Safe-Haven Demand Fuels Dollar Rally Amid Trade, Geopolitical Turmoil

Market sentiment took a decisive turn for the worse last week, with risk aversion dominating across asset classes. The combination of deteriorating domestic economic conditions in the US and heightened global uncertainties has fueled concerns that risk appetite could weaken further. Equities faced renewed selling pressure, yields dropped sharply.

Domestically, US economic data painted a troubling picture. Consumer confidence deteriorated sharply, while weak personal spending data and a rise in jobless claims suggested that the labor market could be facing new headwinds. With the economy looking increasingly fragile, concerns are mounting that the economy may struggle to maintain momentum, reinforcing speculation about Fed rate cuts.

Externally, the risk of a full-blown trade war continues to escalate. US President Donald Trump doubled down on his aggressive tariff agenda, reaffirming the March 4 deadline for 25% tariffs on Canada and Mexico and indicating that the EU would be next in line with reciprocal tariffs.

Geopolitical tensions also worsened, particularly after a dramatic Oval Office showdown between Trump, Vice President JD Vance, and Ukrainian President Volodymyr Zelenskiy. The meeting, initially expected to pave the way for a mineral deal between the US and Ukraine—potentially a step toward resolving the Russian invasion—ended in failure. With US-Ukraine relations strained and no clear resolution in sight, uncertainty in the region remains elevated.

On the bright side, markets have scaled up expectations for a Fed rate cut in the first half of the year. However, it’s unclear whether additional monetary easing will truly bolster risk sentiment or simply underscore the extent of the economic challenges ahead. A rate cut could offer short-term relief for risk assets, but it might also underscore fears of an impending downturn in domestic activity.

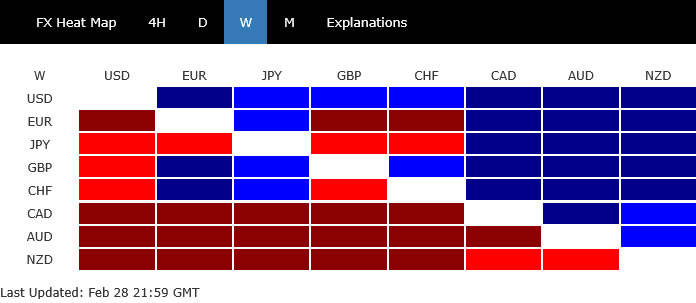

In the forex market, Dollar emerged as the clear winner for the week, benefiting from risk aversion rather than rate expectations. Sterling and Swiss Franc followed as the next strongest currencies, with the UK seemingly avoiding US tariff threats and the Franc gaining from both risk aversion and Euro weakness. At the other end of the spectrum, commodity currencies struggled, with New Zealand Dollar leading the declines, followed by Australian and Canadian Dollars. Meanwhile, Euro ended in a mixed manner, with the initial post-German election boost fading as tariff threats weighed. Yen also struggled to extend its rally, leaving it stuck in the middle of the performance ladder.

Investors Pin Hopes on Fed Easing as Stocks Sell Off, But Is Relief Temporary?

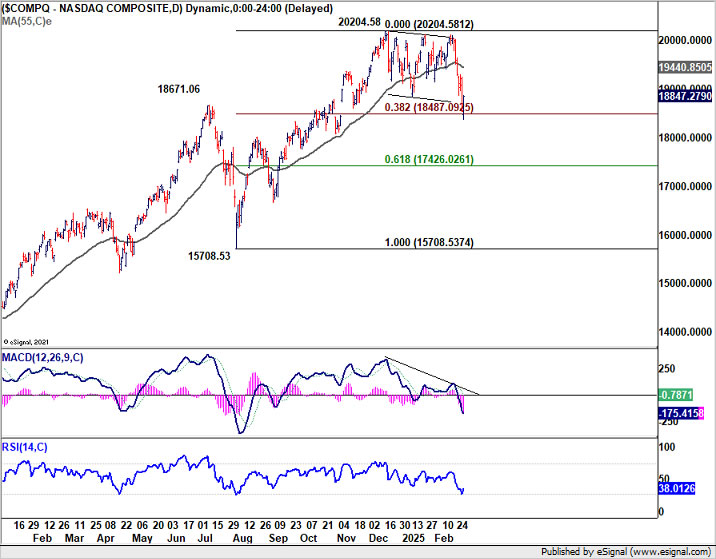

US equity markets ended February on a weak note, with NASDAQ suffering a sharp -3.5% weekly decline despite a late recovery. S&P 500 also lost nearly -1%, while DOW managed to close about 1% higher, benefiting from recovery after leading the selloff earlier in the month. However, the broader market sentiment remained fragile.

