Australian Dollar Dives After Poor Employment Data And Risk Off Sentiment

Australian Dollar faced a discernible decline during today’s Asian trading session, continuing its broad-based selloff throughout the week. The catalyst behind Aussie’s downturn can be traced back to the underwhelming employment figures released from Australia. Additionally, a prevailing risk-averse sentiment, inherited from US markets overnight, further burdened the risk-sensitive currency. Following closely, New Zealand Dollar emerges as the session’s second-weakest currency. Surprisingly, despite market’s cautionary mood, Japanese Yen finds no solace and positions itself as the third-worst performer.

On the other hand, Dollar is showing signs of rejuvenation, bolstered by uptick in benchmark yields. Nonetheless, it’s only managed to secure a spot behind the Sterling, making it the week’s second-strongest currency thus far. Recent market movements hint at a changing dynamic for Euro and Swiss Franc, with both currencies facing downward pressure, especially against Dollar and Pound. Yet, it’s worth noting that Euro still manages to gain a substantial lead over laggards like the Aussie and Kiwi.

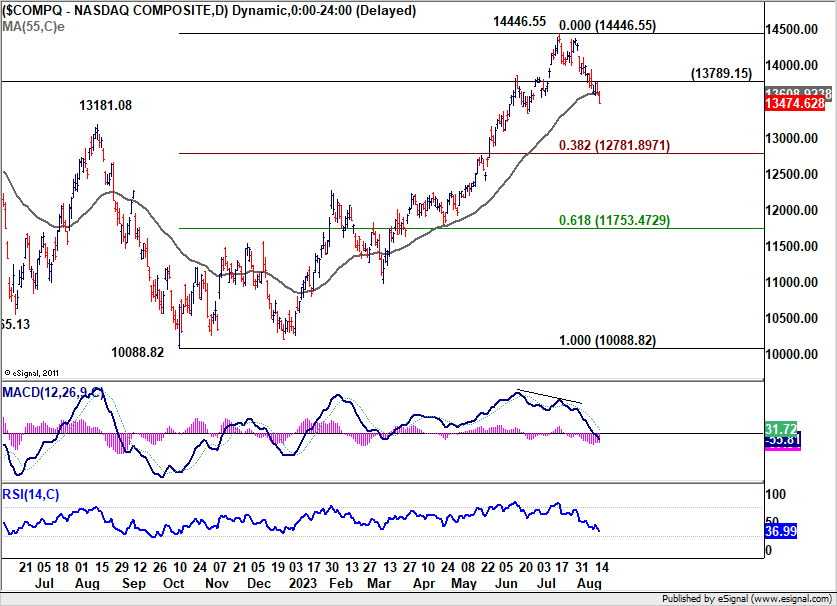

Technically, NASDAQ broke through 55 D EMA (now at 13608.92) overnight to close at 13474.62. The development now affirms that case that it’s at least in correction the whole up trend from 10088.82 (2022 low). Further decline is expected as long as 13789.15 resistance holds. Next target is 38.2% retracement of 10088.82 to 14446.55 at 12781.89. The prevailing uncertainty lies in the trajectory of the sell-off and its ripple effects on currency markets amidst the risk-averse sentiment.

In Asia, at the time of writing, Nikkei is down -0.32%. Hong Kong HSI is down -0.12%. China Shanghai SSE is up 0.01%. Japan 10-year JGB yield is up 0.0177 at 0.650. Overnight, DOW dropped -0.52%. S&P 500 dropped -0.76%. NASDAQ dropped -1.15%. 10-year yield rose 0.037 to close at 4.258.

Hawkish tilt evident in FOMC minutes, yet rate hike skepticism remains

The minutes from FOMC meeting on July 25-26 signal a clear division within the committee regarding the path of future monetary tightening, with a slight inclination towards a hawkish stance.

Despite this, market anticipation for immediate rate adjustments remains tepid. Fed fund futures indicate an 86.5% chance that Fed will maintain the status quo in September, with less than 50% probability of a rate hike by year-end.

On the stock front, NASDAQ felt the heat, declining by 1.15%, possibly reacting to Fed’s deliberations.

Within the minutes, one point was underscored: “With inflation still well above the Committee’s longer-run goal and the labor market remaining tight, most participants continued to see significant upside risks to inflation.”

