Dollar Down Slightly After ISM Manufacturing, Aussie Awaits RBA

Dollar falls broadly after ISM Manufacturing index indciates further deterioration in the sector. But loss is so far limited. Overall markets remain quiet. Swiss Franc and Yen persist are the softer performers. The Franc felt slight impact of Swiss CPI readings, which were lower than anticipated. However, market reaction remains mild, considering SNB’s prior forecast of slowing inflation in the current year. The central bank’s concern primarily lies in the potential for a resurgence in inflation thereafter. Meanwhile, Euro, Sterling, and Canadian Dollar remain steady, bounded within the range defined by Friday’s trading.

On the other side of the spectrum, Australian and New Zealand Dollars are showing minor strength. Volatility around Aussie is set to surge in the forthcoming Asian session as the market braces for RBA rate decision. It’s a split verdict among market observers, who are equally divided on the likelihood of a rate hike or a pause by the central bank. With two market surprises already in its repertoire for this year, the RBA may not shy away from a third.

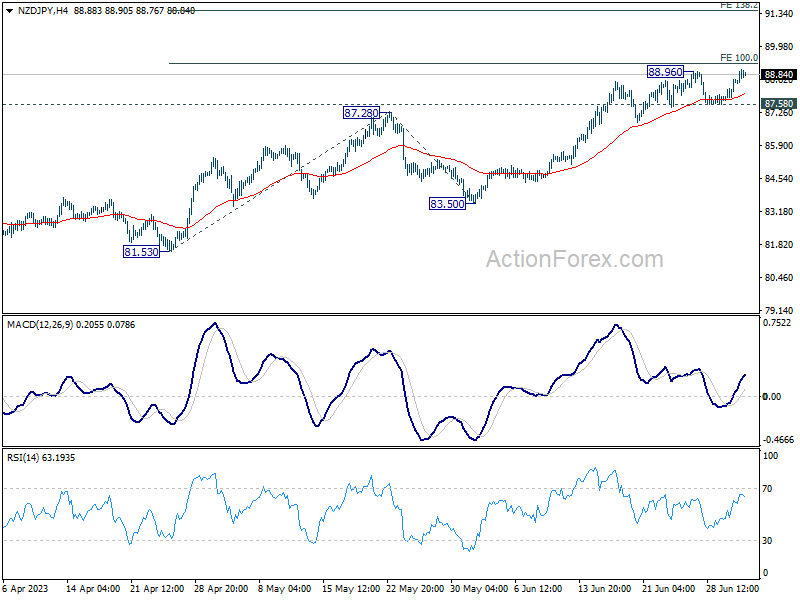

Technically, NZD/JPY is trying to resume recent rally by breaking through 88.96 resistance. But there’s a big question on whether it could power through 100% projection of 81.53 to 87.28 from 83.50 at 89.25. Rejection by this projection level, followed by break of 87.58 support, should confirm short term topping, and even reversal. But decisive break there will pave the way to 138.2% projection at 91.44. The next move could hinge on reaction to RBA.

In Europe, at the time of writing, FTSE is down -0.04%. DAX is down -0.24%. CAC is down -0.07%. Germany 10-year yield is up 0.017 at 2.411. Earlier in Asia, Nikkei rose 1.70%. Hong Kong HSI rose 2.06%. China Shanghai SSE rose 1.31%. Singapore Strait Times is up 0.04%. Japan 10-year JGB yield is up 0.0068 at 0.406.

Bundesbank Nagel: ECB still has a way to go with tightening

Bundesbank President Joachim Nagel acknowledged the rising doubt and escalating criticism around the necessity for more rate hikes. Yet, he insisted on the need for further tightening. He attributed his stance to the robust health of the labour market and the positive growth in the economy.

“We still have a way to go,” Nagel stated, referring to the ECB’s inflation-fighting measures. “Monetary policy signals are clearly pointing in the direction of more tightening”.

Furthermore, Nagel voiced his advocacy for the significant reduction of the Eurosystem’s balance sheet in the forthcoming years, following its expansion due to massive bond purchases and bank loans.

