Dollar Rally Continues On Risk-Off Sentiment And Rising Yields; Markets Eye BoE Rate Decision

Dollar continues to strengthen today, bolstered by prevailing risk-off sentiment that has carried over from US to Asian markets. The surge in benchmark 10-year yields is providing additional support to the greenback, as even Euro has finally conceded a near-term support level against Dollar, further affirming the underlying momentum.

Meanwhile, the foreign exchange markets elsewhere are mixed inside yesterday’s range. Sterling remains relatively indecisive as investors keenly await BoE rate decision. Elements of surprise, including the size of the interest rate hike, voting dynamics, and new economic projections, contribute to the uncertainty. Reactions in Sterling-European crosses will be pivotal, as these could dictate the momentum of the Pound elsewhere.

For this week so far, Dollar is outperforming, followed by Canadian, and then Euro. Conversely, Australian dollar is underperforming, trailed by Yen and New Zealand Dollar.

Technically, it’s likely that S&P 500 has made a short term top at 4607.07, considering mild bearish divergence condition in D MACD. Risk will now stay on the downside as long as yesterday’s high at 4550.93 holds. Deeper fall is in favor towards 55 D EMA (now at 4395.347) as a correction to the larger rally from 3491.58. The down move could be solidified, if 10-year yield could break away from 4.091 resistance decisively. But after all, the next moves will be subject to market reactions to today’s ISM services and tomorrow’s NFP.

In Asia, at the time of writing, Nikkei is down -1.31%. Hong Kong HSI is up 0.11%. China Shanghai SSE is up 0.15%. Singapore Strait Times is down -0.06%. Japan 10-year JGB is up 0.0180 at 0.646. Overnight, DOW dropped -0.98%. S&P 500 dropped -1.38%. NASDAQ dropped -2.17%. 10-year yield hit as high as 4.126 then closed up 0.027 at 4.078.

BoE to hike for sure, but by 25bps or 50bps?

BoE is widely expected to continue tightening today, though the extent of interest rate hike remains a point of contention. Markets currently slightly favor a 25 bps increment to 5.25%. However, a more aggressive 50bps hike to 5.50% cannot be entirely dismissed. The Bank’s unexpected 50bps raise in June took markets by surprise, leading some economists to posit a strategic shift in the institution’s response strategy. Conversely, CPI for June, which slowed more-than-expected to 7.9%, was perceived as a positive development by BoE policymakers, and could argue for a return to slowing tightening.

Regardless of today’s decision, it is widely understood that this will not conclude the ongoing tightening cycle. Compared to ECB and Fed, BoE is anticipated to continue tightening for an extended period. Nonetheless, expectation of terminal rate has been fluctuating widely recently though, swinging from as high as 6.5% to 5.75% in a matter of weeks, suggesting a persisting uncertainty about the path ahead.

In addition to the anticipated rate decision, market observers will be closely watching two key aspects. First, today’s voting could provide insight into the approach of MPC’s newest member, Megan Greene, who recently succeeded known dove Silvana Tenreyro. If Greene presents a less dovish stance, Swati Dhingra may stand out as the only dissenter, making the vote an 8-1 majority.

Secondly, BoE is also set to release its new economic forecasts. Governor Andrew Bailey has repeatedly suggested that inflation is expected to decline fairly swiftly in the second half of the year, prompting keen interest in whether this prediction will still be reflected in the forthcoming projections.

Here are some readings on BoE:

- Will BoE Go Back to 25bps Interest Rate Increments?

