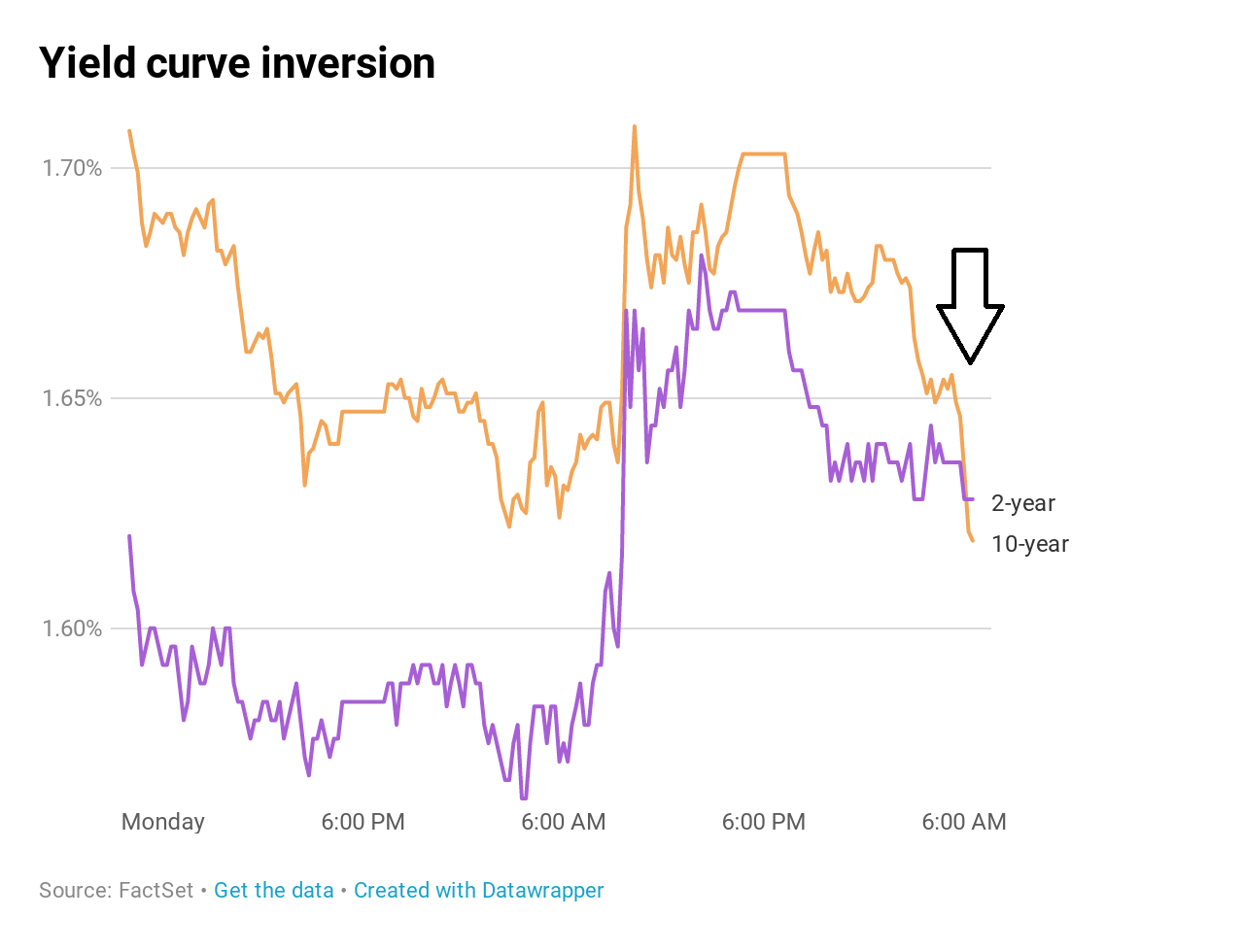

The yield on the benchmark 10-year Treasury note broke below the 2-year rate early Wednesday, an odd bond market phenomenon that has been a reliable, albeit early, indicator for economic recessions.

The yield on U.S. 30-year bond also turned heads on Wall Street during Wednesday's session as it fell to an all-time low, dropping past its prior record notched in summer 2016. The two historic moves coming in tandem show that investors are increasingly worried, and indeed preparing for, a slowdown in both the U.S. and global economies.

Earlier Wednesday, the yield on the benchmark 10-year Treasury note was at 1.623%, below the 2-year yield at 1.634%. In practice, that means that investors are better compensated for loaning the U.S. over two years than they are for loaning for 10 years. The yields steepened later in the session, pushing the 10-year rate back above that of the 2-year note at 1.58%.

The yield on the 30-year Treasury bond traded at 2.02%, well below its former record low of 2.0889% hit in 2016 following Britain's Brexit vote. Yields fall as bond prices rise.

The last inversion of this part of the yield curve was the one that began in December 2005, two years before the financial crisis and subsequent recession. Economists often give the spread between the 10-year and the 2-year special attention because inversions of that part of the curve have preceded every recession over the past 50 years.

"I have to yield to the historical evidence and note that the phrase 'this time is different' usually doesn't work," said Arthur Bass, managing director of fixed income financing, futures, and rates at Wedbush Securities.

"It's a very unusual time period: We haven't had tariff issues like we're dealing with currently in about 80 years," he continued. "It's about dealing with negative rates in most of the European countries and Japan. Again, I have respect for the inverted yield curve as a signal that recession is ahead."

Still, while the inversion is cause for concern, there is often a significant lag before a recession hits and an economic downturn ensues.

Historical inversions of the 2-10 curve (recessions marked in gray)

.1565784045320.png)

Data from Credit Suisse going back to 1978 shows:

- The last five 2-10 inversions have eventually led to recessions.

- A recession occurs, on average, 22 months following a 2-10 inversion.

- The S&P 500 is up, on average, 12% one year after a 2-10 inversion.

- It's not until about 18 months after an inversion when the stock market usually turns and posts negative returns.

Going farther back in history, the yield curve's track record gets a little more spotty. Post WWII, inversions have predicted seven of the last nine recessions, according to Sung Won Sohn, professor of economics at Loyola Marymount University and president of SS Economics.

"This is a track record any economist would be proud of," said Sohn.

Long-term yields have plummeted in August as concerns surrounding trade developments and GDP growth — coupled with expectations for lackluster inflation and more aggressive central bank action — have sent nervous traders in search of safer investments.

Central banks around the world, including the Federal Reserve, have pivoted once again to easing policies. Major government debt in countries like Germany now have negative yields.

The yield on the 10-year Treasury note, an important rate banks use when setting mortgage rates and other lending, has fallen a steep 40 basis points this month.

"The US equity market is on borrowed time after the yield curve inverts. However, after an initial post-inversion dip, the S&P 500 can rally meaningfully prior to a bigger US recession related drawdown," wrote Bank of America technical strategist Stephen Suttmeier.

A portion of the yield curve inverted earlier this year, raising economic concerns as three-month yield topped the 10-year yield.

The popularity of the safety offered by bonds is at financial crisis levels among professional investors as many steel themselves for slowing growth ahead, according to a survey of fund managers conducted by Bank of America Merrill Lynch.

The poll found a net 43% of market pros see lower short-term rates over the next 12 months, compared with just a net 9% that saw higher long-term rates. In sum, that's the most bullish outlook on fixed income since November 2008.

"While yield curve inversions can be a leading indicator of economic weakness or recession, they are an early warning sign," Suttmeier said.

— CNBC's Jeff Cox contributed reporting.