For the entire month, NASDAQ dropped -4%, marking its worst monthly performance since April 2024. S&P 500 fell -1.5%, while the DOW ended down -1.6%. Several factors weighed on market sentiment, including intensifying trade war risks, particularly as the scheduled 25% tariffs on Canada and Mexico approach on March 4. The more consequential reciprocal tariffs, set to take effect on April 2, also remain a source of significant uncertainty.

US economic data further exacerbated concerns, with sharp decline in consumer confidence, jump in jobless claims, and contraction in personal spending, all pointing to risk of extended weakness in household demand. These indicators have fueled doubts about the strength of US consumption, which remains a critical driver of economic growth.

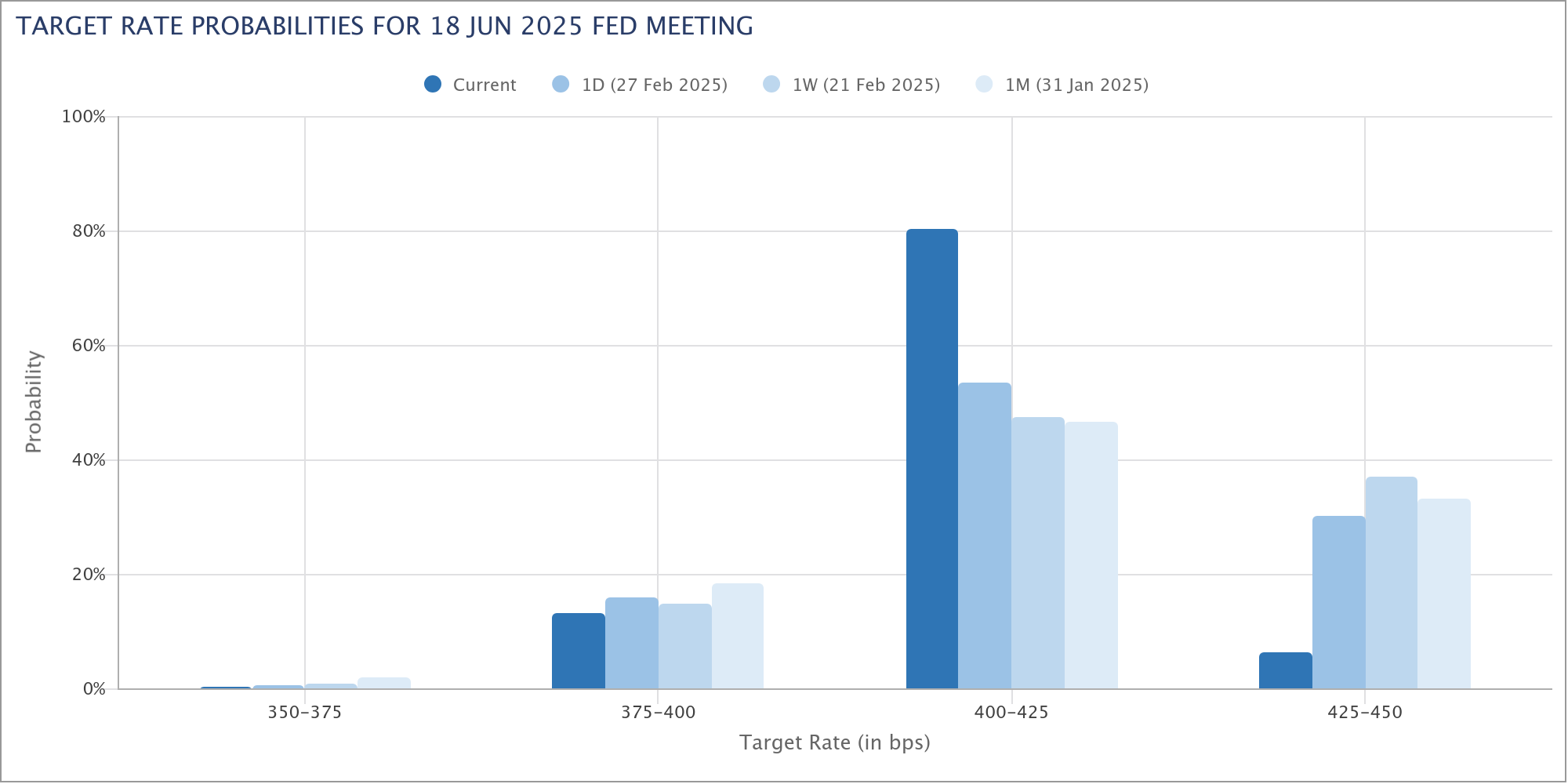

With these headwinds and decline in PCE core inflation as released on Friday, expectations for another Fed rate cut in the first half of the year continued to rise. Fed fund futures now price in a 94% probability of a 25bps cut to 4.00%-4.25% in June, up significantly from 63% just a week ago. This growing optimism about resumed Fed easing has provided some support to market sentiment. But it remains unclear whether it will be enough to reverse the pre-dominating risk-off mood or merely slow the pace of decline.

Technically, NASDAQ is tentatively drawing support from 38.2% retracement of 15708.53 to 20204.58 at 18487.09. Strong rebound from current level, followed by firm break of 55 D EMA (now at 19440.85) will suggest that the corrective pattern from 20204.58 has completed. That will also keep the medium term up trend intact for another rally through 20204.58 at a later stage.

