Euro Shrugs Confidence Data, Quiet Markets With Eyes On Yen

Today’s financial markets exhibited subdued activity, with few standout movements. Notably, even as Eurozone’s investor confidence data outperformed expectations, Euro lagged, moving in tandem with Swiss Franc. On the other hand, Sterling is trading mildly higher, echoing the rise of commodity currencies, while Dollar is steady, devoid of fresh buying enthusiasm.

The spotlight shifts to Yen in the upcoming Asian session, as data on labor cash earnings and household spending take center stage. BoJ has consistently underscored the centrality of wage growth in securing a sustainable inflation target. Recent updates on wage negotiations appear promising. Strong data sets could further bolster BoJ’s inclination to reconsider its ultra-accommodative monetary stance.

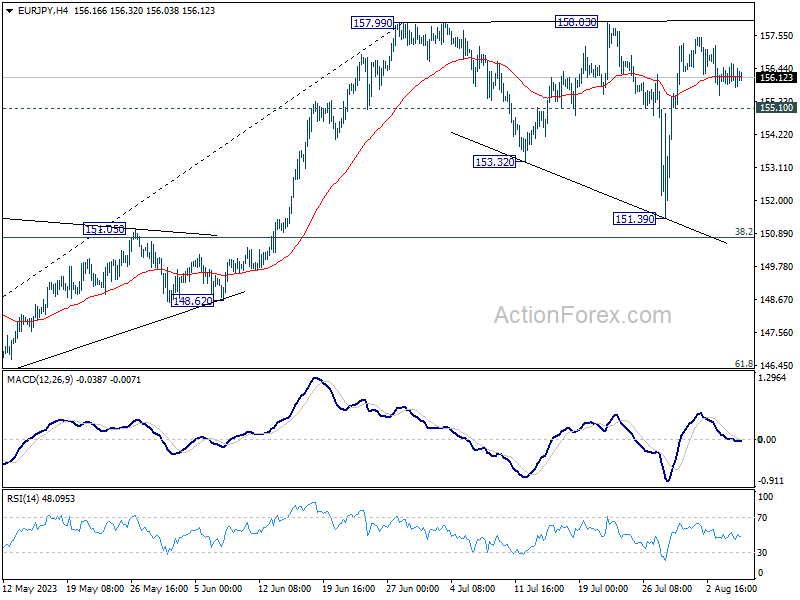

Despite railing to break through 157.99/158.03 resistance on first attempt, EUR/JPY has been relatively resilient. As long as 155.10 minor support holds, another take on the resistance is expected in the near term. Decisive break will confirm larger up trend resumption. However, break of 155.10 will align to outlook with other Yen crosses, and argue that the corrective pattern from 157.99 is extending with another downleg. Deeper fall could then be seen back towards 151.39 support.

In Europe, at the time of writing, FTSE is down -0.49%. DAX is down -0.34%. CAC is down -0.10%. Germany 10-year yield is up 0.0219 at 2.591. Earlier in Asia, Nikkei rose 0.19%. Hong Kong HSI dropped -0.01%. China Shanghai SSE dropped -0.59%. Singapore Strait Times rose 0.53%. Japan 10-year JGB yield dropped -0.018 to 0.628.

Fed Williams: It’s an open question on additional rate hikes

In a candid interview with the New York Times, New York Fed President John Williams deemed the present monetary policy as being “in a good place”. It’s an “open question” on whether Fed needs additional rate hikes.

He emphasized the need to “watch the data”. “Are we seeing the supply-demand imbalances continue to shrink, move in the right direction? Are we seeing the inflation data move in the right direction?”

He anticipates that the need for a restrictive monetary stance will persist for a while. He contemplates, “I think we’re pretty close to what a peak rate would be, and the question will really be — once we have a good understanding of that, how long will we need to keep policy in a restrictive stance, and what does that mean.”

Also, highlighting his approach towards monetary policy, Williams thought of monetary policy primarily in terms of “real interest rates”, rather than “nominal rates” set by Fed. He stressed the potential consequences if inflation rates declined as projected by numerous forecasts: “if we don’t cut interest rates at some point next year then real interest rates will go up, and up, and up. And that won’t be consistent with our goals.” Hence, “to keep maintaining a restrictive stance may very well involved cutting the federal funds rate next year, or year after”.

Eurozone Sentix rose to -18.9, but no joy about this development

Eurozone Sentix Investor Confidence rose from -22.5 to -18.9 in August, much better than expectation of -25.0. Current Situation Index was unchanged at -20.5. Expectations Index rose from -24.5 to -17.3. Inflation theme barometer rose to -11, indicating a decline in inflationary pressure. Central bank policy barometer also rose to -13.

Nevertheless, Sentix noted, “Investors are thus by no means positive about economic developments, the expected rate of deterioration is merely easing. Thus, at the beginning of August 2023, the economy in the euro zone remains in recession mode. There can therefore be no joy about this development.”

In Germany, Sentix Investor Confidence fell from -28.4 to -30.4, lowest since October 2022. Current Situation Index dropped from -28.0 to -35.3. worst since July 2020. Expectations index rose slightly from -28.8 to -26.0.

