Dollar Gears Up As Eyes Turn To FOMC Minutes; Sterling Staying Firm

In early US trading sessions, Dollar is showing signs of regaining momentum as market participants eagerly anticipate the release of FOMC minutes from July 25-26 meeting, where a 25bps hike was delivered. Recent comments from Fed officials suggest an increasing divergence in views regarding the need for additional monetary tightening.

Presently, fed funds futures reflect an approximately 90% likelihood of rates remaining unchanged in September, with the odds for another rate hike by year-end staying well below 40%. Although the minutes might not paint a clear roadmap for future rate adjustments, the deliberations between the more aggressive ‘hawks’ and the cautious ‘doves’ are set to garner significant attention.

In the broader currency landscape, Sterling has emerged as today’s frontrunner, buoyed by UK’s CPI data. However, its climb lacks substantial vigor. Hot on its heels is New Zealand Dollar, followed by Euro. Swiss Franc, meanwhile, finds itself at the opposite end of the spectrum as today’s weakest performer, shadowed closely by the Australian Dollar and the Yen.

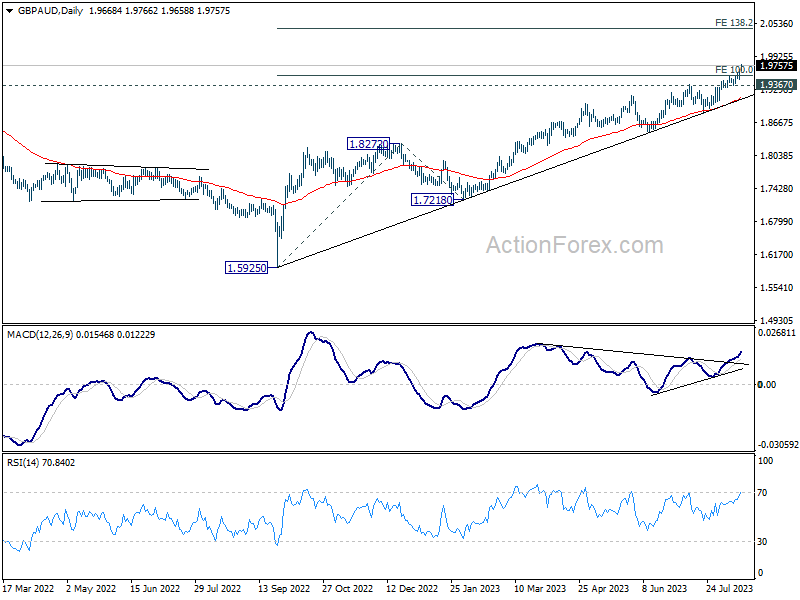

Technically, GBP/AUD up trend continues this week, and D MACD clearly indicates upside reacceleration. Further rise is expected as long as 1.9367 support holds. With 100% projection of 1.5925 to 1.8272 from 1.7218 at 1.9565 taken out, next target is 138.2% projection at 2.0462. While both currencies are risk-sensitive, the development in GBP/AUD suggests that Aussie is the one to go against in case of intensifying risk aversion, not the Pound.

In Europe, at the time of writing, FTSE is down -0.59%. DAX is up 0.02%. CAC is down -0.11%. Germany 10-year yield is down -0.006 at 2.670. Earlier in Asia, Nikkei dropped -1.46%. Hong Kong HSI dropped -1.36%. China Shanghai SSE dropped -0.82%. Singapore Strait Times dropped -0.59%. Japan 10-year JGB yield rose 0.0002 to 0.632.

Eurozone industrial production up 0.5% mom on energy

Eurozone industrial production rose 0.5% mom in June, well above expectation of 0.1% mom. Production of energy grew by 0.5%, while production of durable consumer goods fell by -0.1%, capital goods by -0.7%, intermediate goods by -0.9% and non-durable consumer goods by -1.1%.

EU industrial production rose 0.4% mom. Among Member States for which data are available, the highest monthly increases were registered in Ireland (+13.1%), Denmark (+6.3%) and Lithuania (+3.2%). The largest decreases were observed in Sweden (-5.3%), Finland and Malta (both -3.3%) and Belgium (-3.0%).

UK CPI slowed to 6.8% in Jul, services inflation hit highest since 1992

July saw a marked deceleration in UK’s CPI, falling from 7.9% yoy to 6.8% yoy , precisely in line with market expectations. Core CPI, which strips out variables like energy, food, alcohol, and tobacco, stood unchanged at 6.9% yoy, above the expected 6.8%.

CPI figures pertaining to goods showed a noticeable slowdown, dropping from 8.5% yoy to 6.1% yoy. On the flip side, CPI services ramped up from 7.2% yoy to 7.4% yoy , registering its peak since the staggering 9.5% yoy rate observed in March 1992.

