Antipodean Currencies Under Pressure With Sterling, Euro Shrugs Weak Investor Confidence

Australian and New Zealand Dollar are under some selling pressure today, with the Sterling following suit. These currency fluctuations do not appear to be tied to any specific market developments, but their concurrent weakness may suggest a cautious undertone prevalent among risk-averse traders. Notably, market participants might be realigning their positions in anticipation of this week’s UK employment and GDP data, and RBNZ hold.

Simultaneously, capital appears to be flowing towards Dollar, Canadian and Euro. Despite rather poor Eurozone investor sentiment data, Euro remains robust. The immediate outlook for Dollar hinges largely on the upcoming CPI and PPI data. Canadian Dollar is buoyed by firm oil prices and expectations of an imminent rate hike from BoC. Meanwhile, Yen is extending recent rally against the weaker currencies today while staying firm in tight range against Dollar and Euro.

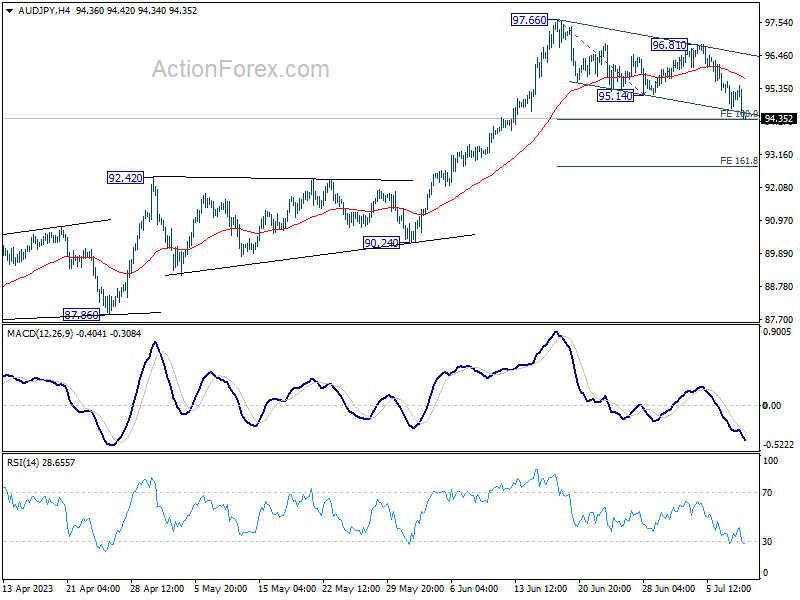

Technically, AUD/JPY in proximity to 100% projection of 97.66 to 95.14 from 96.81 at 94.29. Strong support could be seen around current level to bring rebound. Break of 95.14 support turned resistance be a signal of short term bottoming. However, sustained trading below 94.29, and further downside acceleration, will argue that AUD/JPY is probably reversing the whole rise from 86.04 (March low).

In Europe, at the time of writing, FTSE is up 0.46%. DAX is up 0.54%. CAC is up 0.70%. Germany 10-year yield is up 0.0251 at 2.660. Earlier in Asia, Nikkei dropped -0.61%. Hong Kong HSI rose 0.62%. China Shanghai SSE rose 0.22%. Singapore Strait Times rose 0.31%. Japan 10-year JGB yield rose 0.0363 at 0.473.

Eurozone Sentix fell to -22.5, more serious than usual summer lull

The economic outlook for Eurozone dimmed as Sentix Investor Confidence Index suffered its third consecutive monthly fall, reaching an eight-month low in July. The index tumbled from -17 to -22.5, significantly underperforming market expectations of -18.9. Both Current Situation Index and Expectations Index followed suit, dropping from -15.8 to -20.5 and from -18.3 to -24.5 respectively.

Sentix offered a stark assessment of the situation: “As of early July 2023, the Eurozone economy remains in recession mode.” The investment group expressed skepticism about the potential sources of an economic boost, observing the U.S. economy’s struggle to generate positive momentum, while downplaying any hope of central banks stepping in to counteract the economic downturn.

The investor sentiment towards the central banks’ policies was especially pessimistic, with the topic index “central bank policy” plummeting from -13 to -24, indicating that investors foresee an intensification of restrictive monetary measures.