Eurozone PMI manufacturing finalized at 43.4, reacting negatively to ECB hikes

The final Eurozone PMI Manufacturing reading for June marked a further descent to 43.4, compared to May’s 44.8 – a slump to a low not seen in 37 months. The PMI Manufacturing Output Index also ended lower at 44.2, an 8-month low from May’s 46.4.

The decline wasn’t restricted to a single nation, but spread across several member states, demonstrating widespread economic pressure. Greece was a rare positive outlier, reaching a two-month high at 51.8. In contrast, Spain slid to a 6-month low at 48.0, while Ireland plummeted to a 37-month low at 47.3. France achieved a slight uptick to a 3-month high of 46.0, while Netherlands, Italy, and Germany dipped to 37- and 38-month lows. Austria reached the lowest level, falling to a 38-month low at 39.0.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, articulated the stark economic picture: “Eurozone manufacturing production contracted for the third month in a row in June…with the rate of decline accelerating, pointing to a worsening of factory conditions.”

He also pointed to the negative reaction of the capital-intensive industrial sector to the ECB’s interest rate hikes. For the first time since January 2021, surveyed companies reported a reduction in their headcount. Additionally, purchasing activity declined at one of the most severe rates on record. As demand weakened and costs deflated rapidly, companies cut their sales prices for the second consecutive month.

On a slightly brighter note, de la Rubia noted the continued normalization of delivery times since February, but cautioned that material shortages remain a persisting issue.

UK PMI manufacturing finalized at 46.5, continued to report recessionary conditions

UK PMI Manufacturing was finalized at 46.5 in June, down from May’s 47.1, a six-month low. S&P Global noted that output fell in intermediate and investment goods sectors. Input prices and output charges both fell.

Rob Dobson, Director at S&P Global Market Intelligence, said:

“The UK manufacturing sector continued to report recessionary conditions in June. The headline PMI dropped to a six-month low as output, new orders and employment all suffered further declines. Producers are being hit by weak domestic and export market conditions with clients showing a greater reluctance to commit to spending due to market uncertainty, increased competition and elevated costs. This is also impacting business optimism and stoking fears among some manufacturers that client spending may shift to lower cost rivals and markets.

“Although some respite is being offered in the short-term by reduced pressures on supply chains and costs, these remain a symptom of the current weakness of demand faced by the sector and are therefore unlikely to play a role in boosting production moving forward. Manufacturers therefore remain in defence mode, looking to cut back spending on purchasing and employment wherever possible and release capital tied up in stocks.”

Swiss CPI slowed to 1.7% yoy in Jun, imported products down -0.1% yoy

Swiss CPI rose 0.1% mom in Jun, below expectation of 0.2% mom. Core CPI (excluding fresh and seasonal products, energy and fuel) was flat mom. Domestic products prices rose 0.2%. Imported products prices dropped -0.3% mom.

For the 12 month period, CPI slowed from 2.2% yoy to 1.7% yoy, below expectation of 1.8% yoy. Core CPI ticked down from 1.9% yoy to 1.8% yoy. Domestic products inflation dropped from 2.4% yoy to 2.3% yoy. Import products inflation turned negative from 1.4% yoy to -0.1% yoy.

BoJ’s Tankan survey indicates renewed confidence amongst Japanese businesses

BoJ’s quarterly Tankan survey for Q2 has pointed to an uptick in confidence among Japanese businesses, surpassing market expectations.

Large manufacturing index, a key barometer of Japan’s industrial sector, saw an impressive rise from a two-year low of 1 to 5, outperforming the market expectation of 3. This level marks the highest index value since Q4 of 2022, signifying a considerable rebound in sentiment within the manufacturing sector.

Similarly, large non-manufacturing index advanced from 20 to 23, again exceeding market forecasts of 22. This development signals the highest reading since Q2 2019, reflecting a resurgence in confidence within the broader service sector.

Looking forward, outlook for large manufacturers also leaped from 3 to 9, beating market predictions of 5. However, the outlook for large non-manufacturing firms was slightly below expectations at 20, compared to an anticipated figure of 21.

On the capital expenditure front, large firms plan to ramp up their outlays by a notable 13.4% in the current fiscal year ending March 2024, dwarfing the 3.2% increase projected in the Q1 survey.

