USD/JPY Nears 150, AUD/NZD Slides; US Data, RBA And RBNZ Eyed

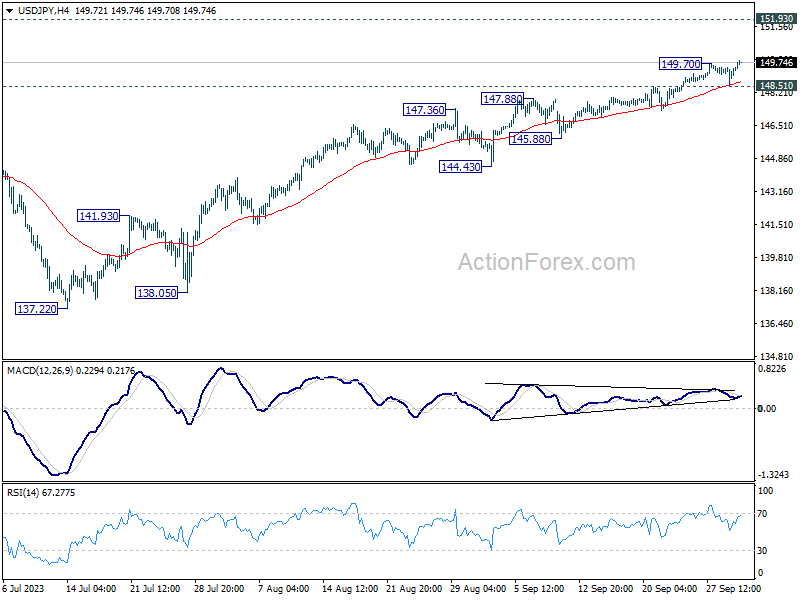

USD/JPY is making notable advances today, resuming recent up trend, and edging closer to 150 psychological handle. AT the same time, Nikkei rebounds, reclaiming 32000 mark. The combined risk-on sentiment could be attributed to investors’ positive response to the optimistic quarterly Tankan survey results, overshadowing the less favorable PMI Manufacturing data.

Despite Japan’s repeated attempts at verbal interventions, their impact appears to be waning as market players seem getting increasingly indifferent to these remarks. A focus is now shifting to the sustainability of USD/JPY’s current upside momentum, especially as the greenback is poised to face significant tests with the release of ISM indexes and non-farm payroll data in the coming data.

In the broader currency market panorama, Canadian dollar is riding the wave alongside US Dollar. Contrarily, Australian and New Zealand Dollars are trailing, displaying weakness in tandem with Yen. Sterling and Swiss Franc are exhibiting slight softness against Euro, but movements between European majors remain within familiar ranges.

