterday did not gain significant traction, partly because stock markets unexpectedly retreated. Currently, futures are indicating a flat opening, and if activity in risk markets remains subdued in this final session of the week, Dollar might stabilize, at least temporarily.

Meanwhile, Japanese Yen is undergoing a consolidation phase after yesterday’s significant gains—the largest daily rally against Dollar since late 2022. Although there has been no official confirmation from Japanese officials regarding intervention in the currency markets, data released by BoJ today suggests that the scale of intervention was likely around JPY 3.5T.

The estimate on Japan’s intervention is derived from movements observed in the central bank’s accounts. Notably, BoJ’s current account balance is expected to decrease by JPY 3.2T due to government fiscal factors by next Tuesday, a stark contrast to the JPY 333B increase forecasted by private money brokers prior to the suspected intervention. Further clarity on these interventions will be available when official monthly data is released on July 31.

Reviewing the weekly performance across currency markets, New Zealand Dollar remains the weakest, closely followed by Dollar and then Swiss Franc. On the stronger side, Yen leads, followed by Sterling and Euro. Australian Dollar and Canadian Dollar are positioned in the middle of the performance spectrum.

In Europe, at the time of writing, FTSE is up 0.19%. DAX is up 0.22%. CAC is up 0.65%. UK 10-year yield is up 0.0524 at 4.131. Germany 10-year yield is up 0.045 at 2.513. Earlier in Asia, Nikkei fell -2.45%. Hong Kong HSI rose 2.59%. China Shanghai SSE rose 0.03%. Singapore Strait Times rose 0.65%. Japan 10-year JGB yield fell -0.0336 to 1.050.

US PPI rises 0.2% mom, 2.6% yoy, largest annual advance in more than a year

US PPI for final demand rose 0.2% mom in June, slightly above expectation of 0.1% mom. PPI rose 2.6% yoy for the 12 months ended in June, above expectation of 2.2% yoy. That’s also the largest annual advance since March 2023.

PPI less foods, energy, and trade services were unchanged at 0.0% mom. For the 12 months period, PPI less foods, energy, and trade services rose 3.1% yoy.

New Zealand BNZ manufacturing freefalls to lowest non-lockdown level since 2009

New Zealand BusinessNZ Performance of Manufacturing Index fell sharply from 46.6 to 41.1 in June, well below the long-term average of 52.6 and marking the lowest non-lockdown monthly level since February 2009.

Breaking down the details, production dropped from 44.0 to 35.4, and new orders fell from 43.9 to 38.8. These sub-40 activity levels for production and new orders are the lowest seen outside of COVID lockdowns since November 2008. Employment also declined significantly, from 50.4 to 43.8, its lowest non-COVID monthly result since July 2019. Finished stocks decreased from 52.3 to 47.9, while deliveries remained unchanged at 44.9.

BusinessNZ’s Director of Advocacy, Catherine Beard, expressed significant concern over the “freefall in activity from May to June,” highlighting the severe challenges facing a sector that has been contracting for the past 15 months. The proportion of negative comments surged to 76.3%, up from 63.5% in May and 69% in April, with respondents highlighting an overall economic slowdown and tough recessionary conditions.