Interestingly, the Tankan survey also revealed that companies foresee inflation hitting 2.6% a year from now, a slight pullback from the 2.8% projection made in March. Looking further ahead, inflation expectations stand at 2.2% for three years’ time, a slight reduction from March figure of 2.3%, while projection for inflation five years from now remains stable at 2.1%.

Japan PMI manufacturing finalized at 49.8, fractional deterioration in the sector

Japan’s Manufacturing PMI was finalized at 49.8 in June, a downturn from May’s 50.6, according to au Jibun Bank. The reading fell just short of the neutral 50.0 threshold that separates expansion from contraction, indicating a slight decline in the health of the nation’s manufacturing sector.

The report also highlighted that both output and new orders regressed, while supplier performance showed the most significant improvement since March 2016. Input prices increased at the slowest pace observed in the past 28 months.

Usamah Bhatti of S&P Global Market Intelligence noted, “The latest data pointed to a fractional deterioration in the Japanese manufacturing sector at the midpoint of 2023.”

However, the slackening in demand and output conditions had a double-edged effect. On one hand, pressure on supply chains eased in June, with average lead times shortening for the second successive month. Simultaneously, easing pressure on supply chains also alleviated inflationary pressures, driving the Input Prices Index to a 28-month low.

China Caixin PMI manufacturing dipped to 50.5, dire job market, deflationary pressure, waning optimism

China’s Caixin PMI Manufacturing for June recorded a slight decline from 50.9 in May to 50.5. slightly above expectation of 50.2. Caixin indicated that while output marginally increased, demand growth remained modest. Meanwhile, input prices experienced their sharpest decline since January 2016, and business confidence sank to an eight-month low.

Wang Zhe, Senior Economist at Caixin Insight Group, summed up the situation: “Manufacturing activity growth suffered a marginal slowdown.”

“A slew of recent economic data suggests that China’s recovery has yet to find a stable footing, as prominent issues including a lack of internal growth drivers, weak demand and dimming prospects remain,” Wang added.

“Problems reflected in June’s Caixin China manufacturing PMI, ranging from an increasingly dire job market to rising deflationary pressure and waning optimism, also point to the same conclusion.”

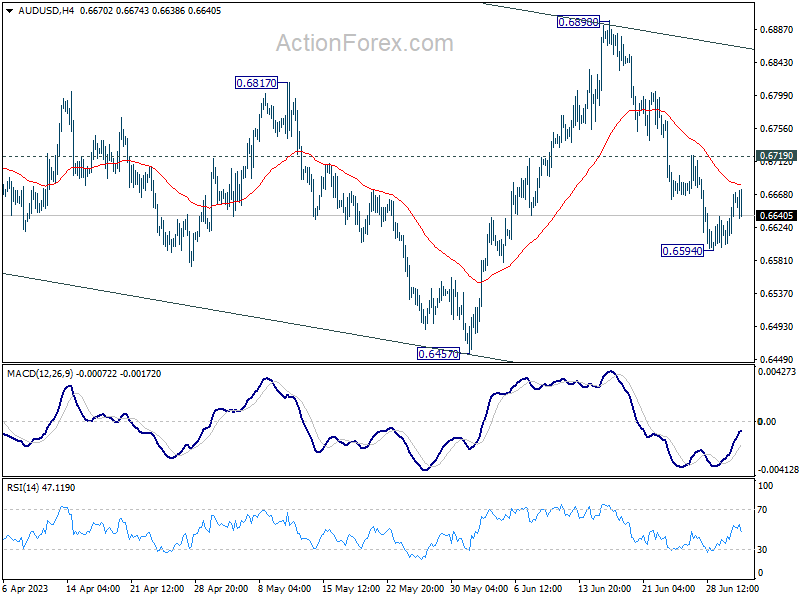

AUD/USD Daily Report

Daily Pivots: (S1) 0.6618; (P) 0.6645; (R1) 0.6687; More…

Intraday bias in AUD/USD remains neutral and further fall is in favor with 0.6719 resistance intact. On the downside, break of 0.6594 will resume the decline to 0.6457 support next. Nevertheless, firm break of 0.6719 will turn bias back to the upside for stronger rebound.

