Sterling Takes A Dive As UK Inflation Data Ease Some Pressure On BoE

Sterling falls sharply following the release of June’s UK CPI figures which revealed faster than expected slowdown in both headline and core inflation. Despite the persistent high inflation levels, these figures suggest BoE may not need to raise interest rates as aggressively as previously anticipated by some economists, potentially easing some monetary policy pressures. In response to the inflation data, notable decreases were observed in both German and US benchmark yields, potentially giving Yen and Swiss Franc a little favor ahead.

Elsewhere in the current markets, Kiwi and Aussie are following the Pound as next weakest. Japan’s Nikkei does follow US markets higher today, but other Asian markets are just sluggish. Canadian Dollar is the relatively stronger one for now, followed by Swiss Franc and Dollar while Euro is mixed.

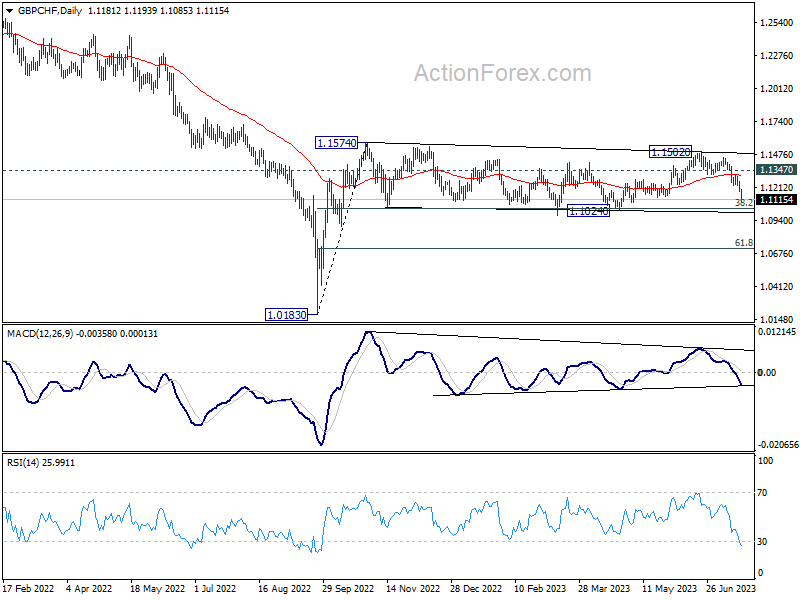

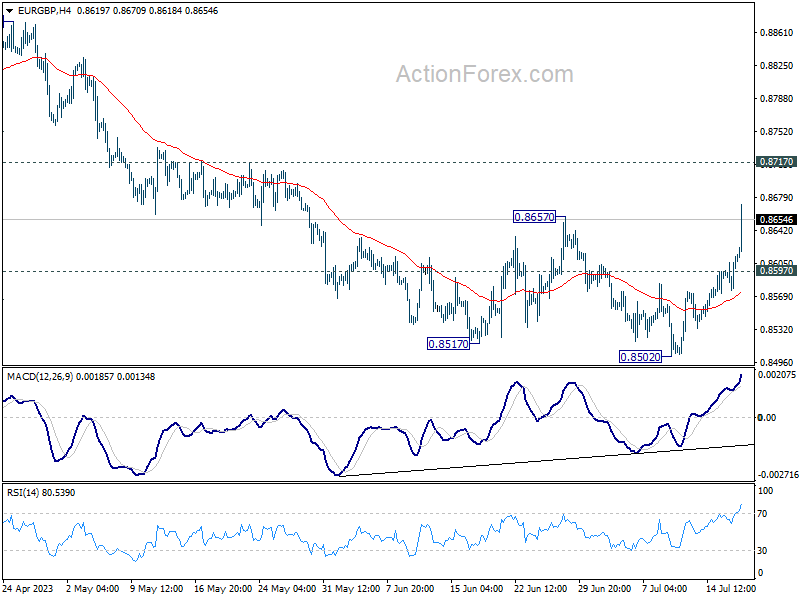

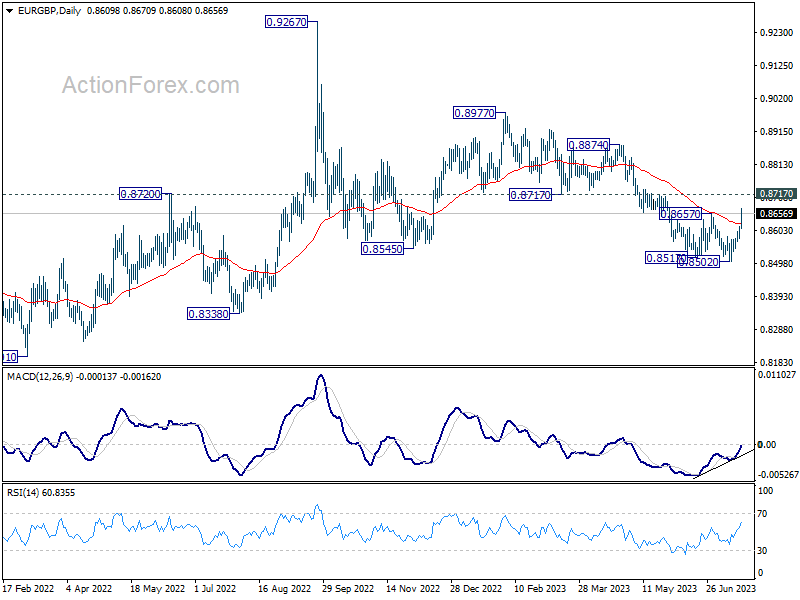

Technically, EUR/GBP’s strong rally and break of 0.8657 resistance confirms shot term bottoming at 0.8502. The development also raises the chance of larger bullish reversal.. As GBP/CHF is diving hard today, focus is back on 1.1024 support, which is close to 38.2% retracement of 1.0183 to 1.1574. Strong support could still be seen from there this time. But decisive break there could prompt steeper selloff in GBP/CHF to 61.8% retracement at 1.0174. Weakness in Sterling could then spread from these two crosses to other pairs.

In Asia, Nikkei closed up 1.24%. Hong Kong HSI is down -0.42%. China Shanghai SSE is down -0.01%. Singapore Strait Times is up 0.55%. Japan 10-year JGB yield is down -0.015 at 0.472. Overnight DOW rose 1.06%. S&P 500 rose 0.71%. NASDAQ rose 0.76%. 10-year yield dropped -0.008 to 3.789.