However, sustained break of 18487.09 will raise the chance that a larger scale correction has already started. In the bearish case, NASDAQ should be correcting whole uptrend from 10088.82 (2022 low). Further break of 55 W EMA (now at 17866.91) will confirm this bearish case and pave the way to 38.2% retracement of 10088.82 to 20204.58 at 16340.36.

Risk Aversion Drags Yields Down, But Lifts Dollar Higher

Risk aversion was also evident in the US bond markets, with 10-year Treasury yield tumbling sharply to its lowest level since December. The sharp drop highlights growing concerns over economic uncertainty and trade tensions.

Technically, current development suggests that rise from 3.603 (2024 low) has completed at 4.809 already, well ahead of 4.997 (2023 high). Current fall is seen as another downleg in the sideway corrective pattern from 4.997. Deeper decline is expected to 61.8% retracement of 3.603 to 4.809 at 4.063 next. Risk will stay on the downside as long as 55 D EMA (now at 4.452) holds, in case of recovery.

Dollar Index clear reacted more to risk aversion than falling yields and Fed cut expectations. The’s strong bounce towards the end of the week and the break of 55 D EMA (now at 107.31) suggests that fall from 110.17 has completed at 106.12. That came after defending 38.2% retracement of 100.15 to 110.17 at 106.34. Further rise should be seen to 108.52 resistance. Firm break there will target a retest on 110.17 high.

In the bigger picture, Dollar Index is holding comfortably above 55 W EMA (now at 105.37), and thus rise from 100.15 and 99.57 should still be intact. Break of 110.17 will pave the way back to 114.77 (2022 high) at a later stage.