- Bank of England Preview – Topside Risk to EUR/GBP With a Return to 25bp Steps

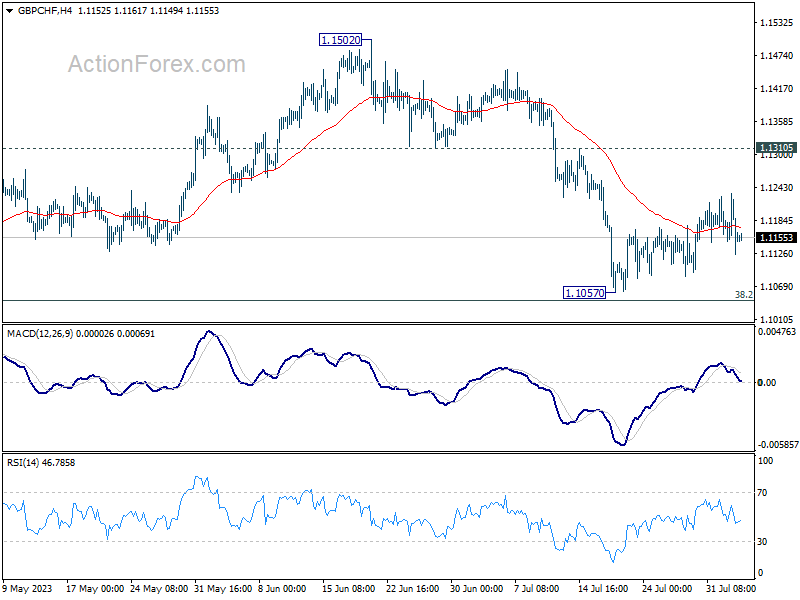

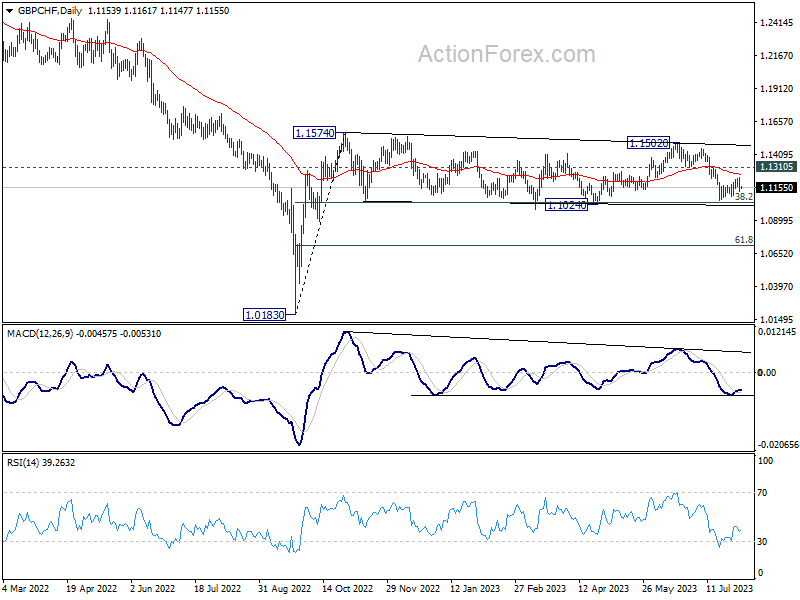

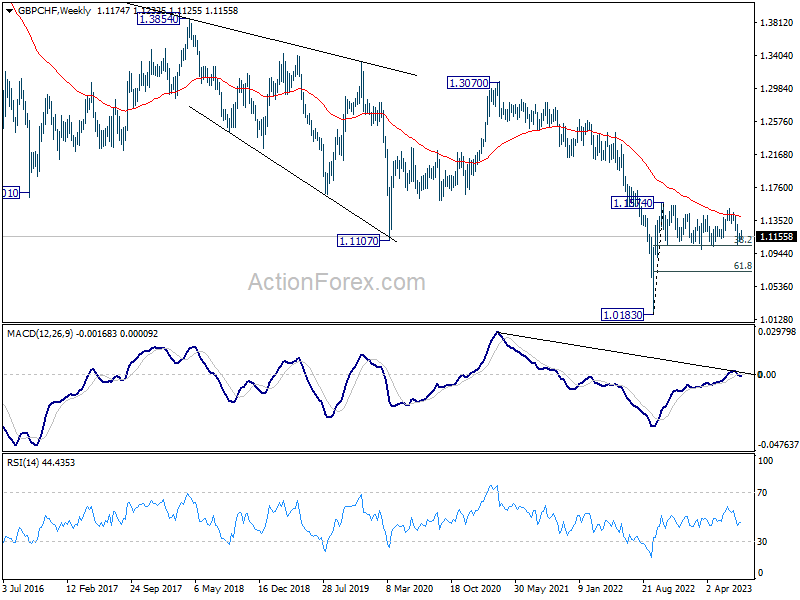

GBP/CHF’s technical picture is mixed for now, with some dovish favor. From the near term angle, recovery from 1.1057 is clearly corrective looking, favoring a downside breakout. But the pair has been trading in medium term range of 1.1024/1574 since last October, keeping it neutral-at-worst. Yet, prior rejection by 55 W EMA is keeping the long term outlook bearish to neutral-at-best.

