Euro Under Pressure Ahead Of PMIs From EZ, UK And US

Euro faces headwinds this week, emerging as one of the more subdued performers, with all eyes set on today’s Eurozone PMI data. Its trajectory, when compared to Yen and Aussie, remains uncertain, as both showed minimal response to their respective PMI releases. Conversely, Dollar’s movement, in anticipation of the PMI release, is expected to be constrained, with the market’s primary focus shifting to Fed Chair Jerome Powell’s upcoming speech at the Jackson Hole Symposium. Meanwhile, Canadian Dollar might witness some stirring due to release of its retail sales data.

For the ongoing week, Yen sits at the bottom of the performance chart, trailed by Euro and then Dollar. Conversely, Australian Dollar is leading the pack, with the New Zealand Dollar and Swiss Franc closely following. Both Sterling and Canadian Dollar hold neutral positions. Remarkably, except for EUR/GBP, majority of major pairs and crosses are treading within the previous week’s range.

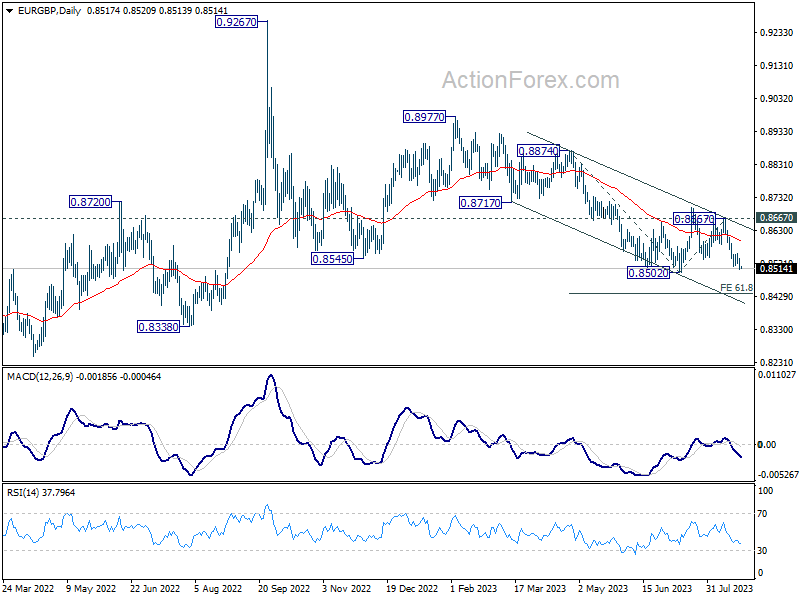

Zooming in on EUR/GBP, release of UK PMIs is anticipated to induce some movement. Immediate focus is now on 0.8502 support in the cross. Decisive break there will resume larger decline from 0.8977. Next target is 61.8% projection of 0.8874 to 0.8502 from 0.8667 at 0.8437. Downside breakout in EUR/GBP, especially with a simultaneous break of 0.9520 support in EUR/CHF, might intensify Euro’s descent across the board.

In Asia, at the time of writing, Nikkei is up 0.34%. Hong Kong HSI is up 0.91%. China Shanghai SSE is down -0.62%. Singapore Strait Times is up 0.36%. Japan 10-year JGB yield is up 0.007 at 0.679. Overnight, DOW dropped -0.51%. S&P 500 dropped -0.28%. NASDAQ rose 0.06%. 10-year yield dropped -0.014 to 4.328.

Japan PMI manufacturing ticked up to 49.7, services rose to 54.3

In August, Japan’s Service PMI climbed from 53.8 to 54.3, while the Manufacturing PMI saw a slight increase from 49.6 to 49.7, just above anticipated figures. The Composite PMI also edged up from 52.2 to 52.6.

Andrew Harker, from S&P Global Market Intelligence, pointed out the robust performance of the service sector, driven by consistent new order growth. In contrast, manufacturing only marginally rebounded but remained below the growth threshold.

