Sterling Jumps On Record Wages Growth, Gold Approaches Key Support

European major currencies are making a notable stride today, with Sterling at the forefront. The Pound ascent is attributed to the historic high recorded in UK regular wage growth. This surge adds further weight to BoE dilemma, pushing it to seriously consider additional monetary tightening in the upcoming month.

While Dollar is making efforts to recoup some of its recent losses, spurred by positive retail sales data surpassing expectations, its upward momentum is noticeably tepid. Canadian Dollar, despite higher than expected inflation figures, has largely been indifferent. This places it in tandem with Australian and New Zealand Dollars, both vying for the least impressive performance of the day. Floating somewhere in the midst, Japanese Yen presents a mixed bag—losing ground against Dollar and Europeans, yet holding its own versus commodity-linked currencies.

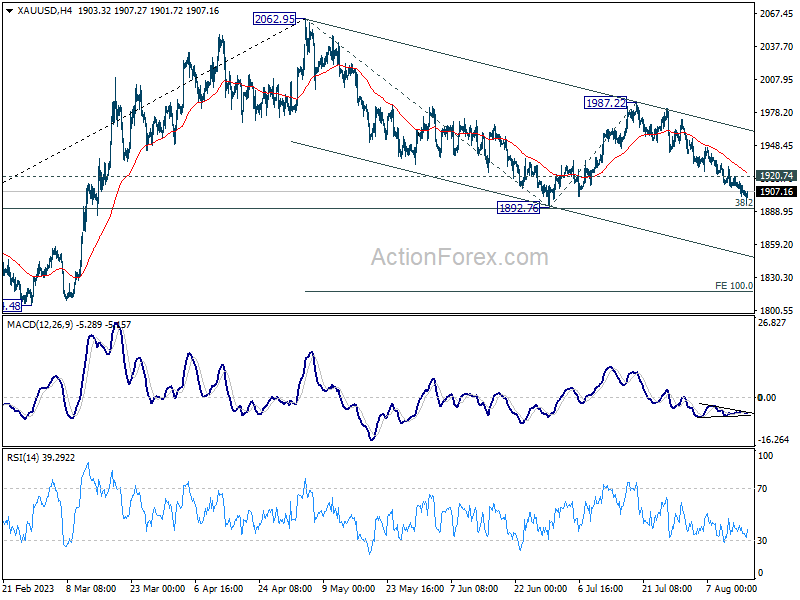

Technically, Gold is now approaching key support level at 1892.76 as the fall from 1987.22 extends. Strong rebound from current level, followed by break of 1920.74 minor resistance, will at least indicate some stabilization, with prospect for further rise back towards 1987.22 resistance. However, sustained break of 1892.76 will risk downside acceleration to 100% projection of 2062.95 to 1892.76 from 1987.22 at 1817.06. Under such a bearish scenario, this would likely serve as a green light for the Dollar to momentum, propelling it higher against other major rivals.

In Europe, at the time of writing, FTSE is down -1.20%. DAX is down -0.78%. CAC is down -0.88%. Germany 10-year yield is up 0.0528 at 2.691. Earlier in Asia, Nikkei rose 0.56%. Hong Kong HSI dropped -1.03%. China Shanghai SSE dropped -0.07%. Singapore Strait Times dropped -0.46%. Japan 10-year JGB yield rose 0.0131 to 0.632.

US retail sales rose 0.7% mom in Jul, ex-auto sales up 1.0% mom

US retail sales rose 0.7% mom to USD 696.4B in July, above expectation of 0.4% mom. Ex-auto sales rose 1.0% mom to USD 562.8B, above expectation of 0.4% mom. Ex-gasoline sales rose 0.8% mom to USD 644.0B. Ex-auto, gasoline sales rose 1.0% mom to USD 510.5B.

Total sales for May 2023 through July 2023 period were up 2.3% from the same period a year ago.

Canada CPI rose to 3.3% yoy in Jul, up 0.6% mom

Canadian inflation, measured by CPI, accelerated in July, posting a 0.6% mom increase, doubling expected rise of 0.3% mom. This upward tick, a substantial leap from June’s 0.1% gain, was significantly influenced by higher travel tour prices.

On a year-on-year basis, July’s CPI leapt from 2.8% yoy to 3.3% yoy , outpacing anticipated 3.0% yoy . A notable factor behind the rapid rise in the headline consumer inflation is base-year effect in gasoline prices. The previous year’s steep decline in gasoline prices for July 2022, which saw a -9.2% drop, has ceased to affect the current 12-month trajectory.

