Adani Group's Debt Pile Up Almost 21%, Relies On Global Banks For Funding

Adani Group’s pile of debt increased almost 21% over the past year and the proportion held by global banks rose to nearly a third, according to data seen by Bloomberg that offers an up-to-date snapshot of its financial health.

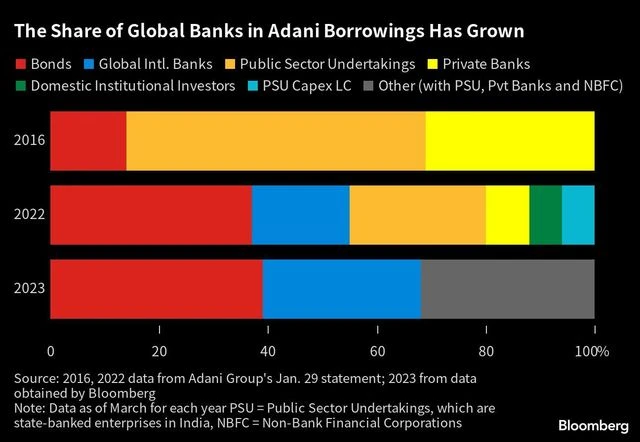

Information gleaned from people familiar with the conglomerate’s inner workings as well as from presentations to investors reveal 29% of its borrowings were with global international banks at the end of March — a category that didn’t feature on the group’s list of creditors seven years ago.

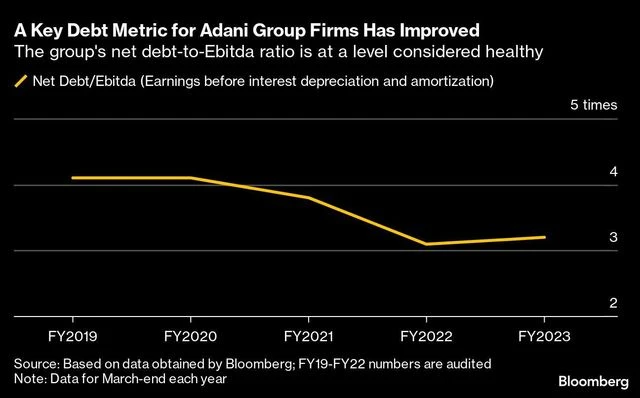

Yet the data also show a metric for its ability to pay off its debts improved.

"chart")

The shifting state of its finances and creditor mix underscores just how swiftly billionaire Gautam Adani’s group, based in the Indian state of Gujarat, has grown and how connected it has become internationally, with business interests as far away as Australia and Israel.

But with that worldwide engagement comes heightened scrutiny, such as it faced when US shortseller Hindenburg Research accused it of extensive corporate fraud.

Despite Adani executives repeatedly denying the allegations and seeking to reassure investors with in-person meetings and repaying debt, the conglomerate’s stocks and dollar bonds have yet to fully recover from the selloff caused by Hindenburg.

That suggests the group may have to pay more to raise money down the road, though an improving debt ratio might help counter any increase. Two global rating firms have said they will closely watch Adani entities’ ability to raise funds.

Here are some details on how the conglomerate’s finances stacked up as of the end of last month. A spokesman for Adani Group did not immediately comment when contacted by Bloomberg about the figures.

"chart")

Adani firms have over the past few years improved on a key metric measuring a company’s ability to service its liabilities, according to the data seen by Bloomberg. The ratio of net debt to run-rate earnings before interest, tax, depreciation and amortization was about 3.2 in the 2023 fiscal year, which ended in March. That’s down from what an Adani report from last September showed to be 7.6 in 2013.

Run-rate Ebitda is calculated by an extrapolation of a firm’s recent financial performance.

Adani Group was looking to reduce its debt further, according to the data.

Concerns about Adani finances started making headlines last year, when research firm CreditSights termed it “deeply overleveraged.” The group countered the claim by saying companies had reduced their debt burden.