Compounding this gloomy outlook, the corresponding Inflation Barometer slid from -6 to -14.5 points, with Sentix cautioning that the current situation is “clearly more serious than the usual summer lull”.

BoJ upgrades assessment on three regions, all picking or recovering moderately

In the Regional Economic Report released today, BoJ painted an encouraging picture of economic recovery. Despite challenges like past spike in commodity prices. All nine regions “had been either picking up or recovering moderately”.

Moreover, three regions – Tokai, Chugoku, and Kyushu-Okinawa – have received upgrades in their economic outlooks, while the views on Hokkaido, Tohok, Hokuriku, Kanto-Koshinetsu, Kinki, and Shikoku remain unchanged.

The report also revealed that numerous regions have seen wage increases across small and mid-sized firms broadening to an extent not witnessed in recent years. However, the future of these wage hikes remains uncertain.

Takeshi Nakajima, BoJ’s branch manager overseeing Kansai western Japan region, underscored this ambiguity, stating that it’s premature to predict if companies will continue raising wages next year. “A lot of companies in the region say that will depend on this year’s earnings and what their rivals could do,” Nakajima said during a news conference.

He added, “If companies can earn enough revenues to pay for higher wages, there’s hope wage rises will continue. Given uncertainty over the outlook, however, it’s premature to say decisively that this will happen.”

China’s PPI down -5.4% yoy, CPI flat in Jun

China’s factory-gate inflation, as measured by PPI, marked its ninth consecutive decline in June, slumping by -5.4% yoy. This drop is the steepest since December 2015 and outstripped -4.6% yoy in May, a well as expectation of -5.0 yoy. PPI fell -0.8% on a month-on-month basis in June, slightly less than the -0.9% mom fall registered in May.

National Bureau of Statistics statistician Dong Lijuan pointed to tumbling commodity prices, particularly oil and coal, as the driving force behind the slump in factory-gate prices. The comparison to high base figures from the previous year also played a role in the significant drop.

Additionally, China’s CPI continued to lose momentum, sliding from 0.2% yoy in May to 0.0% yoy in June, its lowest reading since February 2021. This downturn defied expectations of a 0.2% yoy. On a month-on-month basis, June’s CPI mirrored the previous month, dipping by -0.2%.

Analysing the CPI’s components, core CPI, which excludes volatile food and energy prices, showed a tempered 0.4% yoy rise, compared to 0.6% yoy in May. Food prices accelerated by 2.3% yoya leap from May’s 1.0% yoy increase, while non-food prices moved in the opposite direction, falling by -0.6% yoy in contrast to a flat performance in May.

The sustained descent in PPI, coupled with lackluster CPI, underlines the ongoing deflationary pressures in China’s economy.

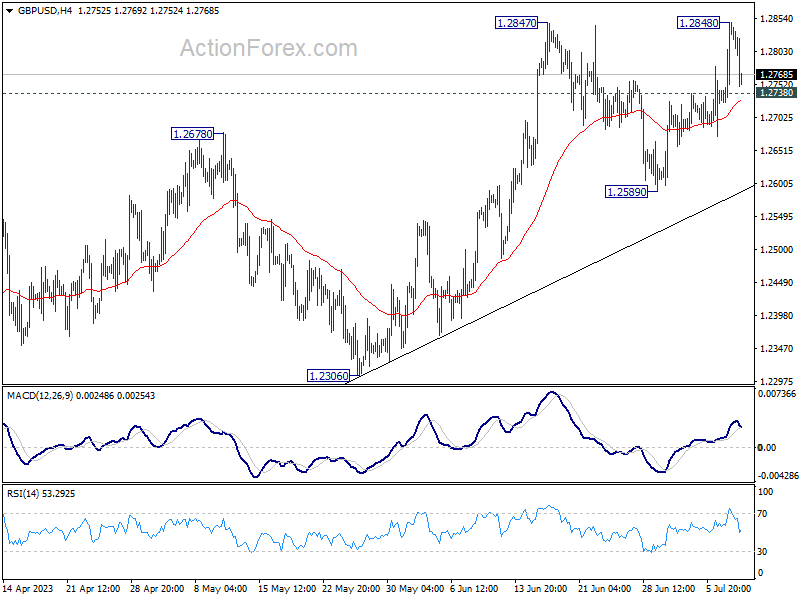

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2760; (P) 1.2805; (R1) 1.2883; More…

Intraday bias in GBP/USD is turned neutral with current retreat. On the downside, break of 1.2738 minor support will indicate that consolidation from 1.2847 is extending with another falling leg, back to 1.2589 support. On the upside, decisive break of 1.2847/8 will confirm resumption of larger up trend from 1.0351. Next target is 61.8% projection of 1.0351 to 1.2445 from 1.1801 at 1.3095.