UK CPI eased to 7.9% in Jun, core CPI down to 6.9%, both below expectations

UK CPI slowed from 8.7% yoy to 7.9% yoy in June, below expectation of 8.2% yoy. Core CPI (excluding energy, food, alcohol and tobacco) slowed from 7.1% yoy to 6.9% yoy, below expectation of staying unchanged at 7.1% yoy.

CPI goods slowed from 9.7% yoy to 8.5% yoy. CPI services also eased from 7.4% yoy to 7.2% yoy.

On a monthly basis, CPI rose just 0.1% mom, down from May’s 0.7% mom. Falling prices for motor fuel led to the largest downward contribution to the monthly change.

Also released, RPI came in at 0.3% mom, 10.7% yoy, versus expectation of 0.3% mom, 10.9% yoy. PPI input was at -1.3% mom, 2.7% yoy. PPI output was at -0.3% mom, 0.1% yoy. PPI core output was at -0.20% mom, 3.00% yoy.

New Zealand’s Q2 CPI beats expectations despite slowdown

New Zealand’s CPI experienced a slightly slowed but stronger-than-expected rise in Q2, registering 1.1% qoq increase compared to Q1’s 1.2% qoq. This exceeded the anticipated 0.9% qoq rise for the quarter. Year-on-year inflation also surpassed expectations, with 6.0% yoy rise as opposed to expected 5.9% yoy, despite slowdown from 6.7% yoy in the previous quarter.

StatsNZ, New Zealand’s pointed out that food prices, which rose 2.2% qoq and 12.3% yoy, were the primary drivers of Q2 annual inflation rate. Rising prices for vegetables, ready-to-eat food, and dairy products like milk, cheese, and eggs played a significant role. Housing and household utilities, another crucial sector, experienced quarterly increase of 1.2% qoq and 6.0% yoy increase annually.