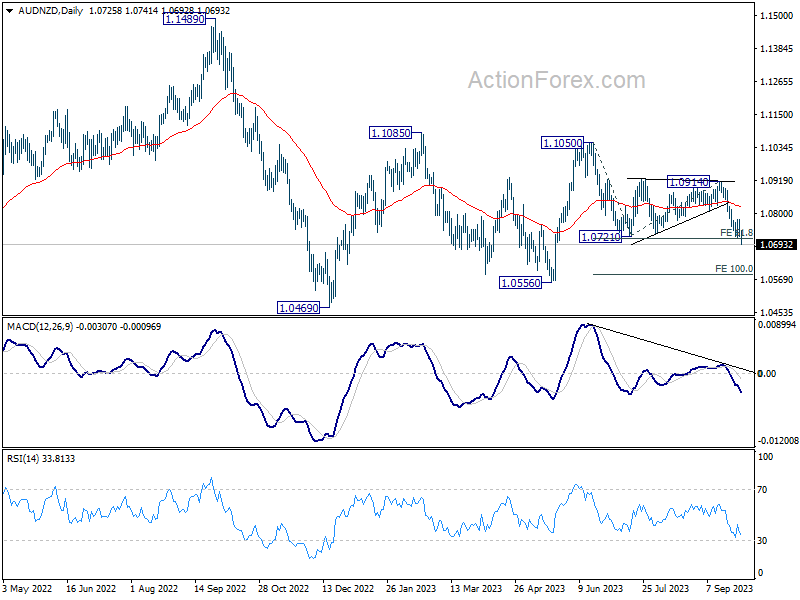

An essential development to monitor is the ongoing decline of AUD/NZD, especially with upcoming rate decisions from both RBA and RBNZ. Analysts predict both banks to maintain their interest rates unchanged. Technically, near term outlook in AUD/NZD will remain bearish as long as 1.0779 resistance holds. With 61.8% projection of 1.1050 to 1.0721 from 1.0914 at 1.0711 taken out, next target is 100% projection at 1.0585. Reaction from there will reveal whether the cross is resuming the down trend from 1.1489 (2022 high).

In Asia, at the time of writing, Nikkei is up 0.25%. Japan 10-year JGB yield is up 0.0087 at 0.780. Singapore Strait Times is down -0.08%. Hong Kong and China are on holiday.

In Asia, at the time of writing, Nikkei is up 0.25%. Japan 10-year JGB yield is up 0.0087 at 0.780. Singapore Strait Times is down -0.08%. Hong Kong and China are on holiday.

BoJ opinions: A blend of caution and optimism

Summary of Opinions of BoJ’s September 21-22 meeting reiterated the general stance that ultra-loose monetary policy remains necessary for now. Yet, there was an undercurrent of optimism, with some members seeing achieve of price target “in sight”.

The collective view reinforced that the “sustainable and stable achievement of the price stability target, accompanied by wage increases, has not yet come in sight.” Given this scenario, the summary stressed the necessity to “patiently continue with monetary easing under yield curve control.”

Underpinning the continued focus on wages, one member stated it is “necessary” to uphold the “momentum for wage hikes through continuation of monetary easing.” Also, in order to achieve inflation target of 2 percent in a sustainable manner, it is necessary that “wage increases take root.”

However, amid the cautious tones, rays of optimism emerged. One member opined that “Japan’s economy is getting closer to achieving the price stability target, although there is somewhat of a distance to go.” Providing a potential timeline for evaluating the price stability objective, focus is now on “the second half of fiscal 2023” especially considering the wage growth prospects for 2024.

Furthering this optimism, another viewpoint conveyed confidence, indicating that “Achievement of 2 percent inflation in a sustainable and stable manner seems to have clearly come in sight.” This perspective also hinted at a clearer outcome by “January to March of next year.”

Japan’s Tankan survey reveals strong business sentiment

The latest Tankan survey results in Q3 showcased strengthening corporate sentiment in Japan. Key indices and outlooks, along with projections for capital expenditure, underscore a robust business environment, as inflation expectations maintain steadiness.

Large Manufacturing Index showed notable gains from 5 to 9, marking its second consecutive quarter of growth. Concurrently, Large Non-Manufacturing Index advanced from 23 to 27, recording its best level since 1991 and marking its sixth straight quarter of improvement.

Further reflecting this positive trend, Large Manufacturing Outlook Index increased from 9 to 10, while its Large Non-Manufacturing Outlook saw an ascent from 20 to 21.

In terms of capital commitments, prominent firms revealed ambitious plans, with an anticipation to bolster capital expenditure by 13.6% for the fiscal year ending March 2024.

Regarding inflation, the corporate sector’s expectations remain consistent. Firms anticipate a price increase of 2.5% in the upcoming year, 2.2% over a three-year horizon, and 2.1% looking five years ahead. These figures mirror projections made in the prior quarter.

A crucial insight from a BOJ official noted that many large businesses have successfully offset higher costs by adjusting consumer prices, subsequently enhancing the overall business sentiment.

Further elevating the positive mood have been factors such as a resurgence in auto production and declining costs for raw materials. However, the official also acknowledged the challenges faced by some smaller enterprises, which have found it difficult to raise their prices.