On a month-to-month analysis for July, CPI receded by -0.4%, a figure slightly above than forecasted decline of -0.5%. Core CPI saw a monthly rise of 0.3% mom. While the CPI for goods plunged by -1.7% mom. , services CPI exhibited an increase, registering growth of 1.0% mom. .

Office for National Statistics remarked, “The slowdown in the annual CPI rate into July 2023 was driven by downward contributions to change from 8 of the 12 divisions.”

Notably, housing and household services emerged as the primary sectors applying downward pressure. Expanding on this, ONS stated, “Within this division, the downward effect came mainly from gas and electricity.”

RBNZ on hold, OCR to stay high for longer

RBNZ has decided to maintain OCR unchanged at 5.50% again, aligning with broad market expectations. Making its stance clear, the bank asserted that the “OCR needs to stay at restrictive levels for the foreseeable future.”

Reflecting a neutral stance, the central bank emphasized its confidence in the current monetary policy, “that with interest rates remaining at a restrictive level for some time, consumer price inflation will return to within its target range of 1 to 3% per annum, while supporting maximum sustainable employment.”

Adding depth to its economic perspective, “The nominal neutral OCR has increased by 25 basis points to 2.25% within the projections,” the Committee noted. They were in consensus that the existing OCR level was contractionary, asserting that it’s effectively curbing domestic spending as intended.

Shifting the lens to future projections, the forecasts in the Monetary Policy Statement hint at the OCR potentially reaching a peak of 5.6% in the first quarter of 2024. This marks a slight shift from the earlier prediction of 5.5% in Q3 2023, hinting at the possibility of an additional rate hike. As for subsequent rate cut expectations are now set for the second quarter of 2025, a slight delay from the previously anticipated period between Q4 2024 and Q1 2025.

Australia’s Westpac leading index ticks up, but below-par growth set to persist

Australia’s Westpac Leading Index figures reveals that growth rate has shown a marginal uptick, moving from -0.67% to -0.60% in July. But alarmingly, this marks the twelfth consecutive month in red, representing the longest stretch of such negative prints in a span of seven years, barring the COVID-affected period.

The subdued, below-par growth momentum witnessed throughout 2023 seems set to persist into the subsequent year. Westpac predicts deceleration in GDP growth to a mere 1% for the current year. Any potential rebound is anticipated to be minimal, with projections indicating a slight rise to 1.4% annually in 2024 – with the bulk of this growth concentrated towards the year-end.

Regarding RBA meeting on September 5, Westpac sets its expectations clear. The institution foresees cash rate remaining stable at 4.10%, denoting the zenith of this current tightening phase.

Referring the recent remarks of RBA Governor before the House of Representatives Standing Committee on Economics, the note emphasized, “Policy is now in a ‘calibration’ phase with small adjustments still possible if the data starts to show clear risks of a slower return to low inflation.”

Nevertheless, given the evident frailty in growth momentum – as underscored by the most recent Leading Index update – coupled with the broader dynamics of price and wage inflation aligning with RBA’s forecasts, “the threshold for additional tightening is high and unlikely to be met.”

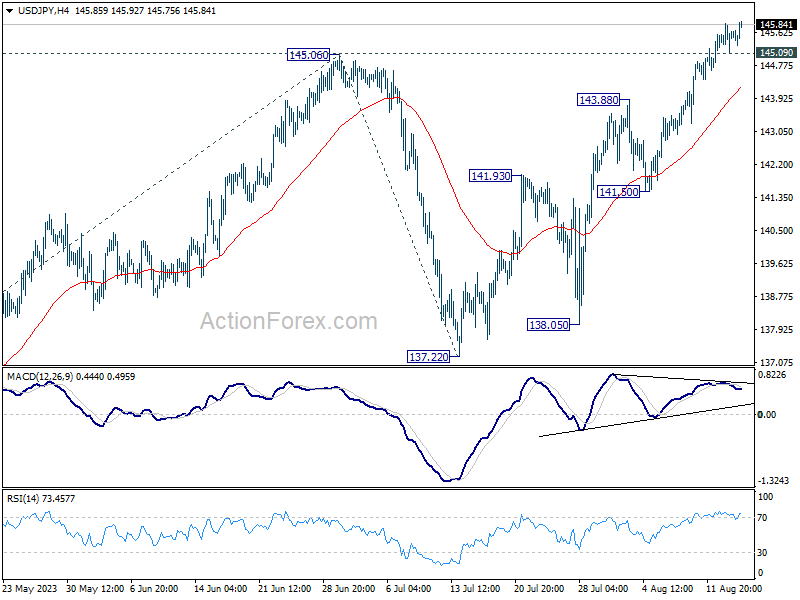

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.17; (P) 145.52; (R1) 145.93; More…

