Dollar Recovers As Markets Await Fed Projections, Gold Loses Some Momentum

Dollar is recovering across the board as markets enter the US session, though the move appears to be more caution-driven than a shift in sentiment. With FOMC rate decision looming, traders are taking a more neutral stance rather than doubling down on Dollar’s recent weakness. Fed is widely expected to keep rates steady at 4.25-4.50%, so the real focus will be on the updated economic projections. Given the uncertainty surrounding US trade policy, these forecasts could offer the first glimpse of how policymakers are factoring in US President Donald Trump’s tariffs into their outlook.

Since the last FOMC meeting in December, the U.S. has implemented its first set of tariffs under the Trump administration. Now, the markets are preparing for the ambitious reciprocal tariffs set to take effect in early April. While tariff impacts may not be fully reflected in Fed’s projections yet, traders will be looking for any revisions to growth and inflation forecasts that could indicate whether policymakers are growing more concerned about trade war risks. If the Fed acknowledges increased downside risks to growth or upward pressures on inflation, markets could adjust their rate cut expectations accordingly.

Meanwhile, Euro is on the weaker side as Eurozone CPI for February was finalized slightly lower than initial estimates. Comments from ECB officials today are typically cautious. French ECB Governing Council member François Villeroy de Galhau reiterated that the timing and size of rate cuts will depend on data. Meanwhile, ECB Vice President Luis de Guindos emphasized that defense spending remains Europe’s top priority, but warned that budget stability must be maintained within the bloc’s fiscal rules.

For the day so far, Dollar is the strongest performer, followed by the Loonie and Sterling. On the weaker side, Kiwi is the worst performer, followed by Aussie and Euro. Yen and Swiss Franc are positioning in the middle.

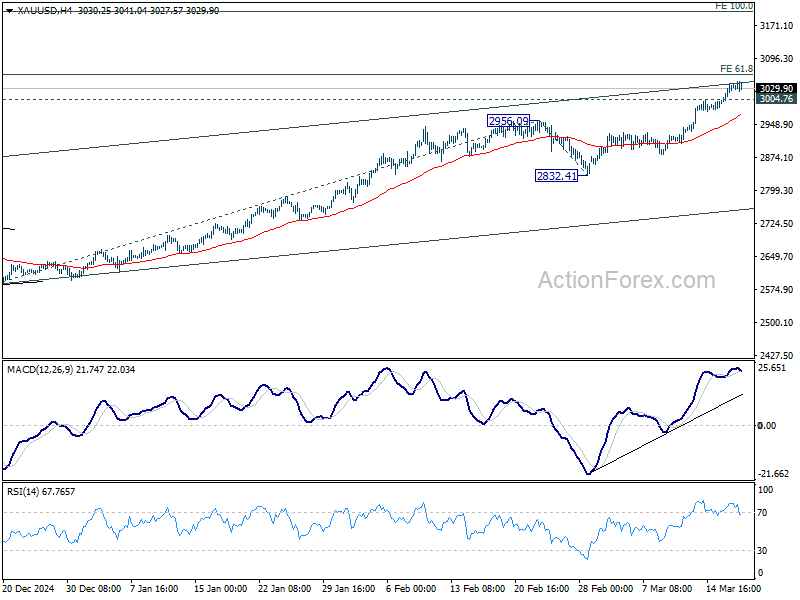

Technically, Gold is losing momentum as it approaches 61.8% projection of 2584.24 to 2956.09 from 2832.41 at 3062.21. This level is close to a key medium-term rising channel resistance, making it a critical test for gold bulls. A break below 3004.76 resistance-turned-support would signal the first rejection at the resistance zone, and leads to a near term pullback.

However, if Dollar resumes its selloff after Fed’s announcement, Gold could break through 3062.21, probably triggering upside acceleration towards 100% projection at 3204.26.

In Europe, at the time of writing, FTSE is down -0.07%. DAX is down -0.81%. CAC is up 0.36%. UK 10-year yield is up 0.003 at 4.65. Germany 10-year yield is down -0.007 at 2.806. Earlier in Asia, Nikkei fell -0.25%. Hong Kong HSI rose 0.12%. China Shanghai SSE fell -0.10%. Singapore Strait Times rose 0.34%. Japan 10-year JGB yield rose 0.026 to 1.531.

Eurozone CPI finalized at 2.3% in Feb, core CPI at 2.6%

Eurozone headline CPI was finalized at 2.3% yoy in February, down from 2.5% yoy in January. Core CPI , which excludes energy, food, alcohol, and tobacco, eased slightly to 2.6% yoy from 2.7% yoy.

The largest driver of Eurozone inflation was services, contributing +1.66 percentage points, followed by food, alcohol, and tobacco (+0.52 pp). Non-energy industrial goods and energy made smaller contributions, with energy adding just +0.01 pps.

In the broader EU, inflation was finalized at 2.7% yoy, down from 2.8% yoy in January. Inflation disparities across member states remain stark, with France (0.9%), Ireland (1.4%), and Finland (1.5%) registering the lowest rates, while Hungary (5.7%), Romania (5.2%), and Estonia (5.1%) recorded the highest. Compared to January, inflation declined in 14 member states, remained unchanged in six, and increased in seven.

BoJ holds rates, flags exchange rate as key inflation factor

BoJ kept its uncollateralized overnight call rate unchanged at around 0.50%, as widely expected.