On analyzing the CPI data further, it was found that excluding food, inflation increased by 4.6% yoy. Excluding housing and household utilities, it increased by 6.1% yoy. When excluding alcoholic beverages and tobacco, the annual increase stood at 5.9% yoy. CPI increased by 6.1% yoy when food, household energy, and vehicle fuels were excluded.

Australia leading index records 11th consecutive negative month

Australia’s Westpac Leading Index rose to -0.51% in June from -1.01% in May, marking the eleventh consecutive negative print. This trend indicates that the Australian economy is likely to operate below its potential trend over the six to nine months outlook.

In light of these results, Westpac maintains a modest forecast for Australian economic growth. It expects modest expansion of 0.3% over the year to June 2024, with contraction in consumer spending of -0.2%.

Commenting on the upcoming RBA meeting on August 1, Westpac anticipates a 25 bps hike in interest rate. It noted, “By the August meeting we expect that the Board will be dealing with an inflation read still above 6%; an unemployment rate registering nearly 1ppt below the Board’s current estimate of full employment; and the recent report from the national accounts showing unit labour costs growing at 7.9% over the year.”

Looking ahead

Eurozone will release June CPI final. US will release building permits and housing starts too.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8589; (P) 0.8602; (R1) 0.8627; More…

EUR/GBP’s strong rally and break of 0.8657 resistance confirms short term bottoming at 0.8502, on bullish convergence condition in 4H and D MACD. Current development argues that fall from 0.8977 might have completed its five-wave sequence. Intraday bias is back on the upside for 0.8717 support turned resistance first. Sustained break there will solidify this case and target 0.8977 resistance next. On the downside, though, below 0.8597 will mix up the outlook and turn intraday bias neutral first.

In the bigger picture, the down trend from 0.9267 (2022 high) is seen as part of the long term range pattern from 0.9499 (2020 high). Firm break of 0.8717 support turned resistance will argue that it has completed with three waves down to 0.8502. Further break of 0.8977 will bring retest o f0.9267 high. Nevertheless, break of 0.8502 will resume the decline towards 0.8201 (2022 low).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | CPI Q/Q Q2 | 1.10% | 0.90% | 1.20% | |

| 22:45 | NZD | CPI Y/Y Q2 | 6.00% | 5.90% | 6.70% | |

| 00:30 | AUD | Westpac Leading Index M/M Jun | 0.10% | -0.30% | ||

| 06:00 | GBP | CPI M/M Jun | 0.10% | 0.40% | 0.70% | |

| 06:00 | GBP | CPI Y/Y Jun | 7.90% | 8.20% | 8.70% | |

| 06:00 | GBP | Core CPI Y/Y Jun | 6.90% | 7.10% | 7.10% | |

| 06:00 | GBP | RPI M/M Jun | 0.30% | 0.30% | 0.70% | |

| 06:00 | GBP | RPI Y/Y Jun | 10.70% | 10.90% | 11.30% | |

| 06:00 | GBP | PPI Input M/M Jun | -1.30% | -0.20% | -1.50% | -1.20% |

| 06:00 | GBP | PPI Input Y/Y Jun | -2.70% | -3.30% | 0.50% | |

| 06:00 | GBP | PPI Output M/M Jun | -0.30% | -0.30% | -0.50% | |

| 06:00 | GBP | PPI Output Y/Y Jun | 0.10% | 1.60% | 2.90% | 2.70% |

| 06:00 | GBP | PPI Core Output M/M Jun | -0.20% | -0.20% | -0.30% | -0.50% |

| 06:00 | GBP | PPI Core Output Y/Y Jun | 3.00% | 2.80% | 4.10% | 3.90% |

| 09:00 | EUR | Eurozone CPI Y/Y Jun F | 5.50% | 5.50% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun F | 5.40% | 5.40% | ||

| 12:30 | USD | Building Permits Jun | 1.48M | 1.49M | ||

| 12:30 | USD | Housing Starts Jun | 1.47M | 1.63M | ||

| 14:30 | USD | Crude Oil Inventories | -2.0M | 5.9M |

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more