Excluding gasoline, CPI rose 4.1% yoy, edging up from 4.0% yoy in June. Excluding energy, CPI decelerated to 4.2% yoy after 4.4% yoy increase in June.

CPI median slowed from 3.9% yoy to 3.7% yoy, matched expectations. CPI trimmed down from 3.7% yoy to 3.6% yoy, above expectation of 3.5% yoy. CPI common also fell from 5.1% yoy to 4.8% yoy, below expectation of 5.0% yoy.

German ZEW rose to -12.3, but current situation dived

August’s ZEW Economic Sentiment Index for Germany showed an unexpected improvement, moving from -14.7 to -12.3, beating forecasted -15. However, the Current Situation index took a hit, declining sharply from -59.5 to -71.3—its lowest since October 2022 and below the predicted -63.

Conversely, Eurozone’s ZEW Economic Sentiment took an optimistic turn, rising from -12.2 to -5.5, surpassing expected -12. Current Situation Index in the Eurozone also advanced, marking a rise of 2.3 points to -42.0.

ZEW President Professor Achim Wambach commented on the mixed results, noting, “The ZEW Indicator of Economic Sentiment remains in negative territory” but added that there’s an anticipated “slight uptick in the economic situation by year-end.”

However, he cautioned against over-optimism due to Germany’s worsening current economic assessment. Highlighting external influences, Wambach mentioned that the prevailing sentiment suggests no further “interest rate hikes in the eurozone and the United States.” He also pointed out a “significant increase” in US economic outlook, which positively impacts Germany’s prospects.

UK payrolled employment rose 97k in Jul, unemployment rate at 4.2% in Jun

UK payrolled employment grew 97k, or 0.3% mom in July. June’s figure was revised from -9k decrease to 47k increase. Median monthly pay rose 7.8% yoy compare with July 2022, down from prior month’s 9.7% yoy. Claimant count rose 29.0k, above expectation of 19.6k.

In the three months to June, unemployment rate rose to 4.2%, above expectation of 4.0%. That’s 0.3% higher than previous quarter. Employment rate rose 0.1% to 75.7%. Inactivity rate fell -0.1% to 20.9%. Average earnings including bonus rose 8.2% 3moy, above expectation of 7.3%. Average earnings excluding bonus rose 7.8% 3moy, above expectation of 7.4%, and hit the highest level on record.

China: Unexpected rate cut by PBOC aligns with disheartening July economic data

In an unexpected decision that took markets by surprise, PBoC announced a cut in key policy rates for the second time in a span of three months, just an hour before the release of July economic data that broadly fell short of market expectations.

PBOC lowered the rate on its one-year medium-term lending facility loans – valued at CNY 401B – to financial institutions by 15bps to 2.50% from the previous 2.65%. This significant move indicates the possibility of a reduction in China’s benchmark loan prime rate in the upcoming week.

A closer look at the economic metrics for July reveals concerns. Industrial production grew at 3.7% yoy, underperforming against the anticipated 4.3% yoy and marking a slowdown from the 4.4% yoy of the previous month. Similarly, retail sales saw increase of just 2.5% yoy, lagging behind projected 4.2% yoy and decelerating from 3.1% yoy. This rate marks the slowest growth pace in sales since the decline observed in December 2022. Furthermore, fixed asset investment growth, year-to-date year-on-year, was recorded at 3.4%, falling short of 3.8% expectation.

Urban unemployment rate witnessed a slight increase, moving from 5.2% to 5.3%. Notably, NBS did not provide the usual age breakdown of unemployment figures. The spokesperson mentioned the suspension of youth unemployment data attributing it to societal and economic changes, and highlighted an ongoing reassessment of its data collection methodology. It’s worth noting that in June, the youth unemployment rate (for ages 16-24) reached a record high of 21.3%

NBS also said in a statement, “We must intensify the role of macro policies in regulating the economy and make solid efforts to expand domestic demand, shore up confidence and prevent risks.”

Japan’s Q2 GDP grew 6% annualized, external demand drives growth

Japan witnessed a stellar performance in its Q2 GDP, registering a growth of 1.5% Qoq, a figure that comfortably surpassed the anticipated 0.8% qoq rise. In annualized terms, growth clocked in at 6.0%, notably higher than expected 3.1%. This rapid expansion marked the quickest pace since the October-December period of 2020 and signifies the third consecutive quarterly growth.