Despite the overall rise in new orders, manufacturing employment remained flat, ending its 28-month growth streak. Additionally, heightened oil prices impacted both sectors, causing the steepest rise in input costs in four months. Notably, business confidence dwindled in both domains due to longer-term economic uncertainties.

Australian PMI hits 19-month low, but concerns on inflation and strong employment rise

Australia’s August PMI data showed a concerning decline across sectors. The Manufacturing PMI slightly decreased from 49.6 to 49.4, while Services PMI dropped to a 19-month low of 46.7. Composite PMI, reflecting both sectors, also declined to a 19-month low of 47.1.

Warren Hogan, Chief Economic Advisor at Judo Bank, drew attention to the employment sector’s resilience. He noted, “Despite weakening PMI figures, the employment index remains positive, indicating robust labour demand across both manufacturing and services.”

With businesses maintaining optimism, they might resist workforce reductions even amidst economic slowdowns. “As aggregate demand is supported by ongoing employment growth… it might mean a further substantial lift in interest rates could be required at some stage in the next 6-12 months,” he added.

Inflation remains a key concern. After 2022 disinflation trend, 2023 has shown a halt in the falling price indexes. The current data suggests an inflation rate of about 4%, overshooting the RBA’s 2-3% target range.

Hogan also noted wage growth concerns. Even with modest official growth figures, he cautioned that wage pressures might exceed RBA’s forecasted 4% annual growth for 2023. “This may mean firm tightening bias to the RBA’s policy deliberations for the rest of the year.”

NZ retail sales volume down -1.0% qoq in Q2, value down -0.2% qoq

New Zealand’s retail sales volume for Q2 plummeted by -1.0% qoq, settling at NZD 25B. This decline starkly contrasts with market forecasts which had anticipated a milder contraction of just -0.2% qoq. A broad-based slump was evident, as 11 out of 15 industries reported reduced seasonally adjusted sales volumes.

Highlighting the sectors that bore the brunt of this downturn, food and beverage services saw a sharp decline of -4.4%. Hardware, building, and garden supplies trailed closely, recording a -4.8% drop. These sectors emerged as the primary drags on the overall sales volume for the quarter.

While sales volume took a hit, retail sales value also showed signs of weakness, contracting -0.2% qoq to land at NZD 30B. Once again showcasing the breadth of the downturn, seven out of 15 industries registered a fall.

Looking ahead

Eurozone and UK PMIs will be the main focus in European session. Later in the day, Canada will release retail sales. US will release PMIs and new home sales.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0809; (P) 1.0870; (R1) 1.0907; More…

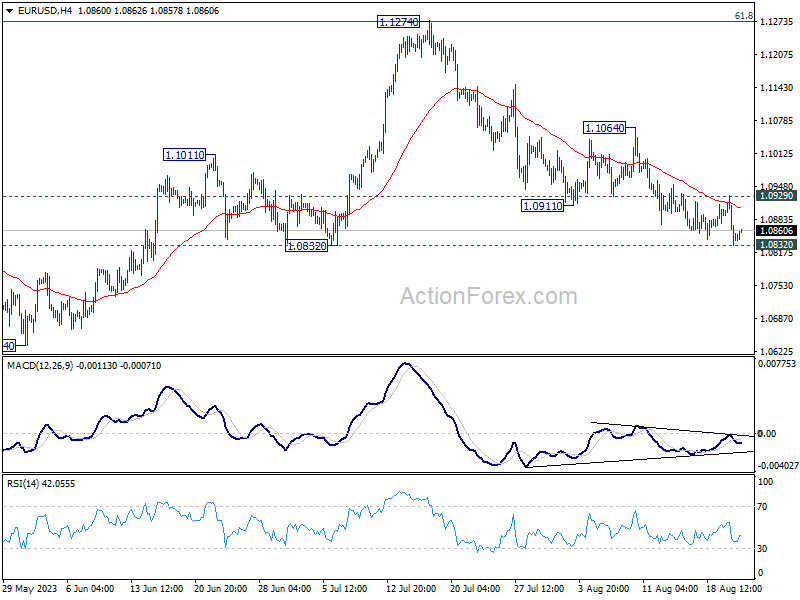

Immediate focus is now on 1.0832 support in EUR/USD. Firm break there will resume whole fall from 1.1274, and target target 1.0609/34 cluster support next. On the upside, however, break of 1.0929 resistance will turn intraday bias to the upside for stronger recovery.