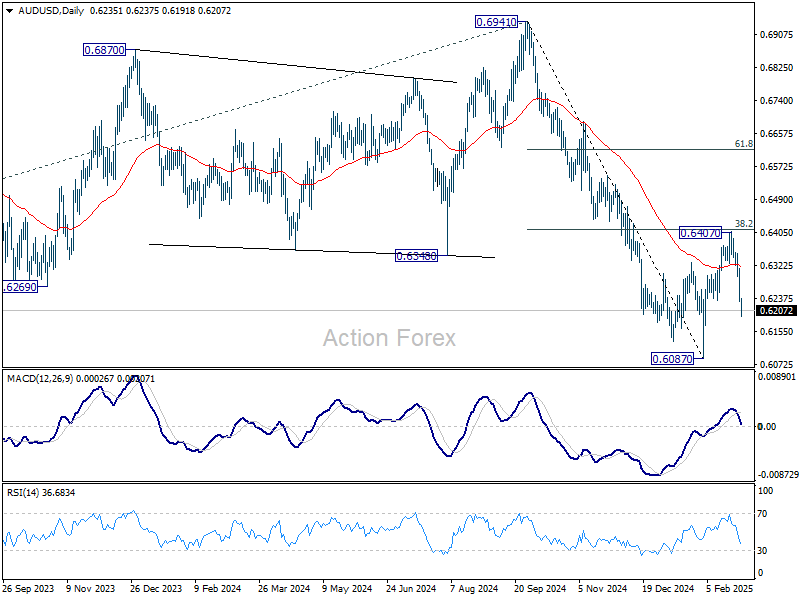

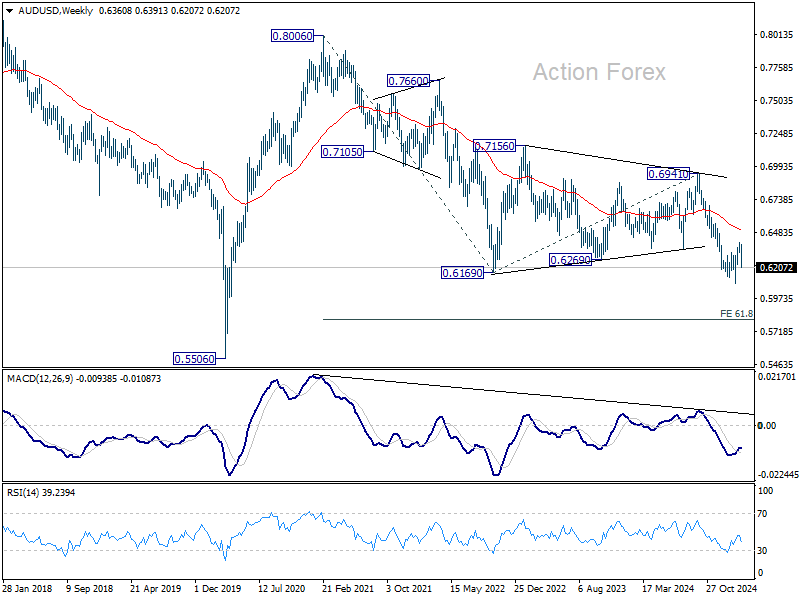

NZD/USD and AUD/USD Sink, Eye 2025 Lows for Support

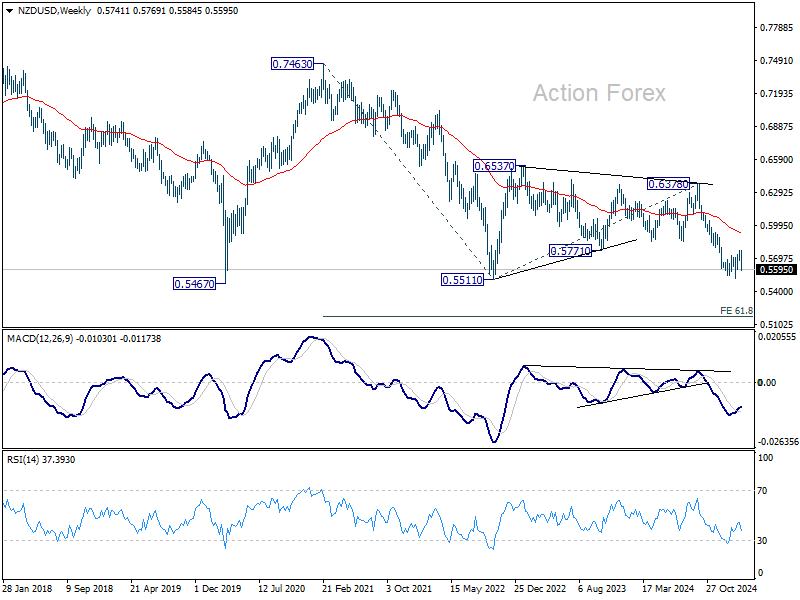

Kiwi and Aussie were the worst-performing currencies last week, each losing around -2.4% against the greenback. With risk sentiment deteriorating downside pressure on these two currencies could persistent. The key focus now is whether risk aversion would intensify and push NZD/USD and AUD/USD through this year’s lows to resume the long term down trend. There these key support levels could offer a breather to them.

Technically, NZD/USD’s steep decline last week suggests that corrective rebound from 0.5515 should have completed at 0.5571 already. Retest of 0.5515 should be seen next. Strong support from there could bring rebound to extend the corrective pattern with another rising leg. But outlook will stay bearish as long as 38.2% retracement of 0.6378 to 0.5515 at 0.5848 holds. Firm break of 0.5515 will resume the long term down trend to 61.8% projection of 0.7463 to 0.5511 from 0.6378 at 0.5172.