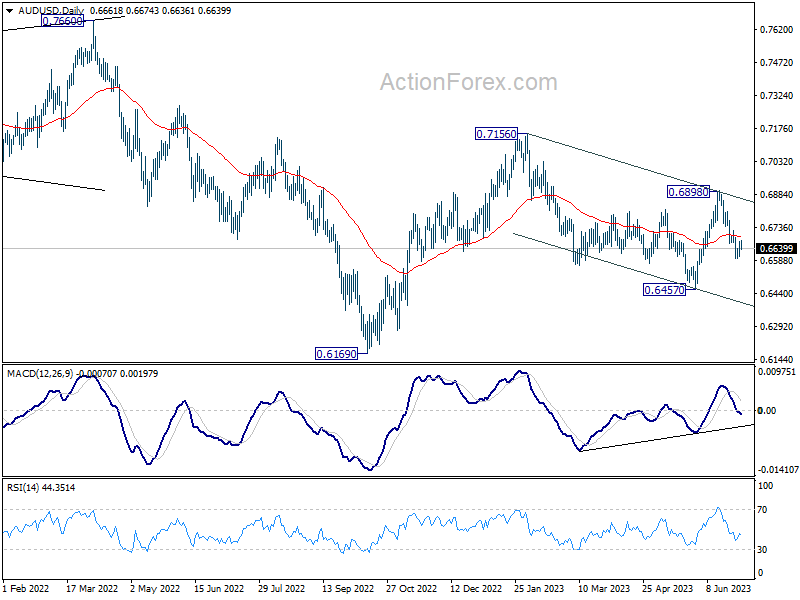

In the bigger picture, price actions from 0.7156 are seen as a correction to the rebound from 0.6169 only, rather than part of larger down trend from 0.8006 (2021 high). Break of 0.6457 could be seen but downside should be contained above 0.6169. This will now remain the favored case as high as 0.6898 resistance holds. Nevertheless, break of 0.6898 resistance will argue that rise form 0.6169 is ready to resume through 0.7156.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M May | -2.20% | -2.60% | ||

| 23:50 | JPY | Tankan Large Manufacturing Index Q2 | 5 | 3 | 1 | |

| 23:50 | JPY | Tankan Non – Manufacturing Index Q2 | 23 | 22 | 20 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q2 | 9 | 5 | 3 | |

| 23:50 | JPY | Tankan Non – Manufacturing Outlook Q2 | 20 | 21 | 15 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q2 | 13.40% | 3.20% | ||

| 00:30 | JPY | Manufacturing PMI Jun F | 49.8 | 49.8 | 49.8 | |

| 01:00 | AUD | TD Securities Inflation M/M Jun | 0.10% | 0.90% | ||

| 01:30 | AUD | Building Permits M/M May | 20.60% | 4.90% | -8.10% | -6.80% |

| 01:45 | CNY | Caixin Manufacturing PMI Jun | 50.5 | 50.2 | 50.9 | |

| 06:30 | CHF | CPI M/M Jun | 0.10% | 0.20% | 0.30% | |

| 06:30 | CHF | CPI Y/Y Jun | 1.70% | 1.80% | 2.20% | |

| 07:30 | CHF | Manufacturing PMI Jun | 44.9 | 42.8 | 43.2 | |

| 07:45 | EUR | Italy Manufacturing PMI Jun | 43.8 | 45.4 | 45.9 | |

| 07:50 | EUR | France Manufacturing PMI Jun F | 46 | 45.5 | 45.5 | |

| 07:55 | EUR | Germany Manufacturing PMI Jun F | 40.6 | 41 | 41 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun F | 43.4 | 43.6 | 43.6 | |

| 08:30 | GBP | Manufacturing PMI Jun F | 46.5 | 46.2 | 46.2 | |

| 13:45 | USD | Manufacturing PMI Jun F | 46.3 | 46.3 | 46.3 | |

| 14:00 | USD | ISM Manufacturing PMI Jun | 46 | 47.2 | 46.9 | |

| 14:00 | USD | ISM Manufacturing Prices Paid Jun | 41.8 | 44.2 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Jun | 48.1 | 51.4 | ||

| 14:00 | USD | Construction Spending M/M May | 0.90% | 0.50% | 1.20% | 0.40% |

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more