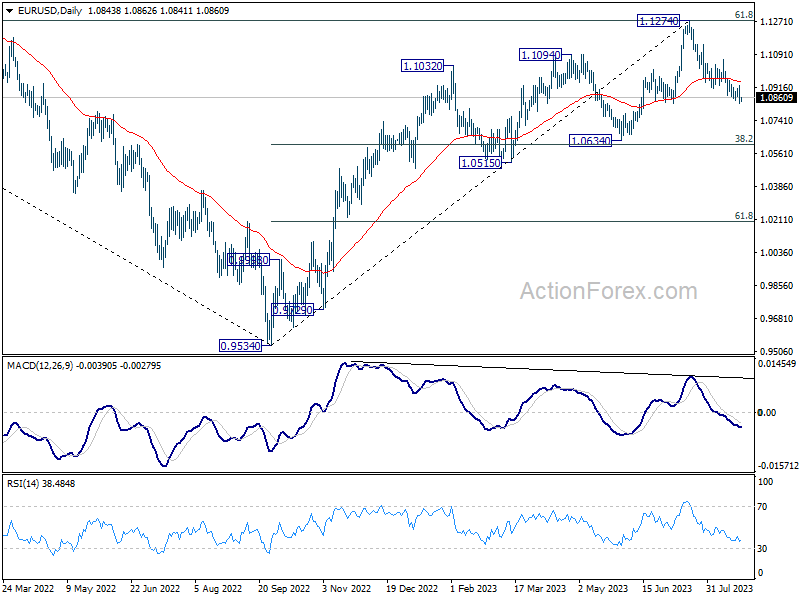

In the bigger picture, a medium term top should be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Fall from there is seen as a correction to the uptrend from 0.9534 (2022 low). Deeper decline would be seen to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation. Yet, medium term outlook will be neutral for now, as long as 1.1274 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Retail Sales Q/Q Q2 | -1.00% | -0.20% | -1.40% | -1.60% |

| 22:45 | NZD | Retail Sales ex Autos Q/Q Q2 | -1.80% | -0.10% | -1.10% | -1.60% |

| 23:00 | AUD | Manufacturing PMI Aug P | 49.4 | 49.6 | ||

| 23:00 | AUD | Services PMI Aug P | 46.7 | 47.9 | ||

| 00:30 | JPY | Manufacturing PMI Aug P | 49.7 | 49.6 | 49.6 | |

| 07:15 | EUR | France Manufacturing PMI Aug P | 45.2 | 45.1 | ||

| 07:15 | EUR | France Services PMI Aug P | 47.3 | 47.1 | ||

| 07:30 | EUR | Germany Manufacturing PMI Aug P | 38.7 | 38.8 | ||

| 07:30 | EUR | Germany Services PMI Aug P | 51.5 | 52.3 | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Aug P | 42.8 | 42.7 | ||

| 08:00 | EUR | Eurozone Services PMI Aug P | 50.5 | 50.9 | ||

| 08:30 | GBP | Manufacturing PMI Aug P | 45.1 | 45.3 | ||

| 08:30 | GBP | Services PMI Aug P | 50.8 | 51.5 | ||

| 12:30 | CAD | Retail Sales M/M Jun | 0.00% | 0.20% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M Jun | 0.30% | 0.00% | ||

| 13:45 | USD | Manufacturing PMI Aug P | 48.9 | 49 | ||

| 13:45 | USD | Services PMI Aug P | 52.4 | 52.3 | ||

| 14:00 | USD | New Home Sales Jul | 708K | 697K | ||

| 14:00 | EUR | Eurozone Consumer Confidence Aug P | -14 | -15 | ||

| 14:30 | USD | Crude Oil Inventories | -2.9M | -6.0M |

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more