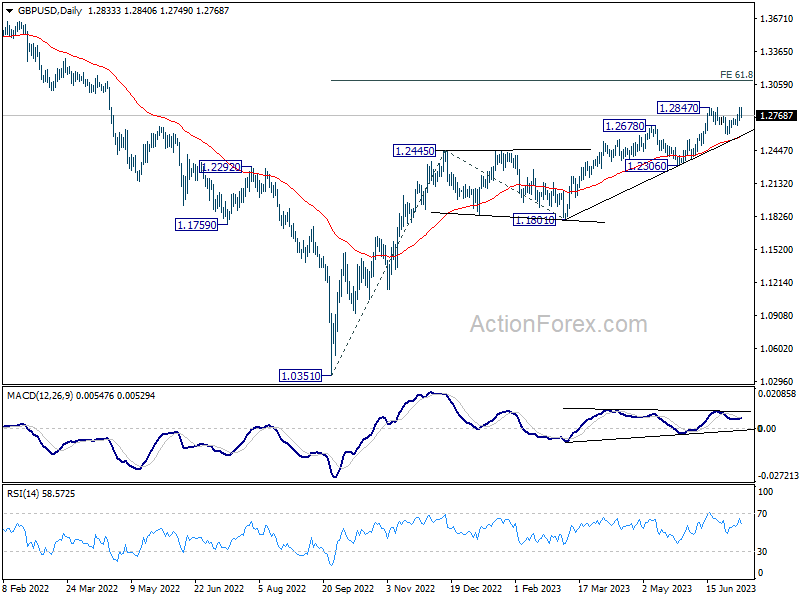

In the bigger picture, the strong support from 55 W EMA (now at 1.2341) is a medium term bullish sign. Outlook will stay bullish as long as 1.2306 support holds. Rise from 1.0351 medium term bottom (2022 low) is expected to extend further to retest 1.4248 key resistance (2021 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Bank Lending Y/Y Jun | 3.20% | 3.50% | 3.40% | |

| 23:50 | JPY | Current Account (JPY) May | 1.70T | 1.87T | 1.90T | |

| 01:30 | CNY | CPI Y/Y Jun | 0.00% | 0.20% | 0.20% | |

| 01:30 | CNY | PPI Y/Y Jun | -5.40% | -5.00% | -4.60% | |

| 05:00 | JPY | Eco Watchers Survey: Outlook Jun | 53.6 | 54.8 | 55 | |

| 08:30 | EUR | Eurozone Sentix Investor Confidence Jul | -22.5 | -18.9 | -17 | |

| 12:30 | CAD | Building Permits M/M May | 10.50% | 7.30% | -18.80% | |

| 14:00 | USD | Wholesale Inventories May F | -0.10% | -0.10% |

Gyrostat Capital Management: Why Risk Management Is Not About Predicting Risk

Why Risk Management is Not About Predicting Risk Financial markets reward confidence, but they punish certai... Read more

Gyrostat January Outlook: Calm At Multiyear Extremes

This monthly Gyrostat Risk-Managed Market Outlook does not attempt to forecast market direction. Its p... Read more

Gyrostat December Outlook: The Market Does The Work

Harnessing Natural Volatility for Consistent Returns Markets have always moved more th... Read more

Gyrostat Capital Management: Why Advisers Must Scenario-Plan Both The Bubble And The Bust

The Blind Spot: Why Advisers Must Scenario-Plan Both The Bubble and The Bust In financial m... Read more

Gyrostat Capital Management: The Hidden Architecture Of Consequences

When Structures Themselves Become A Risk In portfolio construction, risk is rarely where we look for it.... Read more

Gyrostat November Outlook: The Rising Cost Of Doing Nothing

Through the second half of 2025, markets have delivered a curious mix of surface tranquillity and instabi... Read more