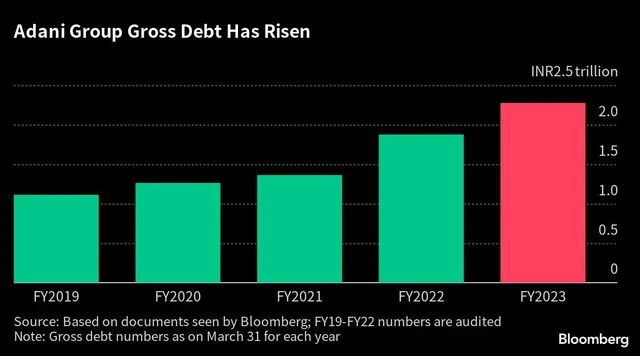

Gross debt at seven main listed Adani firms rose 20.7% to 2.3 trillion rupees ($28 billion) as of March 31, according to the people familiar with the matter, who asked not to be named because they weren’t authorized to speak publicly about it. The borrowings have risen steadily since 2019, as the conglomerate expanded at breakneck speed.

Fallout from Hindenburg’s report, published in late January, has resulted in Adani Group rescaling its grand ambitions, dialing back on petrochemicals, aluminum, steel and road projects while focusing on its core areas that include ports, power and green energy, Bloomberg reported last month.

The most recent data seen by Bloomberg give a sense of creditor exposure. Bonds accounted for 39% of the group’s borrowings as of end March, up from 14% in 2016.

"chart")

Still, local borrowings can be sizable. State Bank of India, the nation’s top lender by assets, had an exposure of about 270 billion rupees ($3.3 billion) to the group, its chairman said in February.

Moody’s Investors Service in February flagged the risk of a jump in funding costs and refinancing needs worth billions of dollars in the next few years.

But a spokesman for the conglomerate told Bloomberg earlier this month there’s “no material refinancing risk” and that near-term liquidity requirements are comfortable because there are no big debt repayments due in coming months.

"chart")

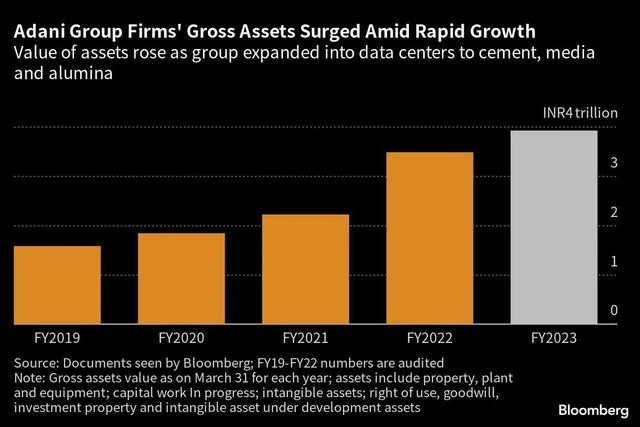

The upside of Adani’s growth and diversification has been a steadily increasing pile of assets — a more than doubling in five years. The first-generation entrepreneur started off as a diamond trader in the 1980s and was until recently Asia’s richest man. He built his empire on the ports and coal trading and in the past few years expanded into airports, renewable energy, data centers, cement and media.

Stablecoin The Future Of Currency?

The payments system is undergoing a quiet but consequential shift. What was once the exclusive preserve of central banks... Read more

BoE Loosens Capital Rules

The Bank of England has taken a significant step towards easing post-crisis regulation by lowering its estimate of the c... Read more

Monzo Looks For US Banking License

Monzo is preparing a renewed push to secure a US banking licence, four years after abandoning its first attempt when tal... Read more

Crypto Firms Push Into US Banking

America’s cryptocurrency companies are scrambling to secure a foothold in the country’s traditional banking system, ... Read more

Parallel Banking: Stablecoins Are Now Global

Parallel Banking: How Stablecoins Are Building a New Global Payments SystemStablecoins—digital currencies pegged to tr... Read more

JPMorgan Deploys AI Chatbot To Revolutionize Research And Productivity

JPMorgan has deployed an AI-based research analyst chatbot to enhance productivity among its workforce, with approximate... Read more