BoJ opinions: Flexible YCC needed while maintaining monetary easing

In the Summary of Opinions at the July 27-28 meeting, BoJ reinforced its commitment to monetary easing but highlighted a pressing need for more “flexibility” in its yield curve control approach policy.

The bank’s primary stance was evident among board members: Achieving a 2% price stability target “has not yet come in sight”, necessitating continued monetary easing and the preservation of the current YCC framework.

“There is still a significantly long way to go before revising the negative interest rate policy, and the framework of yield curve control needs to be maintained,” one member noted.

However, there will be potential market disruptions by strictly capping 10-year JGB yields at 0.5%, another opinion noted.

Also, given the “increasingly significant upside and downside risks” to prices outlook, flexible YCC is needed for allowing market-driven interest rates, ensuring liquidity, and preventing abrupt rate shifts.

The bank also remarked on the current inflation trends, suggesting they primarily stem from import inflation. A rise in earning power, especially for small and medium-sized firms, was emphasized as crucial before instituting broader YCC flexibility.

At the meeting, BoJ permitted a rise in the 10-year yield beyond its usual 0.5% limit, reaching up to 1%.

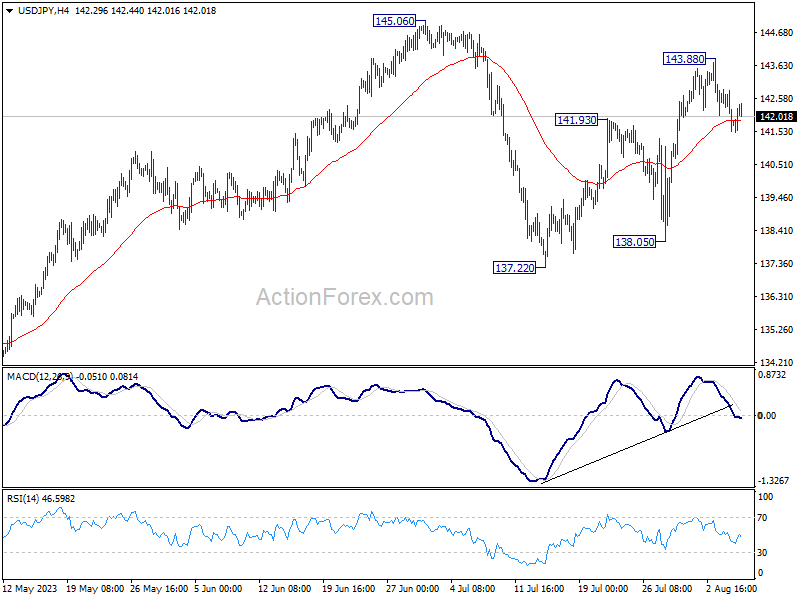

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 141.26; (P) 142.07; (R1) 142.59; More…

Intraday bias in USD/JPY stays mildly on the downside for the moment. Fall from 143.88 could be the third leg of the pattern from 145.06. Deeper fall would be seen to 55 D EMA (now at 140.50). On the upside, though, above 143.88 will resume the rise from 137.22 to retest 145.06 resistance instead.

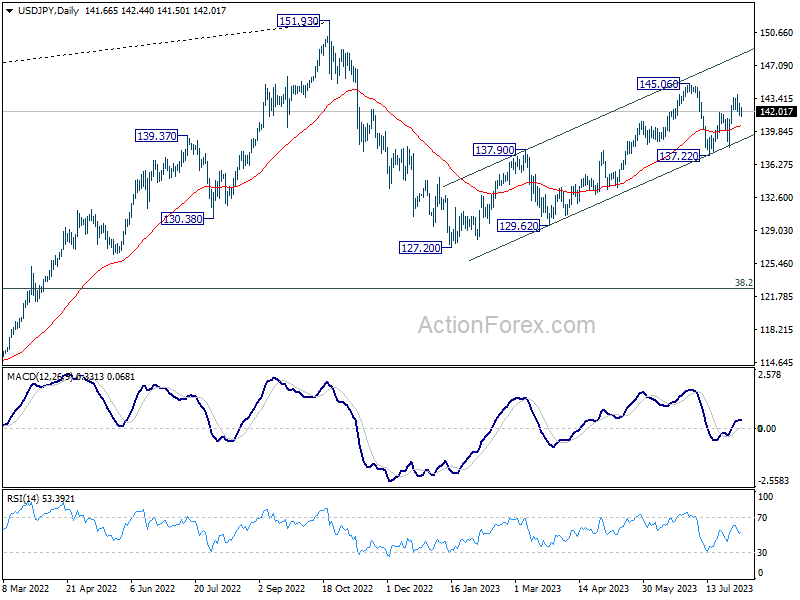

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Summary of Opinions | ||||

| 05:00 | JPY | Leading Economic Index Jun P | 108.9 | 108.9 | 109.2 | |

| 06:00 | EUR | Germany Industrial Production M/M Jun | -1.50% | -0.40% | -0.20% | -0.10% |

| 07:00 | CHF | Foreign Currency Reserves (CHF) Jul | 698B | 725B | ||

| 08:30 | EUR | Eurozone Sentix Investor Confidence Aug | -18.9 | -25 | -22.5 |

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more