Yet, counterpoints highlighted potential economic vulnerabilities and concerns about unemployment, with some members noting, “there continued to be downside risks to economic activity and upside risks to the unemployment rate.”

Additionally, a number of participants judged that risks to achieve inflation target “had become more two sided”, and wanred of the risk of “inadvertent overtightening of policy against the cost of an insufficient tightening.”

Australian employment down -14.6k, but hours worked continue to rise

Australia witnessed a contraction in employment by -14.6k in July, starkly missing expectations of a 15.2k growth. This decline was majorly attributed to a drop in full-time jobs by -24.2k, even as part-time employment saw an increase of 9.6k.

Unemployment rate rose from 3.5% to 3.7%, surpassing market anticipations which had pinned it at 3.6%. The participation rate also registered a dip, moving from 66.8% to 66.7%.

However, it wasn’t all bleak. Monthly hours worked showed a marginal increase of 0.2% mom. Commenting on this aspect, Bjorn Jarvis, ABS head of labour statistics, observed, “The strength in hours worked shows that it continues to be a tight labour market.”

Jarvis pointed out that hours worked have risen by an impressive 5.2% compared to July 2022, a significant outperformance relative to the 2.8% annual increase in employment.

He further noted, “The strength in hours worked over the past year, relative to employment growth, shows the demand for labour is continuing to be met, to some extent, by people working more hours.”

RBNZ Orr: We don’t feel a rush to be changing rates anytime soon

In a Bloomberg TV interview, RBNZ Governor Adrian Orr indicated that a forthcoming mild recession is the “bare minium” for New Zealand, as “demand has been well outstripping the pace of the supply capacity.”

“We need to see subdued consumer spending, business investment and government constraints on spending, these are a critical part of the inflation process,” he added.

Orr also reiterated that interest rate will need to stay high for a period of time, as “we don’t feel a rush to be changing rates anytime soon.”

“We believe if we stay where we are for long enough, inflation will be back inside the target band mid-next year and, and stay there,” he added.

RBNZ projects OCR to peak at 5.59% in mid-2024, then retract slightly to 5.36% by early 2025. This suggests rate cuts might be off the table for about 18 months. Orr clarified that these figures are projections and “signal or constraint.”

Japans’ export contracts in Jul, shipments to China fell for 8th month

Japan Witnesses First Export Contraction in Over Two Years Amidst Declining Trade with China

Japan’s exports experienced a dip of -0.3% yoy to JPY 8725B in July. This contraction is noteworthy as it breaks a growth streak that has lasted for over two years since February 2021.

Diving deeper into the data, while shipments to US and Europe saw a positive trajectory with respective rises of 13.5% yoy and 12.4% yoy, the trade dynamics with China narrated a different story.

Exports to China, Japan’s primary trading ally, plummeted by -13.4%, marking the steepest decline since January. Notably, this reflects an ongoing trend with shipments to China diminishing for the eighth consecutive month, subsequent to a -10.9% yoy drop in June.

On the import front, Japan registered a decline of -13.5% yoy to JPY 8804B. This marks the fourth consecutive month of declining imports and is the most significant dip since September 2020. The downturn can be partly attributed to the decreasing commodities prices.

With imports exceeding exports, trade balance for the month ended in a deficit of JPY -78.7B.

When observing the figures in seasonally adjusted terms, both exports and imports displayed a 2.0% mom rise, amounting to JPY 8460B and JPY 9018B respectively. Consequently, trade deficit widened slightly, reaching JPY -557B.

Looking ahead

Eurozone trade balance will be release in European session. US will release jobless claims and Philly Fed survey.