Intraday bias in USD/JPY remains on the upside at this point, despite some loss of momentum. Current rally from 127.20 is in progress for 61.8% projection of 129.62 to 145.06 from 137.22 at 146.76. On the downside, below 144.62 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

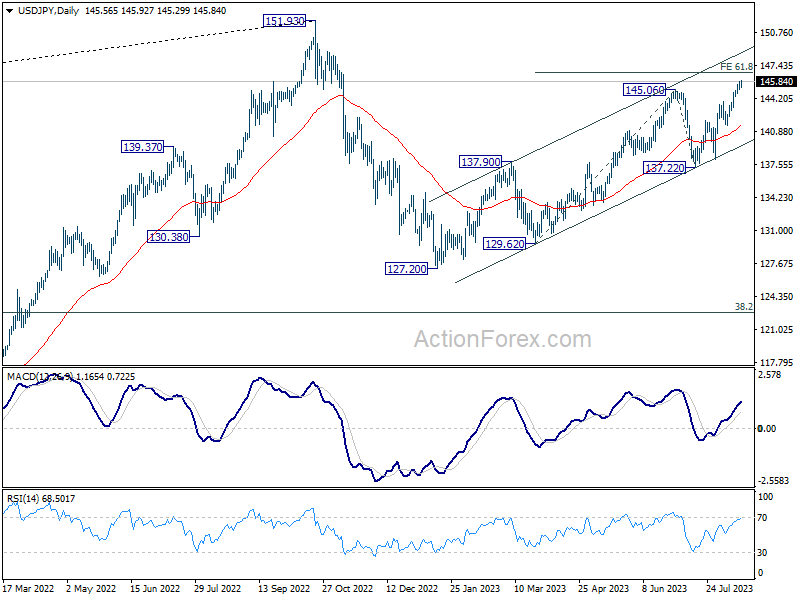

In the bigger picture, overall price actions from 151.93 (2022 high) are views as a corrective pattern. Rise from 127.20 is seen as the second leg of the pattern and could still be in progress. But even in case of extended rise, strong resistance should be seen from 151.93 to limit upside. Meanwhile, break of 137.22 support should confirm the start of the third leg to 127.20 (2023 low) and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Jul | 0.00% | 0.12% | ||

| 02:00 | NZD | RBNZ Interest Rate Decision | 5.50% | 5.50% | 5.50% | |

| 03:00 | NZD | RBNZ Press Conference | ||||

| 06:00 | GBP | CPI M/M Jul | -0.40% | -0.50% | 0.10% | |

| 06:00 | GBP | CPI Y/Y Jul | 6.80% | 6.80% | 7.90% | |

| 06:00 | GBP | Core CPI Y/Y Jul | 6.90% | 6.80% | 6.90% | |

| 06:00 | GBP | RPI M/M Jul | -0.60% | -0.70% | 0.30% | |

| 06:00 | GBP | RPI Y/Y Jul | 9.00% | 9.00% | 10.70% | |

| 06:00 | GBP | PPI Input M/M Jul | -0.40% | 0.00% | -1.30% | |

| 06:00 | GBP | PPI Input Y/Y Jul | -3.30% | -5.10% | -2.70% | -2.90% |

| 06:00 | GBP | PPI Output M/M Jul | 0.10% | -0.40% | -0.30% | -0.20% |

| 06:00 | GBP | PPI Output Y/Y Jul | -0.80% | -1.20% | 0.10% | 0.30% |

| 06:00 | GBP | PPI Core Output M/M Jul | 0.10% | -0.30% | -0.20% | |

| 06:00 | GBP | PPI Core Output Y/Y Jul | 2.30% | 1.60% | 3.00% | 3.10% |

| 09:00 | EUR | Eurozone GDP Q/Q Q2 P | 0.30% | 0.30% | 0.30% | |

| 09:00 | EUR | Employment Change Q/Q Q2 P | 0.20% | 0.40% | 0.60% | |

| 09:00 | EUR | Eurozone Industrial Production M/M Jun | 0.50% | 0.10% | 0.20% | |

| 12:15 | CAD | Housing Starts Y/Y Jul | 255K | 260K | 281.4K | |

| 12:30 | CAD | Wholesale Sales M/M Jun | -2.80% | -4.40% | 3.50% | 2.90% |

| 12:30 | USD | Housing Starts Jul | 1.45M | 1.45M | 1.43M | 1.40M |

| 12:30 | USD | Building Permits Jul | 1.44M | 1.47M | 1.44M | |

| 13:15 | USD | Industrial Production M/M Jul | 1.00% | 0.30% | -0.50% | -0.80% |

| 13:15 | USD | Capacity Utilization Jul | 79.30% | 79.00% | 78.90% | 78.60% |

| 14:30 | USD | Crude Oil Inventories | -2.4M | 5.9M | ||

| 18:00 | USD | FOMC Minutes |

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more