Still, further fall is more likely than not as long as 1.3105 support turned resistance zone. Decisive break of 1.1024 will bring deeper decline to 38.2% 1.0183 to 1.1574 at 1.0714 in rather quick manner. Let’s see how GBP/CHF would reaction to today’s BoE announcement.

China’s Caixin PMI composite fell to 51.9, lowest since Jan

China’s Caixin PMI Services increased slightly from 53.9 to 54.1 in July, surpassing the anticipated figure of 52.5. However, this reading fell short of the 55.5 average seen over the previous six months. Concurrently, PMI Composite dropped from 52.5 to 51.9, its lowest mark since January.

Commenting on the latest figures, Wang Zhe, a Senior Economist at Caixin Insight Group, expressed that the uneven recovery of the service and manufacturing industries remains a prominent concern. He noted, “Although the manufacturing sector was a drag, the steady expansion of the services industry still helped overall output, demand, and employment remain in positive territory.”

The contraction in exports appeared pronounced, and while input costs saw a slight uptick, output prices registered a minor drop. Despite these challenges, expectations for future output remained on the optimistic side, though this metric recorded a new low since November.

On the broader economic landscape, Wang Zhe noted, “Although the data for industrial production and investment in June showed some signs of recovery, macroeconomic growth remained sluggish, and considerable downward pressure on the economy persisted.”

Turning to policy recommendations, he emphasized the need for employment guarantees, stabilization of expectations, and boosting household income. He further argued that “At present, monetary policy only has a limited effect on boosting supply. An expansionary fiscal policy that targets demand should be prioritized.”

On the data front

Swiss CPI will be a main feature in European session. Eurozone will release PMI services final and PPI. UK will also release PMI services final.

Later in the day, US jobless claims, non-farm productivity, ISM services and factory orders will be published.

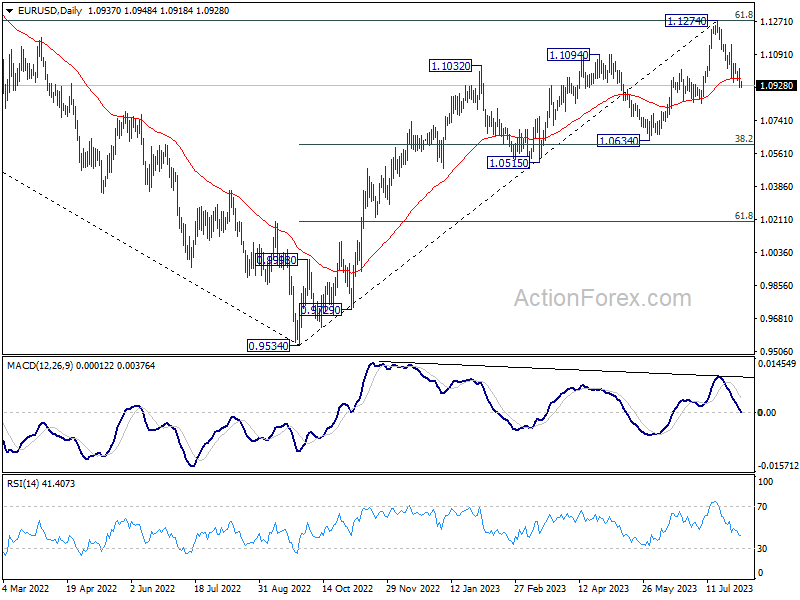

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0897; (P) 1.0959; (R1) 1.0999; More…