Similarly, AUD/USD’s corrective rebound from 0.6087 should have completed at 0.6407. Retest of 0.6087 low should be seen next. Strong rebound from there would extend the corrective pattern with another rising leg. But outlook will stay bearish as long as 38.2% retracement of 0.6941 to 0.6087 at 0.6413 holds. Firm break of 0.6087 will resume the long term down trend to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806.

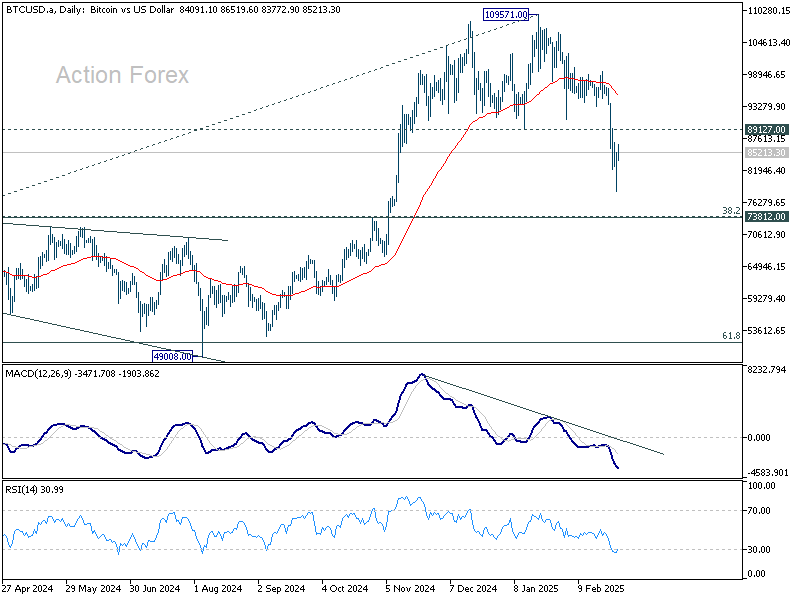

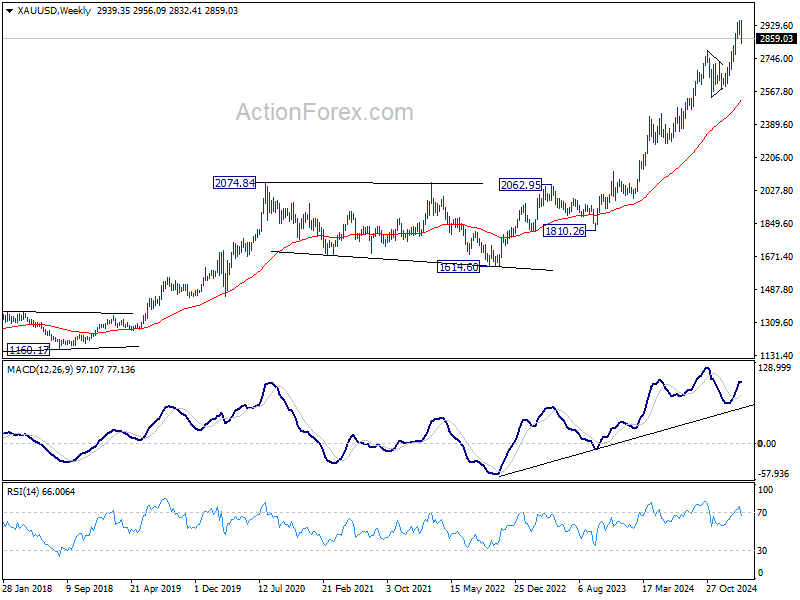

Bitcoin and Gold Tumble on Risk-Off Sentiment

Bitcoin and Gold struggled under renewed risk aversion last week, extending their losses in line with broader market weakness. While Gold retains a comparatively better outlook, both assets remain vulnerable to ongoing volatility.

Bitcoin suffered a sharp fall, decisively breaking 89127 support, confirming medium-term topping at 109571. The current slide is seen as a correction of the entire uptrend from the 15452 (2022 low). Deeper decline toward 55 W EMA (now at 74129) is expected.

Strong support could emerge from the 73812 cluster zone (38.2% retracement of 15452 to 109571 at 73617) to bring rebound, at least first attempt. However, downside risks remain as long as 55 D EMA (now at 95288) caps any recovery.

Decisive break of 73617/73812 zone could extended the decline to 50k mark, which is close to 49008 support and 61.8% retracement at 51405.

