“Coalition Of The Willing” Fuels Euro Strength, Boosts Defense Outlook

European markets saw a strong rally today, with notable fund inflows driving gains in DAX and Euro. Investor sentiment was boosted by expectations of increased military spending after the announcement of the UK and France-led “Coalition of the Willing” to support Ukraine. FTSE and Sterling also benefited from the renewed optimism, as traders priced in the broader economic implications of higher defense expenditures across Europe.

Defense stocks led the charge, as recent geopolitical developments, in particular the Trump-Zelenskiy clash in the Oval Office, pointed to the beginning of a European rearmament cycle. With growing isolationism in the US under President Donald Trump, European nations appear to be shifting toward greater self-reliance in military production, reducing dependence on the US. This shift has fueled expectations of long-term defense budget expansions, providing fresh momentum for European economies.

Meanwhile, the latest Eurozone inflation data provided a mix of signals for policymakers at ECB. Prices growth did decelerate slightly in February, an outcome that might please the doves. However, the slowdown probably isn’t enough to change please the hawks for letting guard off inflation risk.. Policymakers are still certain to continue their measured approach to rate cuts with another 25bps reduction this week. But the data will spark fresh debate over the pace and extent of easing beyond the decision.

Overall in the currency markets, Euro is the best performer for the day so far, followed by Sterling, and then Aussie. Yen is the worst, followed by Dollar, and then Kiwi, Loonie and Kiwi are positioning in the middle.

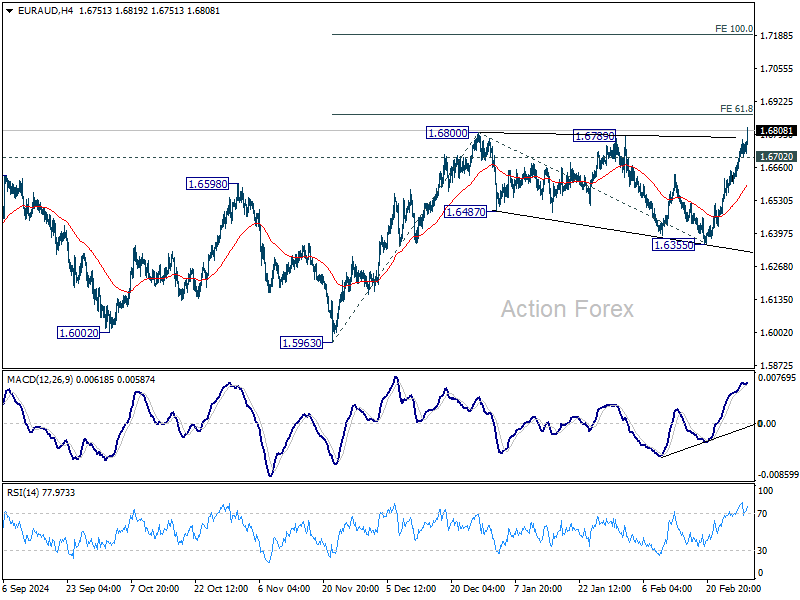

Technically EUR/AUD’s break of 1.6800 resistance should confirm resumption of whole rally from 1.5693. Further rise should be seen to 61.8% projection of 1.5963 to 136800 from 1.6355 at 1.6872. Decisive break there could prompt upside acceleration to 100% projection at 1.7192. Nevertheless, break of 1.6702 support will delay the bullish case and bring consolidations first.

In Europe, at the time of writing, FTSE is up 0.77%. DAX is up 2.33%. CAC is up 1.43%. UK 10-year yield is up 0.052 at 4.537. Germany 10-year yield is up 0.091 at 2.502. Earlier in Asia, Nikkei rose 1.70%. Hong Kong HSI rose 0.28%. China Shanghai SSE fell -0.12%. Singapore Strait Times rose 0.34%. Japan 10-year JGB yield rose 0.034 to 1.410.

Eurozone CPI falls to 2.4%, core CPI slows to 2.6%, both above expectations

Eurozone CPI ticked down from 2.5% yoy to 2.4% yoy in February, above expectation of 2.3% yoy. Core CPI (ex-energy, food, alcohol & tobacco), fell from 2.7% yoy to 2.6% yoy, above expectation of 2.5% yoy.

Looking at the main components of inflation, services is expected to have the highest annual rate in February (3.7%, compared with 3.9% in January), followed by food, alcohol & tobacco (2.7%, compared with 2.3% in January), non-energy industrial goods (0.6%, compared with 0.5% in January) and energy (0.2%, compared with 1.9% in January).

Eurozone PMI manufacturing finalized at 47.6, a 24-mth high

Eurozone manufacturing activity showed signs of stabilization in February, with PMI finalized at 47.6, a 24-month high, up from January’s 46.6. While still in contraction territory, the improvement offers some hope that the sector may be finding its footing.

Among individual countries, Ireland led the rankings at 51.9, marking a 12-month high, while the Netherlands reached the neutral 50.0 mark for the first time in eight months. However, Spain dipped to a 13-month low at 49.7, and Italy, Austria, Germany, and France all remained below 50, despite showing some improvement.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, emphasized that while the data is encouraging, it’s “too early to call it a recovery”. New orders are still falling but at the slowest rate since May 2022, and production is inching closer to stabilization. After nearly three years of recession, there is potential for modest growth in the coming months.

Despite ongoing risks, most businesses remain optimistic about the future, with confidence slightly above its long-term average. This resilience is notable, given the looming threat of US tariffs. Additional positive factors include hopes that Russia’s war in Ukraine could come to an end this year, alongside expectations of greater political stability in Germany following the recent elections.