A significant driver of this growth was a 3.2% surge in exports during the quarter. The rejuvenation in external demand, particularly net exports, added a substantial 1.8% to the quarter’s growth. The auto exports sector reaped benefits from the alleviation of supply disruptions, while a consistent uptick in international tourists bolstered the economy. On the flip side, imports dipped by -4.3% as energy and COVID vaccine imports declined.

A closer look at the domestic sector unveils a few challenges. Private consumption, a sector that constitutes over half of the economy, contracted by -0.5% on a quarterly basis. This resulted in domestic demand cutting -0.3% from growth. The mounting prices of regular commodities affected consumer spending negatively. Furthermore, sales of durable goods took a hit, which overshadowed the robust demand for services.

In terms of capital investment, the growth remained tepid, registering just a 0.03% increase. However, it’s noteworthy that this was buoyed by spending related to software, marking its second successive quarter of rise.

RBA sees credible path back to inflation target with interest rate at present level

In the minutes from RBA’s August 1 meeting, board members weighed the decision between raising cash rate by 25bps or maintaining its unchanged.

The board’s inclination to hold the rate steady was rooted in their belief that prior tightening measures were “working as intended.” Despite the full effects not yet being evident in the data, there were important signs, as “consumption had already slowed significantly”, “labour market might be at a turning point”, and “inflation was heading in the right direction”.

The board observed a “credible path back to the inflation target with the cash rate staying at its present level.” This assessment seemed to be “broadly in line with the staff’s central forecasts.” Solidifying their position, members collectively agreed that the reasons to “leave the cash rate unchanged at this meeting was the stronger one.”

Meanwhile, they also acknowledged that “further tightening of monetary policy might be required” to consistently meet inflation goals. Such decisions will be driven by data trends and ongoing risk assessments.

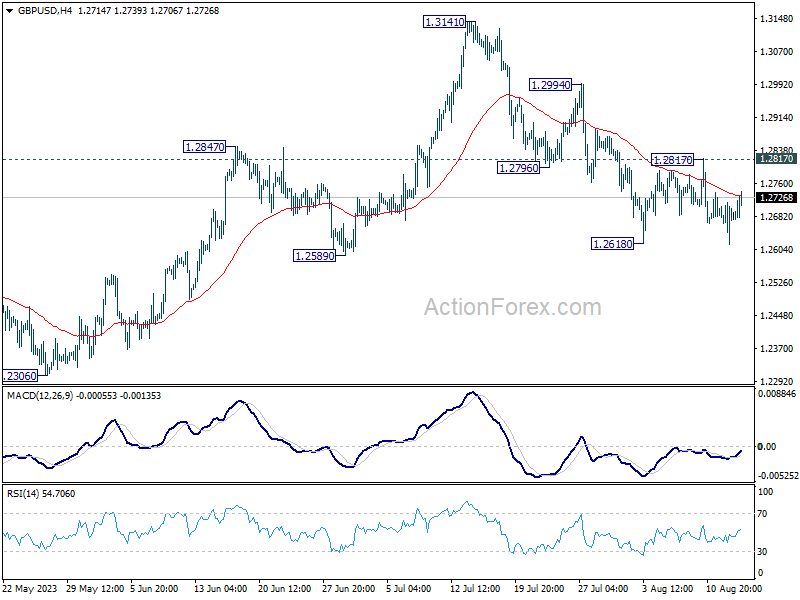

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2631; (P) 1.2673; (R1) 1.2729; More…

GBP/USD recovers notably today but stays below 1.2817 resistance. Intraday bias remains neutral at this point. On the downside, firm break of 1.2618, and sustained trading below 1.2678 resistance turned support will argue that it’s already in a larger correction. Deeper decline would then be seen to 1.2306 support next. Nevertheless, break of 1.2817 minor resistance will indicate that the pull back has completed, and turn bias back to the upside for stronger rebound.