By contrast, Gold’s outlook is less overtly bearish. 2956.09 is seen as a short term top only, for now. Subsequent pullback is viewed primarily as a correction of the rise from 2584.24. Strong support might be seen from 55 D EMA (now at 2792.05) to bring rebound, and set the base for uptrend resumption at a later stage.

However, considering that Gold was just rejected by 3000 psychological level sustained trading below 55 D EMA would argue that larger scale correction in underway. In the bearish case, Gold could be starting a medium term decline back to 55 W EMA (now at 2522.33).

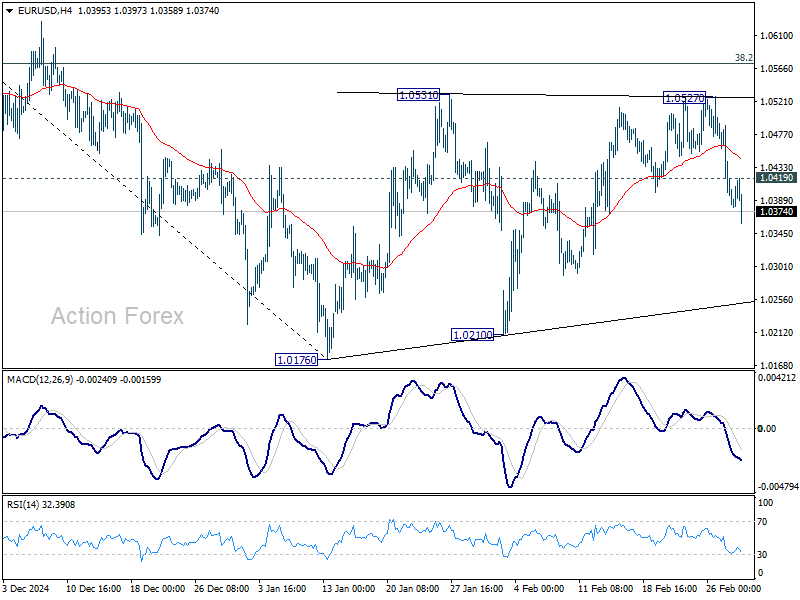

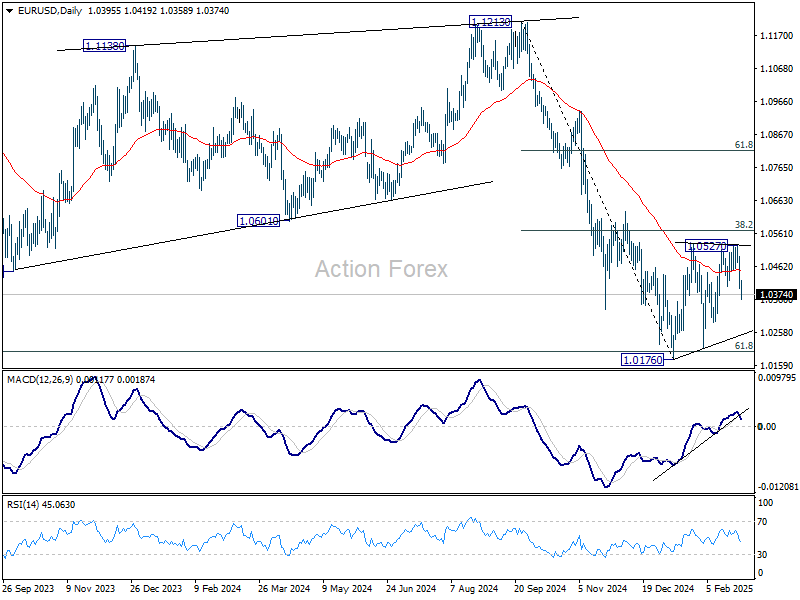

EUR/USD reversed after edging higher to 1.0527 last week, and the development suggests that consolidation from from 1.0176 has already completed. Initial bias stays on the downside this week for retesting 1.0176/0210 support zone first. Firm break there will resume whole fall from 1.1213, and carry larger bearish implications. On the upside, above 1.0419 minor resistance will turn intraday bias neutral. But outlook will stay bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

In the long term picture, down trend from 1.6039 remains in force with EUR/USD staying well inside falling channel, and upside of rebound capped by 55 M EMA (now at 1.0929). Consolidation from 0.9534 could extend further and another rising leg might be seem. But as long as 1.1274 resistance holds, eventual downside breakout would be mildly in favor.

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more