Japan PMI manufacturing finalized at 48.5 in Sep, headwinds at home and abroad

Japanese manufacturing sector is facing challenges as evidenced by the drop in PMI Manufacturing to 48.5 in September, down from August’s 49.6, the lowest level since February. Additionally, the average reading for Q3 stands at 49.3, a reduction from 50.0 in Q2.

According to key findings by S&P Global, the sector experienced faster falls in production and incoming new work. Alarmingly, backlogs declined at the strongest rate since April. A specific area of concern is the accelerated rate of input price inflation, reaching a four-month high, fueled by increasing costs of raw materials, oil, freight, and energy.

Usamah Bhatti at S&P Global Market Intelligence, conveyed a sombre view of the situation. He noted, “Depressed economic conditions domestically and globally weighed heavily on the sector, as both output and new orders were scaled back further. The decline in the latter was notably sharp, and the strongest seen for seven months.” The future outlook is also tinged with apprehension, as manufacturers signaled the most significant depletion in outstanding business in five months.

The inflationary aspect further complicates the picture. Bhatti highlighted, “The rate of input price inflation accelerated for the second month running to a four-month high.” Reports indicated that the sustained weakness of the yen is exacerbating the situation, elevating prices for inputs from abroad and placing an additional strain on firms.

RBA, RBNZ and US Data Deluge

This week, the spotlight shines on the meetings of two central banks and a slew of significant US economic data.

RBA, under the stewardship of its new Governor Michelle Bullock, is stepping into the limelight. With expectations anchored on continuation of 4.10% interest rate, the focus shifts to any potential hints of a future trajectory, especially amidst the backdrop of a slight uptick in the monthly CPI in . With Q3 data largely veiled in obscurity, concrete guidance is anticipated to be sparse, leaving market analysts and investos to decipher subtler cues.

Across the waters, RBNZ is another focal point. Holding a pioneering stance in post-COVID rate hikes, speculations are rife on whether RBNZ could also be the trailblazer in reversing the trend with rate cuts in the forthcoming year. However, consensus is elusive. Some economic pundits are forecasting an opposite movement, anticipating a hike to 5.75% come November or an increment early next year. Yet, with Q3 data conspicuously absent, tangible guidance from RBNZ remain improbable.

In the US, a busy week unfurls with ISM reports and non-farm payroll data taking center stage. These releases are imbued with heightened significance following last week’s softer-than-projected core inflation figures. Fed fund futures currently indicate a sub-35% probability of a rate hike by year-end. A pressing query emerges – is the US economy, especially services sector and employment, moderating sufficiently to douse inflationary pressures, or is it on the brink of a more pronounced downturn, heralding a recession?

Complicating the narrative is the potential disarray in the data release schedule, courtesy of the partial government shutdown. This adds another layer of uncertainty, rendering the task of gauging economic health and future directions more intricate.

Here are some highlights for the week:

- Monday: BoJ summary of opinions, Japan Tankan survey, PMI manufacturing final; Swiss retail sales, PMI manufacturing; Eurozone PMI manufacturing final, unemployment rate; UK PMI manufacturing final; US ISM manufacturing construction spending.

- Tuesday: Japan monetary base; RBA rate decision, Australia building approvals; Swiss CPI.

- Wednesday: RBNZ rate decision; Eurozone PMI services final, PPI, retail sales; UK PMI services final; US ADP employment, ISM services, factory orders.

- Thursday: Australia trade balance; Germany trade balance; France industrial production; UK PMI construction; Canada trade balance, Ivey PMI; US jobless claims, trade balance.

- Friday: Japan average cash earnings, household spending, leading indicators; Swiss unemployment rate; Germany factory orders; France trade balance; Swiss foreign currency reserves; Canada employment; US non-farm payrolls.