UK PMI manufacturing finalized at 46.9, job cuts accelerate

The UK manufacturing sector continued to struggle in February, with PMI Manufacturing finalized at 46.9, down from January’s 48.3, marking a 14-month low. Weak demand and declining confidence among clients have exacerbated the downturn, leading to falling output and new orders.

Rob Dobson, Director at S&P Global Market Intelligence, noted that UK manufacturers are facing an “increasingly difficult trading environment.” The combination of subdued demand, rising cost pressures, and uncertainty over future economic conditions is making it harder for firms to sustain growth.

Inflation fears are also rising, particularly due to changes in the national minimum wage and employer NICs announced in the Autumn Budget.

One of the most concerning trends is the acceleration in job losses. The pace of staff reductions in the sector is now at levels not seen since the pandemic-induced slump in mid-2020.

Japan’s PMI manufacturing finalized at 49 in Feb, modest improvement but outlook remains weak

Japan’s manufacturing sector showed slight improvement in February, with PMI finalized at 49.0, up from 48.7 in January. However, the sector remains in contraction territory, reflecting ongoing struggles with weak demand.

According to Usamah Bhatti at S&P Global Market Intelligence, manufacturers cited soft global and domestic demand, with “muted conditions” in key markets such as the US, Europe, and China. Additionally, purchasing activity saw a solid and sustained decline.

The “near-term outlook remains clouded”. Business confidence fell to its lowest level since mid-2020, driven by growing concerns over the impact of US trade policies and a slower-than-expected global economic recovery.

China’s Caixin PMI manufacturing rises to 50.8, but employment remains a concern

China’s Caixin PMI Manufacturing climbed to 50.8 in February, up from 50.1, exceeding expectations of 50.3.

Wang Zhe, Senior Economist at Caixin Insight Group, noted that new export orders rebounded, corporate purchasing increased, and logistics remained smooth. However, employment continued to decline, and output prices stayed weak.

Additionally, official PMI data released over the weekend further reinforced signs of recovery. The official PMI Manufacturing rebounded from 49.1 to 50.2, marking its highest level since November and moving back into expansionary territory. Additionally, the non-manufacturing PMI, which covers services and construction, ticked up to 50.4 from 50.2.

EUR/USD Mid-Day Outlook

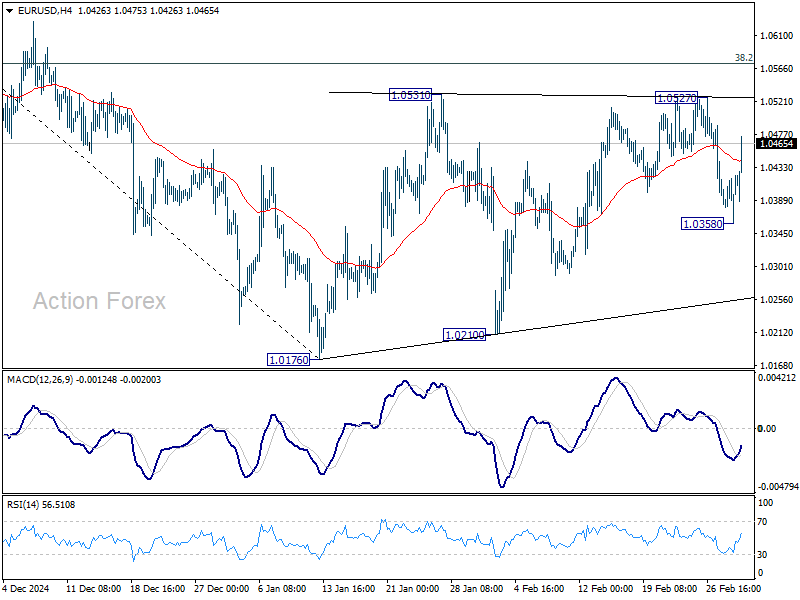

Daily Pivots: (S1) 1.0350; (P) 1.0385; (R1) 1.0410; More…

EUR/USD’s strong rebound today is mixing up the near term outlook. But still, intraday bias stays neutral and further decline is in favor as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. Below 1.0358 will target 1.0176/0210 support zone first. Firm break there will resume whole fall from 1.1213, and carry larger bearish implications. However, sustained trading above 1.0572 will pave the way to 61.8% retracement at 1.0817.

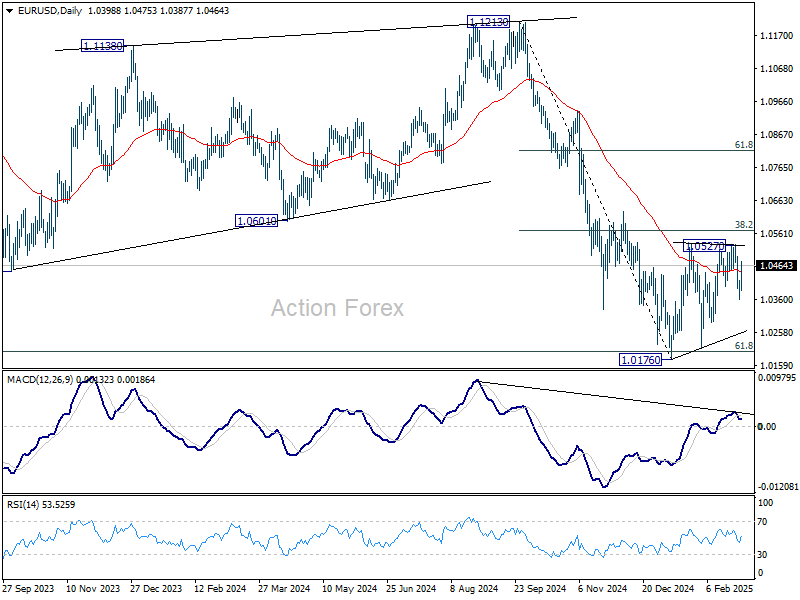

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more