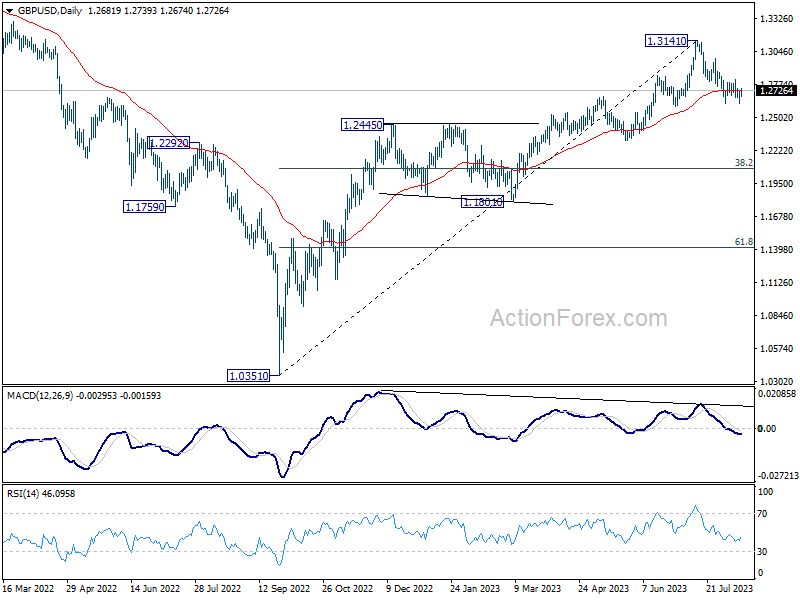

In the bigger picture, a medium term top could be in place at 1.3141 already, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.2723) should confirm this case, and bring deeper fall to 38.2% retracement of 1.0351 to 1.3141 at 1.2075, as a correction to up trend from 1.0351 (2022 low). For now, rise will stay mildly on the downside as long as 1.3141 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | GDP Q/Q Q2 P | 1.50% | 0.80% | 0.70% | |

| 23:50 | JPY | GDP Deflator Y/Y Q2 P | 3.40% | 3.80% | 2.00% | |

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 01:30 | AUD | Wage Price Index Q/Q Q2 | 0.80% | 1.00% | 0.80% | |

| 02:00 | CNY | Industrial Production Y/Y Jul | 3.70% | 4.30% | 4.40% | |

| 02:00 | CNY | Retail Sales Y/Y Jul | 2.50% | 4.20% | 3.10% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jul | 3.40% | 3.80% | 3.80% | |

| 04:30 | JPY | Industrial Production M/M Jun F | 2.40% | 2.00% | 2.00% | |

| 06:00 | GBP | Claimant Count Change Jul | 29.0K | 19.6K | 25.7K | 16.2K |

| 06:00 | GBP | ILO Unemployment Rate (3M) Jun | 4.20% | 4.00% | 4.00% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jun | 8.20% | 7.30% | 6.90% | 7.20% |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jun | 7.80% | 7.40% | 7.30% | 7.50% |

| 06:30 | CHF | Producer and Import Prices M/M Jul | -0.10% | 0.20% | 0.00% | |

| 06:30 | CHF | Producer and Import Prices Y/Y Jul | -0.60% | -0.50% | -0.60% | |

| 09:00 | EUR | Germany ZEW Economic Sentiment Aug | -12.3 | -15 | -14.7 | |

| 09:00 | EUR | Germany ZEW Current Situation Aug | -71.3 | -63 | -59.5 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Aug | -5.5 | -12 | -12.2 | |

| 12:30 | CAD | Manufacturing Sales M/M Jun | -1.70% | -2.10% | 1.20% | |

| 12:30 | CAD | CPI M/M Jul | 0.60% | 0.30% | 0.10% | |

| 12:30 | CAD | CPI Y/Y Jul | 3.30% | 3.00% | 2.80% | |

| 12:30 | CAD | CPI Media Y/Y Jul | 3.70% | 3.70% | 3.90% | |

| 12:30 | CAD | CPI Trimmed Y/Y Jul | 3.60% | 3.50% | 3.70% | |

| 12:30 | CAD | CPI Common Y/Y Jul | 4.80% | 5.00% | 5.10% | |

| 12:30 | USD | Empire State Manufacturing Index Aug | -19 | -0.3 | 1.1 | |

| 12:30 | USD | Retail Sales M/M Jul | 0.70% | 0.40% | 0.20% | 0.30% |

| 12:30 | USD | Retail Sales ex Autos M/M Jul | 1.00% | 0.40% | 0.20% | |

| 12:30 | USD | Import Price Index M/M Jul | 0.40% | 0.20% | -0.20% | |

| 14:00 | USD | Business Inventories Jun | 0.20% | 0.20% | ||

| 14:00 | USD | NAHB Housing Market Index Aug | 56 | 56 |

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more