In its statement, BoJ noted that growth is expected to remain above potential, while inflation progress remains on track toward its 2% target. However, policymakers flagged high levels of uncertainty, particularly citing global trade tensions and policy shifts in major economies as key risks.

A notable shift in BoJ’s tone was its heightened focus on exchange rate movements as a key factor influencing inflation. The central bank acknowledged that with firms increasingly raising wages and prices, exchange rate developments are, compared to the past, “more likely to affect prices”.

This suggests that further depreciation in Yen could accelerate price increases, and influence future monetary policy decisions.

Japan’s export rises 11.4% yoy in Feb, up for fifth straight month

Japan’s exports surged 11.4% yoy to JPY 9,191B in February, marking the fifth consecutive month of growth, driven by strong demand from both the US and China. Exports to the US rose 10.5% yoy, while shipments to China saw an even stronger 14.1% yoy increase.

Meanwhile, imports declined by -0.7% yoy, marking their first drop in three months, as demand for crude oil and coal weakened. This shift in trade dynamics helped Japan return to a trade surplus of JPY 584.5B, the first positive balance in two months.

On a seasonally adjusted basis, exports rose 4.0% mom to JPY 9,688B, while imports fell -4.1% mom to JPY 9,505B, leading to a JPY 182B surplus.

GBP/USD Mid-Day Outlook

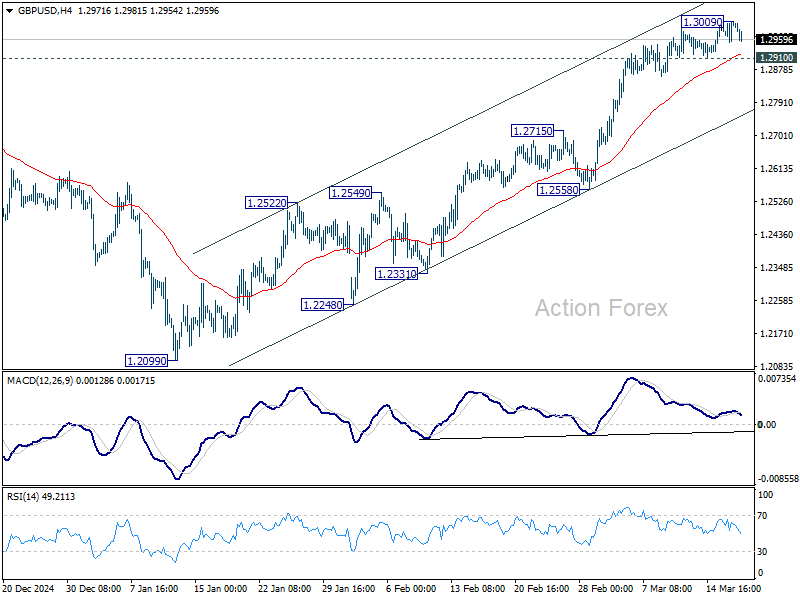

Daily Pivots: (S1) 1.2967; (P) 1.2988; (R1) 1.3025; More…

Intraday bias in GBP/USD is turned neutral first with current retreat. Another rise is expected as long as 1.2910 support holds. Above 1.3009 will resume the rally from 1.2099 to retest 1.3433 high. However, firm break of 1.2910 will indicate short term topping, likely with bearish divergence condition in 4H MACD. That would turn intraday bias back to the downside for deeper pullback.

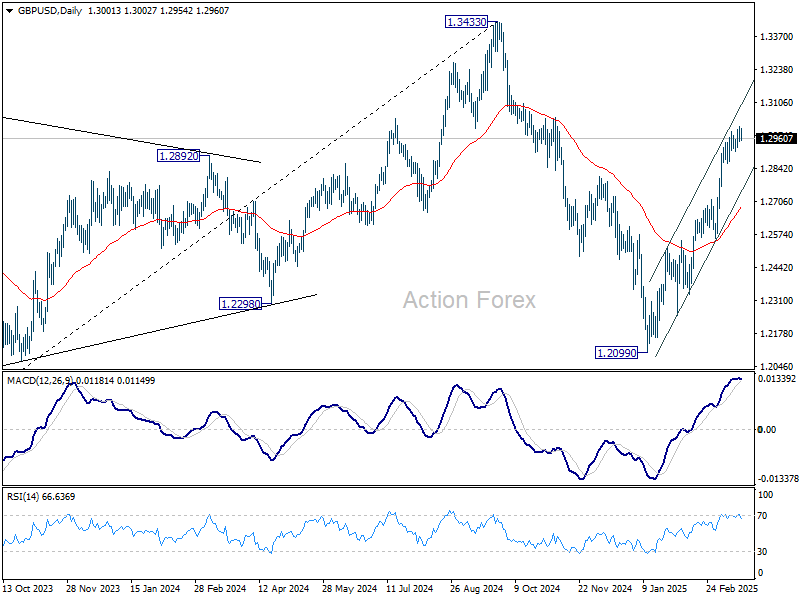

In the bigger picture, up trend from 1.3051 (2022 low) is not completed. Resumption is expected after corrective pattern from 1.3433 completes. Next target will be 1.4248 key resistance. This will now remain the favored case as long as 1.2099 support holds.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more