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.76; (P) 149.13; (R1) 149.73; More…

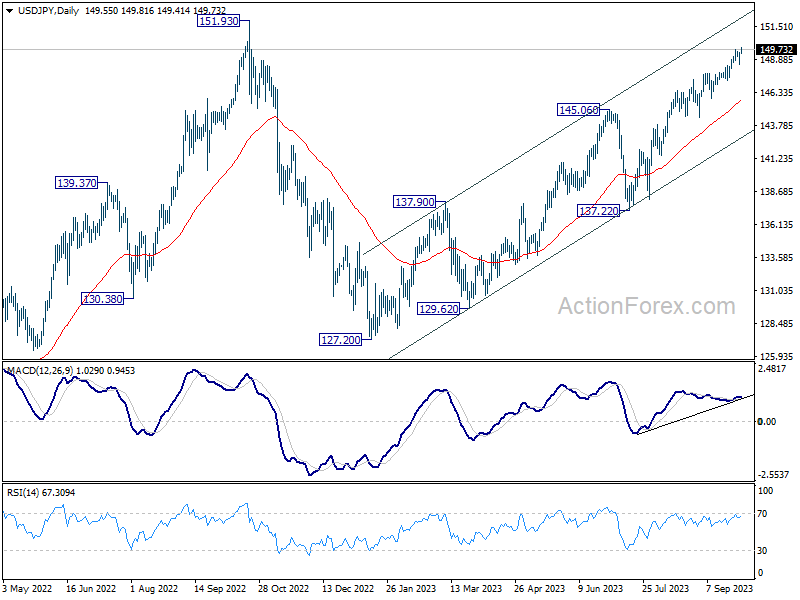

USD/JPY’s rally resumed today by breaking through 149.70 resistance and intraday bias is back on the upside. Current rise from 127.20 should target a retest on 151.93 high next. On the downside, break of 148.51 support is needed to indicate short term topping. Otherwise, outlook will stay bullish in case of retreat.

In the bigger picture, while rise from 127.20 is strong, it could still be seen as the second leg of the corrective pattern from 151.93 (2022 high). Rejection by 151.93, followed by break of 145.06 resistance turned support will be the first sign that the third leg of the pattern has started. However, sustained break of 151.93 will confirm resumption of long term up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 23:50 | JPY | Tankan Large Manufacturing Index Q3 | 9 | 6 | 5 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q3 | 10 | 5 | 9 | |

| 23:50 | JPY | Tankan Non – Manufacturing Index Q3 | 27 | 24 | 23 | |

| 23:50 | JPY | Tankan Non – Manufacturing Outlook Q3 | 21 | 22 | 20 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q3 | 13.60% | 13.40% | ||

| 00:00 | AUD | TD Securities Inflation M/M Sep | 0.00% | 0.20% | ||

| 00:30 | JPY | Manufacturing PMI Sep F | 48.5 | 48.6 | 48.6 | |

| 06:30 | CHF | Real Retail Sales Y/Y Aug | -1.80% | -2.20% | ||

| 07:30 | CHF | Manufacturing PMI Sep | 40.5 | 39.9 | ||

| 07:45 | EUR | Italy Manufacturing PMI Sep | 45.6 | 45.4 | ||

| 07:50 | EUR | France Manufacturing PMI Sep F | 43.6 | 43.6 | ||

| 07:55 | EUR | Germany Manufacturing PMI Sep F | 39.8 | 39.8 | ||

| 08:00 | EUR | Italy Unemployment Aug | 7.70% | 7.60% | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Sep F | 43.4 | 43.4 | ||

| 08:30 | GBP | Manufacturing PMI Sep F | 44.2 | 44.2 | ||

| 09:00 | EUR | Eurozone Unemployment Rate Aug | 6.40% | 6.40% | ||

| 13:30 | CAD | Manufacturing PMI Sep | 48 | |||

| 13:45 | USD | Manufacturing PMI Sep F | 48.9 | 48.9 | ||

| 14:00 | USD | ISM Manufacturing PMI Sep | 47.9 | 47.6 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Sep | 48.9 | 48.4 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Sep | 48.5 | |||

| 14:00 | USD | Construction Spending M/M Aug | 0.60% | 0.70% |

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more