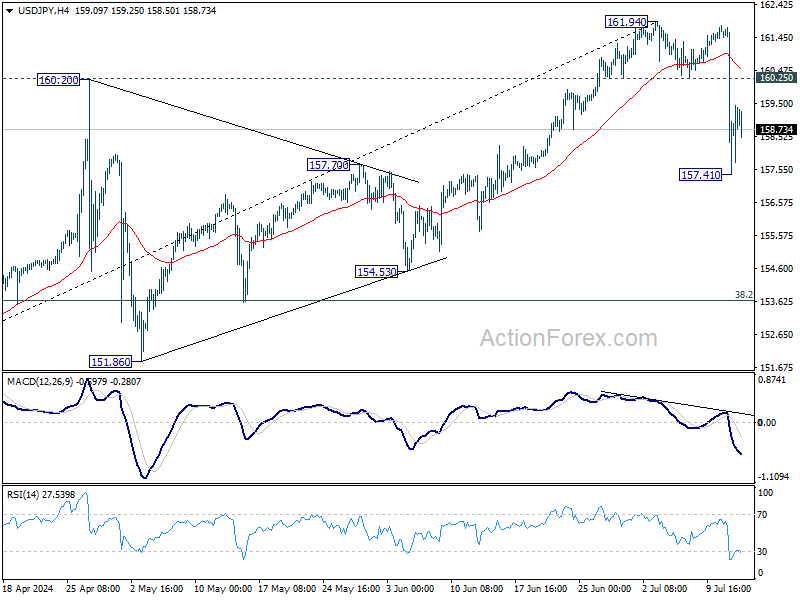

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.97; (P) 159.37; (R1) 161.30; More…

No change in USD/JPY’s outlook. Deeper decline is expected with 160.25 support turned resistance intact. Fall from 161.94 is seen as corrective the five-wave rally from 140.25. Sustained break of 55 D EMA (now at 157.71) will affirm this bearish case. Next target will be 38.2% retracement of 140.25 to 161.94 at 163.65.

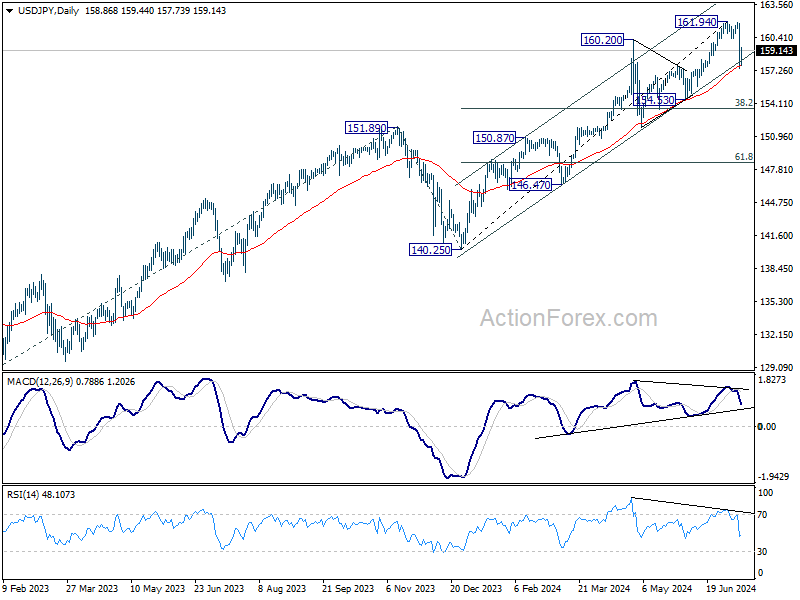

In the bigger picture, long term up trend is still in progress. Further rise is expected as long as 154.53 support holds. Next target is 100% projection of 127.20 (2023 low) to 151.89 (2023 high) from 140.25 at 164.94. However, sustained break of 154.53 will raise the chance of larger scale correction and target 140.25/151.89 support zone.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Jun | 41.1 | 47.2 | 46.6 | |

| 03:00 | CNY | Trade Balance (USD) Jun | 99.1B | 85.1B | 82.6B | |

| 03:00 | CNY | Trade Balance (CNY) Jun | 704B | 590B | 586B | |

| 04:30 | JPY | Industrial Production M/M May F | 3.60% | 2.80% | 2.80% | |

| 12:30 | CAD | Building Permits M/M May | -12.20% | -5.00% | 20.50% | 23.40% |

| 12:30 | USD | PPI M/M Jun | 0.20% | 0.10% | -0.20% | 0.00% |

| 12:30 | USD | PPI Y/Y Jun | 2.60% | 2.20% | 2.20% | |

| 12:30 | USD | PPI Core M/M Jun | 0.40% | 0.20% | 0.00% | 0.30% |

| 12:30 | USD | PPI Core Y/Y Jun | 3.00% | 2.50% | 2.30% | |

| 14:00 | USD | Michigan Consumer Sentiment Jul P | 68.5 | 68.2 |

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more