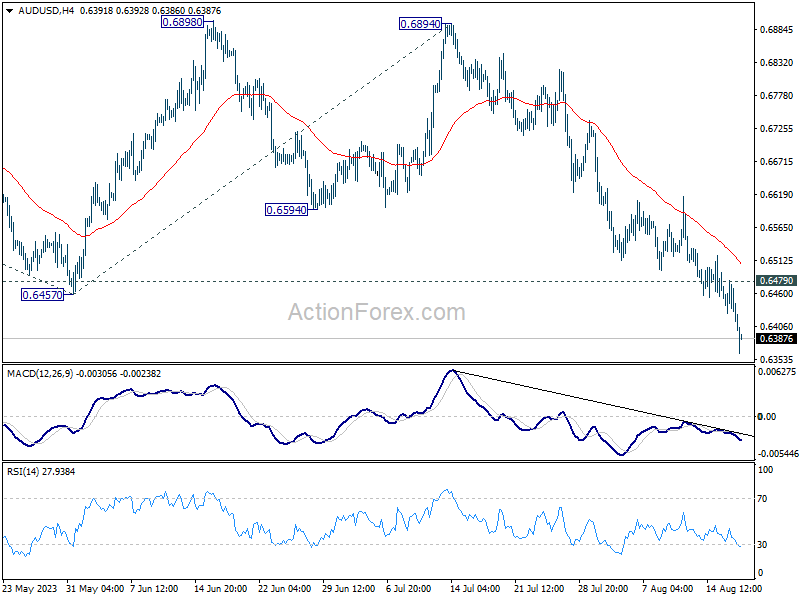

AUD/USD Daily Report

Daily Pivots: (S1) 0.6400; (P) 0.6440; (R1) 0.6464; More…

Intraday bias in AUD/USD remains on the downside at this point, as decline from 0.7156 extends. Next target is 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195. On the upside, above 0.6479 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

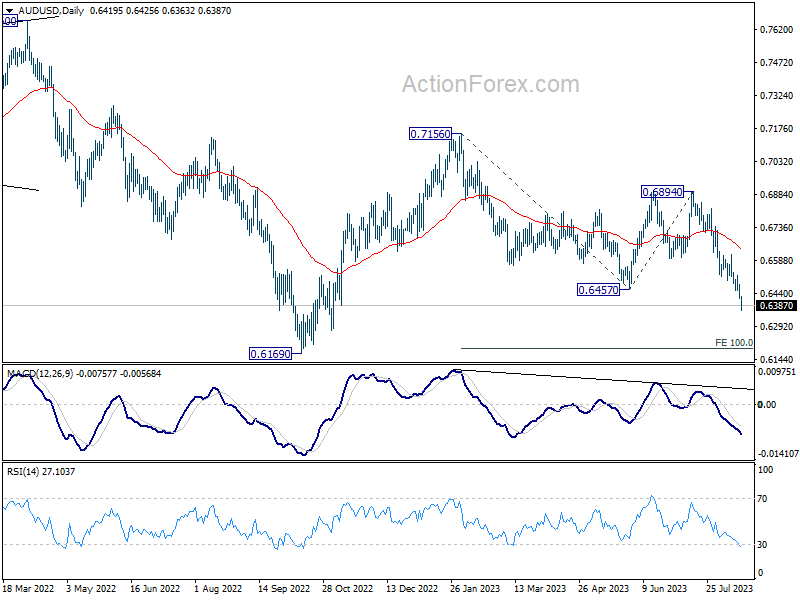

In the bigger picture, the down trend from 0.8006 (2021 high) could still be in progress. Break of 0.6457 support affirms this bearish case. Further break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | PPI Input Q/Q Q2 | -0.20% | 0.40% | 0.20% | 0.00% |

| 22:45 | NZD | PPI Output Q/Q Q2 | 0.20% | 0.80% | 0.30% | 0.20% |

| 23:50 | JPY | Trade Balance (JPY) Jul | -0.56T | -0.44T | -0.55T | -0.54T |

| 23:50 | JPY | Machinery Orders M/M Jun | 2.70% | 3.60% | -7.60% | |

| 01:30 | AUD | Employment Change Jul | -14.6K | 15.2K | 32.6K | 31.6K |

| 01:30 | AUD | Unemployment Rate Jul | 3.70% | 3.60% | 3.50% | |

| 04:30 | JPY | Tertiary Industry Index M/M Jun | -0.40% | -0.10% | 1.20% | 1.00% |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jun | 2.3B | -0.9B | ||

| 12:30 | USD | Initial Jobless Claims (Aug 11) | 240K | 248K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Aug | -9.5 | -13.5 | ||

| 14:30 | USD | Natural Gas Storage | 35B | 29B |

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more