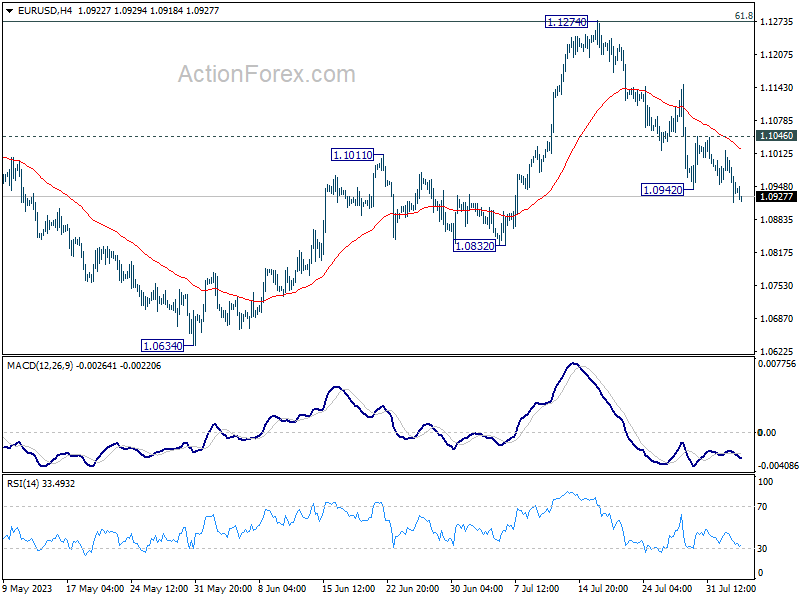

EUR/USD’s decline from 1.1274 resumed by breaking through 1.0942 and intraday bias is back on the downside. Deeper fall would be seen to 1.0832 support. Sustained trading below there will target 1.0609/34 cluster support. On the upside, however, break of 1.1046 resistance will turn bias back to the upside for stronger rebound instead.

In the bigger picture, a medium term top could be formed at 1.1274, after failing to break through 61.8% retracement of 1.2348 (2021 high) to 0.9534 at 1.1273 decisively, on bearish divergence condition in D MACD. Sustained trading below 55 D EMA (now at 1.0963) will bring deeper correction to 1.0634 cluster support (38.2% retracement of 0.9534 to 1.1274 at 1.0609). Strong support could be seen there, at least on first attempt, to set the range for consolidation.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Trade Balance (AUD) Jun | 11.32B | 10.50B | 11.79B | |

| 01:45 | CNY | Caixin Services PMI Jul | 54.1 | 52.5 | 53.9 | |

| 06:00 | EUR | Germany Trade Balance (EUR) Jun | 15.5B | 14.4B | ||

| 06:30 | CHF | CPI M/M Jul | -0.10% | 0.10% | ||

| 06:30 | CHF | CPI Y/Y Jul | 1.50% | 1.70% | ||

| 07:45 | EUR | Italy Services PMI Jul | 52.3 | 52.2 | ||

| 07:50 | EUR | France Services PMI Jul F | 47.4 | 47.4 | ||

| 07:55 | EUR | Germany Services PMI Jul F | 52 | 52 | ||

| 08:00 | EUR | Italy Retail Sales M/M Jun | 0.00% | 0.70% | ||

| 08:00 | EUR | Eurozone Services PMI Jul F | 51.1 | 51.1 | ||

| 08:30 | GBP | Services PMI Jul F | 51.5 | 51.5 | ||

| 09:00 | EUR | Eurozone PPI M/M Jun | -0.20% | -1.90% | ||

| 09:00 | EUR | Eurozone PPI Y/Y Jun | -1.50% | |||

| 11:00 | GBP | BoE Interest Rate Decision | 5.25% | 5.00% | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | 7–0–2 | 7–0–2 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Jul | 25.20% | |||

| 12:30 | USD | Initial Jobless Claims (Jul 28) | 223K | 221K | ||

| 12:30 | USD | Nonfarm Productivity Q2 P | 1.10% | -2.10% | ||

| 12:30 | USD | Unit Labor Costs Q2 P | 2.70% | 4.20% | ||

| 13:45 | USD | Services PMI Jul F | 52.4 | 52.4 | ||

| 14:00 | USD | ISM Services PMI Jul | 53 | 53.9 | ||

| 14:00 | USD | Factory Orders M/M Jun | 0.20% | 0.30% | ||

| 14:30 | USD | Natural Gas Storage | 18B | 16B |

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more